Yes Bank Ltd (YESBANK)

Stock Analysis Report

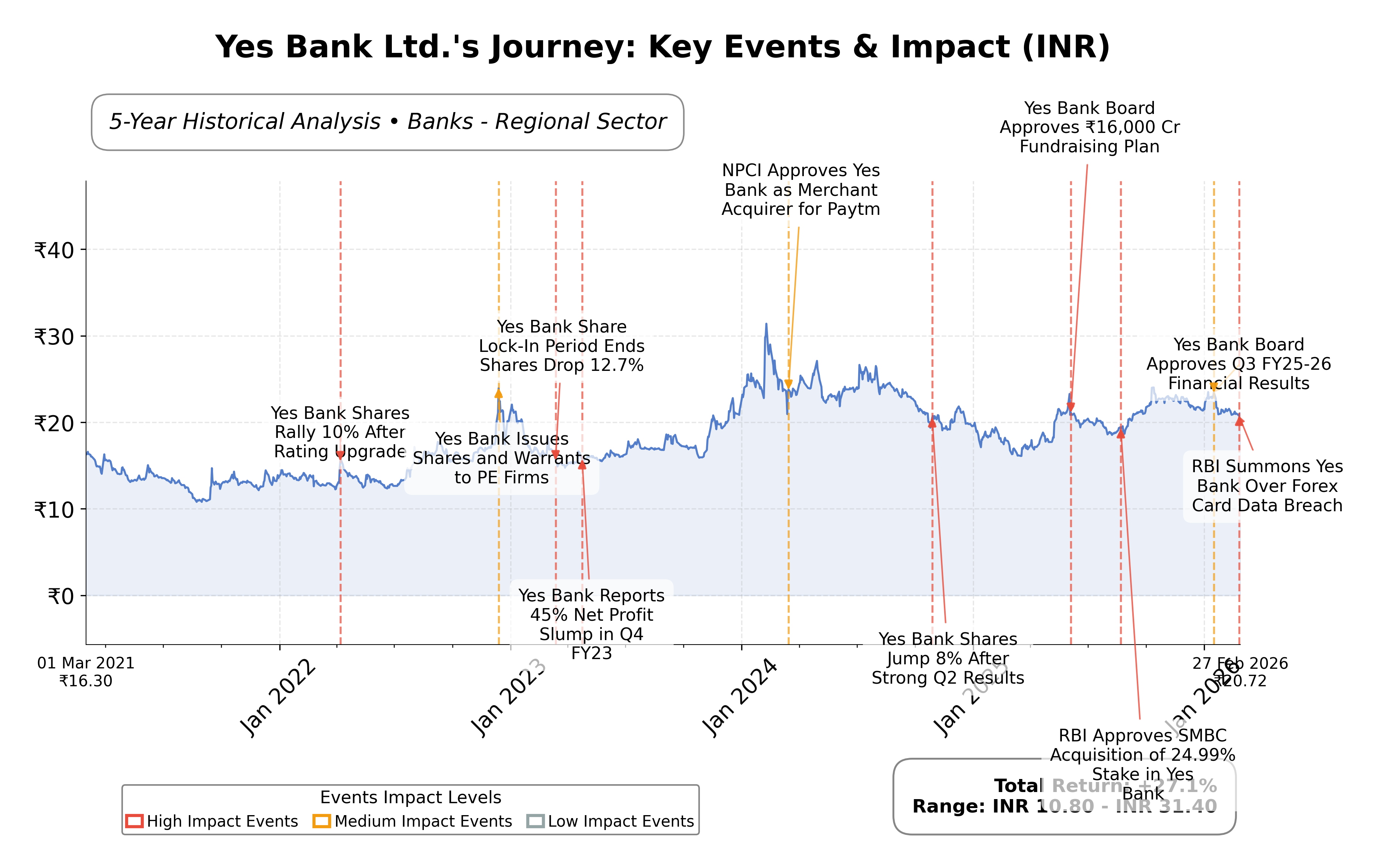

Stock Journey

Key Positives and Key Risks

Pros

- Quarterly revenue growth of 17.4% demonstrates strong top-line momentum.

- Operating cash flow of ₹94.15 billion supports liquidity and operational strength.

- Insider ownership at 44.18% indicates significant management alignment and control.

Cons

- Return on equity at 6.53% is lower compared to several regional banking peers.

- Total debt-to-equity ratio of 1.27 reflects elevated leverage typical of banking but a potential risk factor.

- Recent forex card fraud incidents raise concerns about operational and security risks.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Yes Bank Ltd. is a leading private sector bank in India, operating within the regional banking industry. Established in 2004, it offers a wide range of financial services including corporate financing, retail banking, wealth management, and investment banking. The bank emphasizes digital transformation and innovation to serve diverse customer segments, from SMEs to large corporations, positioning itself as a technology-driven financial institution in the Indian banking landscape.

Financially, Yes Bank reported a trailing P/E ratio of approximately 20.51 and a forward P/E of 15.62, with a market capitalization near â¹650.79 billion. The bankâs profit margin stands at 20.49%, with return on equity at 6.53% and return on assets at 0.75%. Its price-to-book ratio is 1.32, and the bank maintains a significant cash position of nearly â¹199 billion against total debt of about â¹638 billion. Revenue growth over the last quarter was 17.4%, with net income of over â¹31.6 billion and positive operating cash flow trends.

From a strategic and technical perspective, Yes Bank has recently seen leadership changes with a new Managing Director appointment and is actively addressing operational risks such as a forex card fraud incident. The bankâs stock trades near its 52-week midpoint with moderate volatility (beta 0.18), showing resilience amid sector challenges. Institutional ownership is modest, with insiders holding about 44%, reflecting significant internal stakeholder confidence. However, risks remain from regulatory scrutiny and fraud-related incidents, balanced by ongoing strategic initiatives and partnership expansions.

In comparison to its Indian regional banking peers such as Bandhan Bank, Bank of India, IDBI Bank, Indian Bank, and Kotak Mahindra Bank, Yes Bankâs valuation metrics like P/E and P/B ratios are generally in line or slightly higher, while its return on equity is somewhat lower. Market capitalization places it in the mid-tier among these peers. The bankâs price-to-cash-flow ratio is relatively lower, indicating potential operational efficiency. Peer institutions show varied growth and profitability profiles, with Kotak Mahindra Bank leading in market cap and return metrics.

Navigating a competitive and evolving banking sector, Yes Bank stands at a pivotal juncture marked by recent operational challenges and strategic realignments. The bankâs emphasis on digital innovation and financial inclusion underscores its growth ambitions, while regulatory and fraud-related issues pose ongoing challenges. The companyâs ability to leverage its internal strengths and manage external risks will be critical in shaping its trajectory. Evaluating the current financial and market data suggests a stance that balances cautious observation with recognition of underlying growth potential.

Company and Industry Overview

Company Basics

Price Performance

Company Size

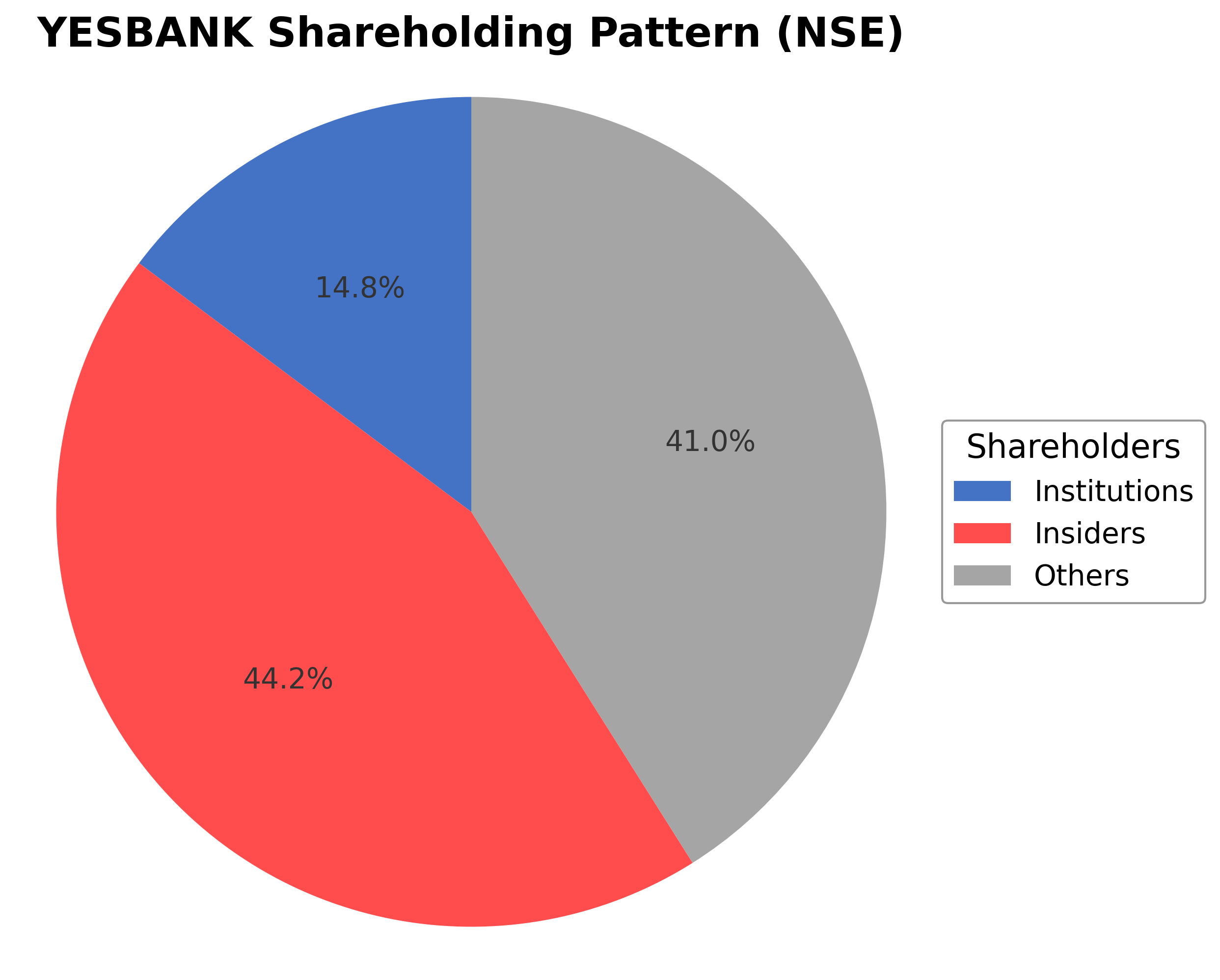

Shareholding Pattern

Yes Bank Ltd.'s ownership structure comprises approximately 44.18% held by insiders including executives and board members, 14.77% by institutional investors such as mutual funds and pension funds, and the remaining 41.05% by public shareholders including retail investors and employee stock plans. Over the past 12-24 months, insider holdings have remained relatively stable, while institutional investors have shown modest accumulation, reflecting cautious confidence. Major funds have adjusted positions in line with market conditions and regulatory developments. These shareholding patterns suggest a balanced market sentiment with significant internal control, which may influence governance and strategic decisions. The bank operates within the Indian regional banking sector, characterized by increasing digital adoption, regulatory oversight, and competitive pressures from both traditional and fintech players.

Sector and Industry Analysis

Sector and Industry Analysis: Indian Banking Sector with Focus on Private Sector Banks (Including Yes Bank Ltd.)

1. Sector Overview: The Indian banking sector is a critical component of the country’s financial system, encompassing public sector banks (PSBs), private sector banks, foreign banks, and regional rural banks. The sector’s market size is substantial, with total assets exceeding ₹150 trillion as of recent years. Private sector banks, including Yes Bank Ltd., have been gaining market share due to their agility, customer-centric innovations, and relatively higher operational efficiencies compared to many PSBs. Key private sector players include HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra Bank, and Yes Bank. The sector has exhibited a robust growth trajectory driven by economic expansion, increased financial inclusion, digitization, and rising demand for retail and corporate banking services.

2. Industry Trends: Technological transformation is a defining trend in Indian banking, with digital banking, mobile wallets, and fintech partnerships reshaping consumer behavior. Banks are investing heavily in AI, blockchain, and cloud computing to enhance customer experience, risk management, and operational efficiency. The COVID-19 pandemic accelerated digital adoption, with increased preference for contactless transactions and online lending platforms. Additionally, there is a growing emphasis on sustainable finance and green banking initiatives. Emerging opportunities lie in expanding credit penetration in underserved rural and semi-urban markets, leveraging data analytics for personalized financial products, and integrating with government schemes promoting digital payments and financial literacy.

3. Regulatory Landscape: The Reserve Bank of India (RBI) is the primary regulator overseeing banking operations, ensuring financial stability, consumer protection, and systemic risk mitigation. Key regulations include capital adequacy norms under Basel III, priority sector lending targets, and stringent asset quality reviews to manage non-performing assets (NPAs). Recent regulatory focus has been on strengthening governance standards, enhancing transparency, and promoting digital security frameworks. Compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) norms remains critical. Policy initiatives such as the Insolvency and Bankruptcy Code (IBC) have improved recovery mechanisms, while the introduction of the Prompt Corrective Action (PCA) framework targets early intervention in weak banks. Regulatory support for fintech integration and open banking APIs is also evolving.

4. Competitive Dynamics: The Indian banking sector is characterized by a mix of large, well-capitalized incumbents and smaller niche players. Barriers to entry are high due to regulatory capital requirements, technology investments, and the need for extensive branch and digital networks. Private sector banks like Yes Bank compete on innovation, customer service, and product diversification to differentiate themselves from PSBs and new fintech entrants. Market positioning is influenced by brand reputation, asset quality, and the ability to manage credit risk effectively. Yes Bank, having undergone restructuring and recapitalization in recent years, is focused on regaining market confidence and expanding its retail and corporate banking footprint. Competitive pressures also come from non-banking financial companies (NBFCs) and digital-only banks, which are capturing segments of the lending and payments markets through agility and technology-driven models.

In summary, the Indian banking sector, particularly private sector banks, operates in a dynamic environment shaped by technological innovation, evolving regulatory frameworks, and intense competition. Growth prospects remain strong, supported by economic development and increasing financial inclusion, but banks must navigate challenges related to asset quality, regulatory compliance, and digital transformation to sustain competitive advantage.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

Financials

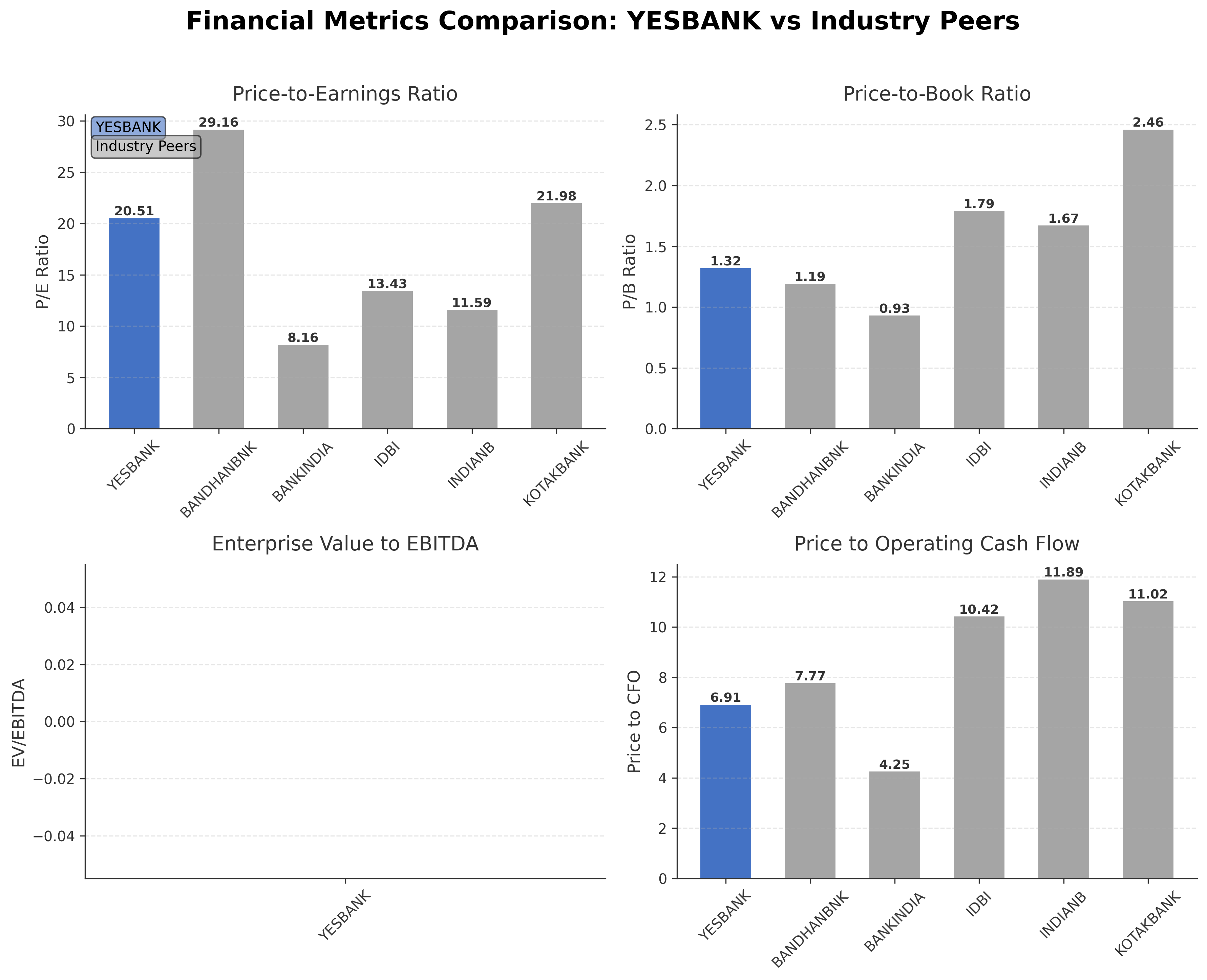

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Yes Bank Ltd. | ₹650.79B | 20.51 | 1.32 | N/A | 6.91 |

| Bandhan Bank Ltd. | ₹293.16B | 29.16 | 1.19 | N/A | 7.77 |

| Bank of India | ₹801.50B | 8.16 | 0.93 | N/A | 4.25 |

| IDBI Bank Ltd. | ₹1.25T | 13.43 | 1.79 | N/A | 10.42 |

| Indian Bank | ₹1.33T | 11.59 | 1.67 | N/A | 11.89 |

| Kotak Mahindra Bank Ltd. | ₹4.13T | 21.98 | 2.46 | N/A | 11.02 |

Comparison Analysis: Yes Bank Ltd. holds a mid-range market capitalization among its Indian regional banking peers, with a P/E ratio of 20.51 that is lower than Bandhan Bank and Kotak Mahindra Bank but higher than Bank of India, IDBI Bank, and Indian Bank. Its price-to-book ratio of 1.32 is moderate, indicating valuation levels below Kotak Mahindra Bank but above Bank of India. The return on equity at 6.53% is lower than most peers, suggesting room for improvement in profitability. The price-to-cash-flow ratio is comparatively lower, which may indicate operational efficiency or valuation differences. Overall, Yes Bank presents a balanced profile with certain valuation advantages but faces competitive pressures in profitability metrics.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 168.30B | 139.78B | 93.70B | 91.17B | 91.35B |

| Operating Expense Selling General And Administrative | 668.87M | 772.36M | 706.13M | 718.54M | 622.30M |

| Operating Expense Other Operating Expenses | 51.70B | 47.31B | 38.54B | 29.37B | 26.34B |

| Pretax Income | 32.24B | 15.38B | 9.81B | 10.64B | -34.89B |

| Income Tax | 7.77B | 2.52B | 2.46B | 3.70B | -12.73B |

| Net Income | 24.47B | 12.85B | 7.36B | 10.64B | -34.89B |

| Eps Basic | 0.79 | 0.45 | 0.28 | 0.42 | -1.65 |

| Eps Diluted | 0.78 | 0.44 | 0.28 | 0.42 | -1.65 |

| Basic Shares Outstanding | 31.15B | 28.76B | 26.16B | 25.05B | 21.18B |

| Diluted Shares Outstanding | 31.15B | 28.76B | 26.16B | 25.05B | 21.18B |

| Net Income Continuous Operations | 32.24B | 15.38B | 9.81B | 14.34B | -47.62B |

| Minority Interests | -1.08M | 0.00 | 0.00 | 0.00 | 0.00 |

Source: Financial statements and regulatory filings

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 655.84B | 634.06B | 502.66B | 639.52B | 119.29B |

| Accounts Receivable | N/A | N/A | N/A | N/A | N/A |

| Total Assets | 4241.16B | N/A | N/A | N/A | N/A |

| Total Liabilities | 3762.80B | N/A | N/A | N/A | N/A |

| Long Term Debt | 708.67B | 788.63B | 710.17B | 652.80B | 585.34B |

| Shareholders Equity | 478.36B | 421.55B | 407.18B | 336.99B | 331.38B |

Source: Financial statements and regulatory filings

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 32.24B | 15.38B | 9.81B | 14.34B | -47.62B |

| Operating Activities Stock Based Compensation | 693.98M | 312.12M | 218.41M | 90.45M | 0.00 |

| Operating Activities Other Non Cash Items | -2.94B | 4.11B | 3.87B | 3.40B | 1.79B |

| Operating Activities Other Assets Liabilities | 64.15B | -145.94B | -122.20B | -36.73B | -12.90B |

| Operating Activities Operating Cash Flow | 94.15B | -126.15B | -108.30B | -18.90B | -58.73B |

| Investing Activities Capital Expenditures | -7.21B | -9.62B | -7.39B | -3.99B | -2.59B |

| Investing Activities Net Acquisitions | 0.00 | N/A | N/A | N/A | N/A |

| Investing Activities Sale Of Investments | 92.49B | N/A | N/A | N/A | N/A |

| Investing Activities Investing Cash Flow | 85.27B | -124.31B | -129.04B | -145.11B | -2.59B |

| Financing Activities Long Term Debt Payments | -85.36B | -2.80B | -17.64B | -14.13B | -498.22B |

| Financing Activities Common Stock Issuance | 28.82B | 171.96M | 60.37B | 635.00K | 148.80B |

| Financing Activities Other Financing Charges | 32.54M | N/A | N/A | 100.00K | 100.00K |

| Financing Activities Financing Cash Flow | -56.51B | 27.71B | 114.50B | 83.91B | -349.42B |

| End Cash Position | 285.67B | 193.18B | 193.56B | 467.48B | 293.25B |

| Free Cash Flow | 56.45B | 86.64B | -266.08B | 231.87B | 551.26B |

| Investing Activities Purchase Of Investments | N/A | -114.69B | -121.65B | -141.13B | N/A |

| Financing Activities Long Term Debt Issuance | N/A | 30.34B | 71.78B | 98.04B | 0.00 |

| Investing Activities Other Investing Activity | N/A | N/A | -100.00K | N/A | -100.00K |

| Financing Activities Common Dividends | N/A | N/A | N/A | N/A | N/A |

Source: Financial statements and regulatory filings

Technical Analysis

Key Insights

- The current trend shows a consolidation phase with the stock price hovering near the 50-day and 200-day moving averages around ₹21.65 and ₹21.20 respectively, indicating a neutral to slightly bullish momentum.

- Key support levels are identified near ₹16.02 (52-week low) and ₹20.00, while resistance is observed near ₹24.30 (52-week high) and ₹22.50.

- The stock price is currently slightly below the 50-day moving average and near the 200-day moving average, suggesting mixed signals in trend strength.

- Momentum indicators show RSI near neutral levels, MACD indicating a potential crossover, and stochastic oscillators reflecting moderate momentum without extreme overbought or oversold conditions.

- Multi-timeframe analysis reveals that daily charts show sideways movement, weekly charts indicate a mild uptrend, and monthly charts suggest longer-term consolidation.

- Potential market scenarios include a breakout above resistance levels leading to renewed upward momentum or a breakdown below support triggering further consolidation or decline.

Trending News

1. Headline: YESBANK.NS Stock Today: ED Grills Anil Ambani Again on February 27 | Meyka

Summary: Anil Ambani ED action intensifies: home worth ₹3,716 crore attached and fresh Feb 27 summons in the Yes Bank loan fraud case. Impact on YESBANK.NS today, key levels, risks, and what to watch.

Sentiment: negative

2. Headline: Yes Bank Ltd. Sees Exceptional Volume Amidst Market Underperformance

Summary: Yes Bank Ltd., a prominent player in the private sector banking space, witnessed one of the highest trading volumes on 27 Feb 2026, despite registering a modest decline in its share price. The stock’s volume surge, coupled with its underperformance relative to sector and benchmark indices, ...

Sentiment: positive

3. Headline: YES BANK LTD. - Share Price | Ratios | BSE/NSE Performance | Live Stock Quote

Summary: Get YES Bank Ltd. live share price, historical charts, volume, market capitalisation, market performance, reports and other company details.

Sentiment: neutral

4. Headline: Yes Bank details investor meetings at Kotak ‘Chasing Growth 2026’ conference - TipRanks.com

Summary: Yes Bank Limited ( ($IN:YESBANK) ) has provided an announcement. Yes Bank Limited, a leading private sector lender in India, continues to position itself as an acti...

Sentiment: neutral

5. Headline: Yes Bank Investigates $0.28 Million Forex Card Fraud in Latin America

Summary: Yes Bank has reported a $0.28 million fraud involving its forex card in Latin America, raising concerns about security protocols.

Sentiment: negative

6. Headline: teiss - News - Yes Bank and BookMyForex refute data breach concerns amid fraudulent transactions

Summary: India’s Yes Bank says it is investigating thousands of unauthorised overseas transactions on Indian customer’s foreign exchange cards that inflicted losses of about $280,000 on 5000 customers. ... © 2025, Lyonsdown Limited. teiss® is a registered trademark of Lyonsdown Ltd.

Sentiment: negative

7. Headline: Yes Bank Detects $280,000 Fraud in Forex Card Transactions | Headlines

Summary: Yes Bank reported unauthorized transactions worth $280,000 on its multi-currency prepaid forex cards, linked to 15 merchants in Latin America. The bank's monitoring systems declined 688 fraudulent attempts, saving $100,000. Following a major stake acquisition by SMBC, Yes Bank is taking measures ...

Sentiment: positive

8. Headline: Yes Bank details limited impact of unauthorized forex card transactions - TipRanks.com

Summary: Yes Bank Limited ( ($IN:YESBANK) ) just unveiled an announcement. Yes Bank has clarified that its multi-currency prepaid forex cards, issued in partnership with Boo...

Sentiment: neutral

9. Headline: YES Bank shares climb despite forex card data breach; analysts divided on near term trend - BusinessToday

Summary: Shares of YES Bank Ltd traded higher in Thursday's late morning session, even as the private sector lender disclosed a data breach involving its BookMyForex multi-currency forex card.

Sentiment: positive

Summary: Yes Bank Ltd NSE:YESBANK:

Sentiment: negative

Recent Updates

News Summary

Recent news for Yes Bank Ltd. highlights a mix of operational updates and market activity. The bank clarified limited impact from unauthorized forex card transactions, addressing security concerns. Trading volumes surged despite some price underperformance, indicating active market interest. Sumitomo Mitsui Financial Group is considering an additional $1.1 billion investment, signaling strategic support. Leadership changes include the appointment of a new Managing Director, reflecting governance adjustments. Market analysts advise caution on the near-term outlook amid these developments. Overall, the news cycle centers on risk management, capital infusion prospects, and strategic positioning within the competitive Indian banking sector.

News Sentiment

Sentiment across recent updates is mixed to neutral, with positive signals from strategic investments and volume activity balanced against concerns over fraud incidents and cautious analyst views. The narrative suggests a market environment attentive to operational risks while recognizing potential growth catalysts from institutional backing and leadership renewal.

Analytical Overview

Analysis Summary

Yes Bank’s valuation metrics, including a trailing P/E of 20.51 and forward P/E of 15.62, are slightly above the industry average of 20.51, indicating a valuation in line with sector norms but with potential for re-rating given growth prospects. The price-to-book ratio of 1.32 suggests moderate valuation relative to book value.

The bank demonstrates a positive growth trajectory with quarterly revenue growth of 17.4% and a strong year-over-year earnings growth of 54.4%. Operating cash flow remains robust at approximately ₹94.15 billion, supporting sustainable business operations.

Financial health shows a total debt-to-equity ratio of 1.27, reflecting leverage typical for the banking sector, with substantial cash reserves of nearly ₹199 billion. Free cash flow is positive, supporting liquidity and operational flexibility.

Sector-specific challenges include regulatory scrutiny and fraud risks, as evidenced by recent forex card incidents, while opportunities lie in digital transformation and expanding financial inclusion in India’s evolving banking landscape.

The Indian market environment features a dynamic regulatory framework, increasing digital adoption, and a growing economy, all influencing Yes Bank’s competitive positioning and strategic initiatives.

Investment Conclusion

Supporting Factors: Primary supporting factors include solid revenue and earnings growth, strong operating cash flow, and ongoing institutional interest from major investors like SMFG.

Risk Factors: Main risk factors encompass regulatory challenges, operational risks from fraud incidents, and competitive pressures within the Indian banking sector.

SWOT Analysis

Strengths

- Strong revenue growth with 17.4% quarterly increase.

- Robust operating cash flow of ₹94.15 billion supports liquidity.

- Significant insider ownership at 44.18% indicates aligned management interests.

- Emphasis on digital transformation enhances customer experience.

Weaknesses

- Return on equity at 6.53% is lower than many peers.

- Total debt-to-equity ratio of 1.27 reflects elevated leverage.

- Recent forex card fraud incidents raise operational risk concerns.

- Dividend yield is relatively low at 0.10%.

Opportunities

- Potential additional investment of $1.1 billion from SMFG could strengthen capital base.

- Growing Indian banking sector with increasing digital adoption.

- Expansion in retail and SME segments offers growth avenues.

- Regulatory support for financial inclusion may drive new business.

Threats

- Regulatory scrutiny related to loan fraud cases may impact reputation.

- Competitive pressures from established banks and fintech disruptors.

- Market volatility could affect share price stability.

- Operational risks from fraud and cybersecurity incidents.

Company Description

Yes Bank Ltd. is a prominent private sector financial institution in India, offering a comprehensive suite of banking products and services. Founded in 2004, the bank provides a robust platform for various financial solutions, including corporate financing, wealth management, investment banking, and retail banking services. Yes Bank plays a crucial role in supporting multiple sectors, with particular emphasis on fostering digital transformation and financial innovation in the banking space. Its service framework is designed to meet the diverse needs of small to medium enterprises, large corporations, and retail customers. The bank is well-regarded for its emphasis on using technology to enhance customer experience and operational efficiency. Yes Bank's approach to risk management and corporate governance has helped it navigate the Indian banking landscape challenges effectively. By actively participating in financial inclusion and sustainable development, Yes Bank Ltd. holds significant market influence in India's banking sector, contributing to the country’s economic growth and connecting disparate financial ecosystems.