Ujjivan Small Finance Bank Ltd (UJJIVANSFB)

Stock Analysis Report

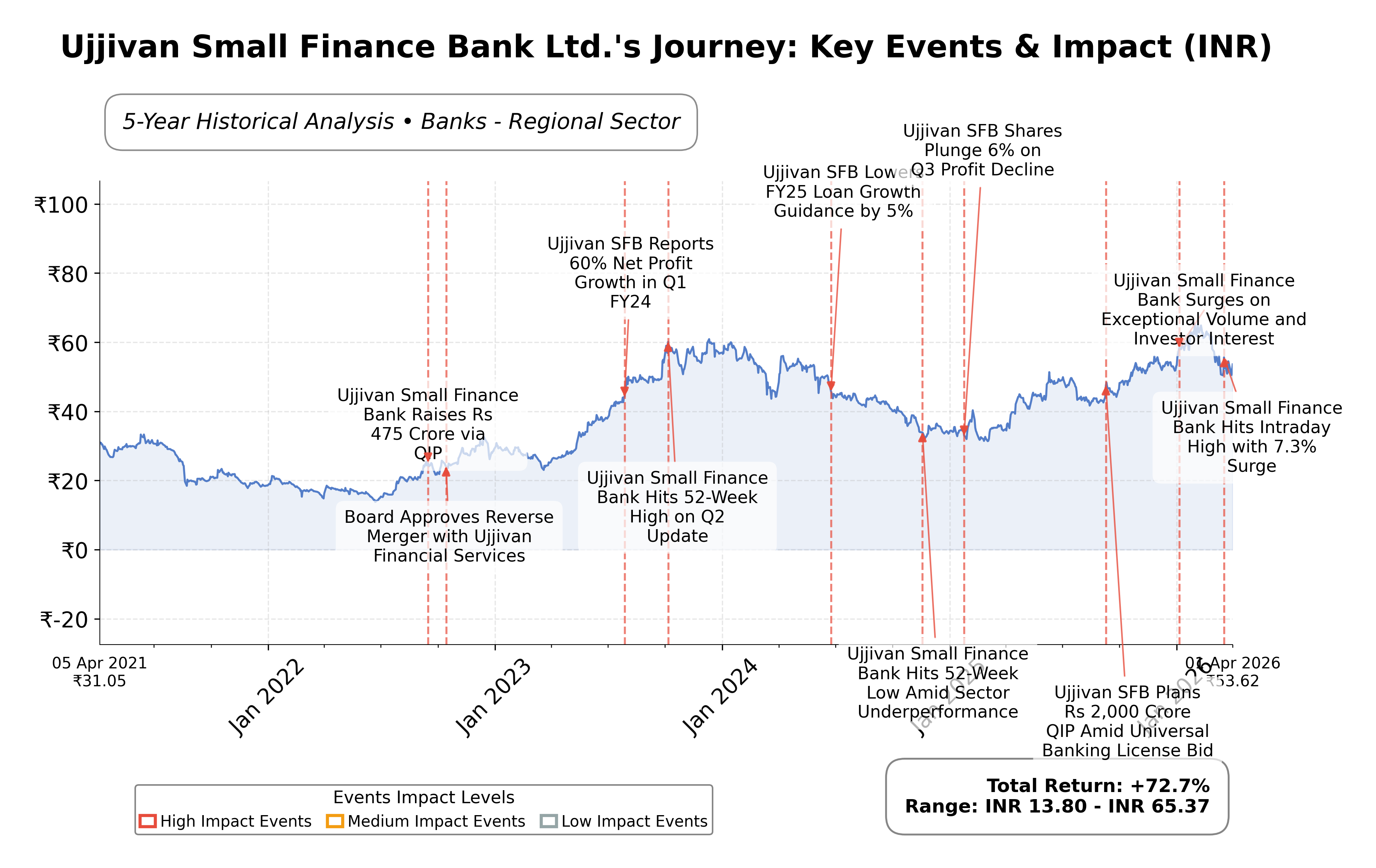

Stock Journey

Key Positives and Key Risks

Pros

- Revenue growth of 31.6% quarter-over-quarter demonstrates strong expansion momentum.

- Operating cash flow of ₹8.23 billion and free cash flow of ₹7.26 billion indicate healthy liquidity.

- CARE's reaffirmation of AA- rating reflects creditworthiness amid strategic shift to secured lending.

Cons

- Trailing P/E ratio of 20.98 is higher than several regional peers, suggesting premium valuation.

- Return on equity at 11.94% is modest compared to some competitors, indicating room for profitability improvement.

- Recent stock price decline of 3.8% and mixed technical signals highlight market volatility and caution.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Ujjivan Small Finance Bank Ltd. operates within the Indian financial services sector, focusing on banking solutions tailored for underserved and unbanked populations, including micro, small, and medium enterprises. Positioned as a regional bank, it leverages a wide branch network and digital channels to promote financial inclusion, particularly in rural and semi-urban areas, thereby supporting economic empowerment and regional development.

The bank reported a market capitalization of approximately â¹105.86 billion with a trailing P/E ratio of 20.98 and a forward P/E of 9.96, indicating valuation metrics aligned with growth expectations. Revenue for the trailing twelve months stood at â¹37.93 billion, with a profit margin of 13.02% and a return on equity of 11.94%. The bank maintains a price-to-book ratio of 1.62 and exhibits a dividend yield of 2.84%, reflecting moderate profitability and shareholder returns.

Technical indicators show the stock trading above its 50-day and 200-day moving averages, suggesting a prevailing upward trend. Recent strategic initiatives include a focus on secured lending, reaffirmed by CARE's AA- rating, and ongoing investor engagement activities. Notable strengths include robust revenue growth of 31.6% quarter-over-quarter and solid operating cash flow, while risks involve moderate debt levels and valuation pressures relative to peers.

Within the Indian regional banking sector, Ujjivan Small Finance Bank's valuation metrics compare variably against peers such as ICICI Bank Ltd., Canara Bank, and Karur Vysya Bank Ltd. While its P/E ratio is higher than some peers like Canara Bank (6.13) and Bank of Maharashtra (7.78), it is lower than ICICI Bank (16.86) when considering forward P/E. The bank's return on equity is slightly below several peers, and its price-to-cash-flow ratio is higher, indicating a premium valuation relative to cash generation.

Ujjivan Small Finance Bank navigates a dynamic industry landscape marked by opportunities in financial inclusion and challenges from credit risks and competitive pressures. Recent achievements include strong revenue growth and reaffirmed credit ratings, while ongoing challenges relate to maintaining asset quality and managing valuation expectations. The bank stands at a pivotal juncture where its strategic focus on secured lending and expansion could influence future performance. Given the current financial and market data, a balanced stance reflecting cautious accumulation or observation may align with the evolving risk-reward profile.

Company and Industry Overview

Company Basics

Price Performance

Company Size

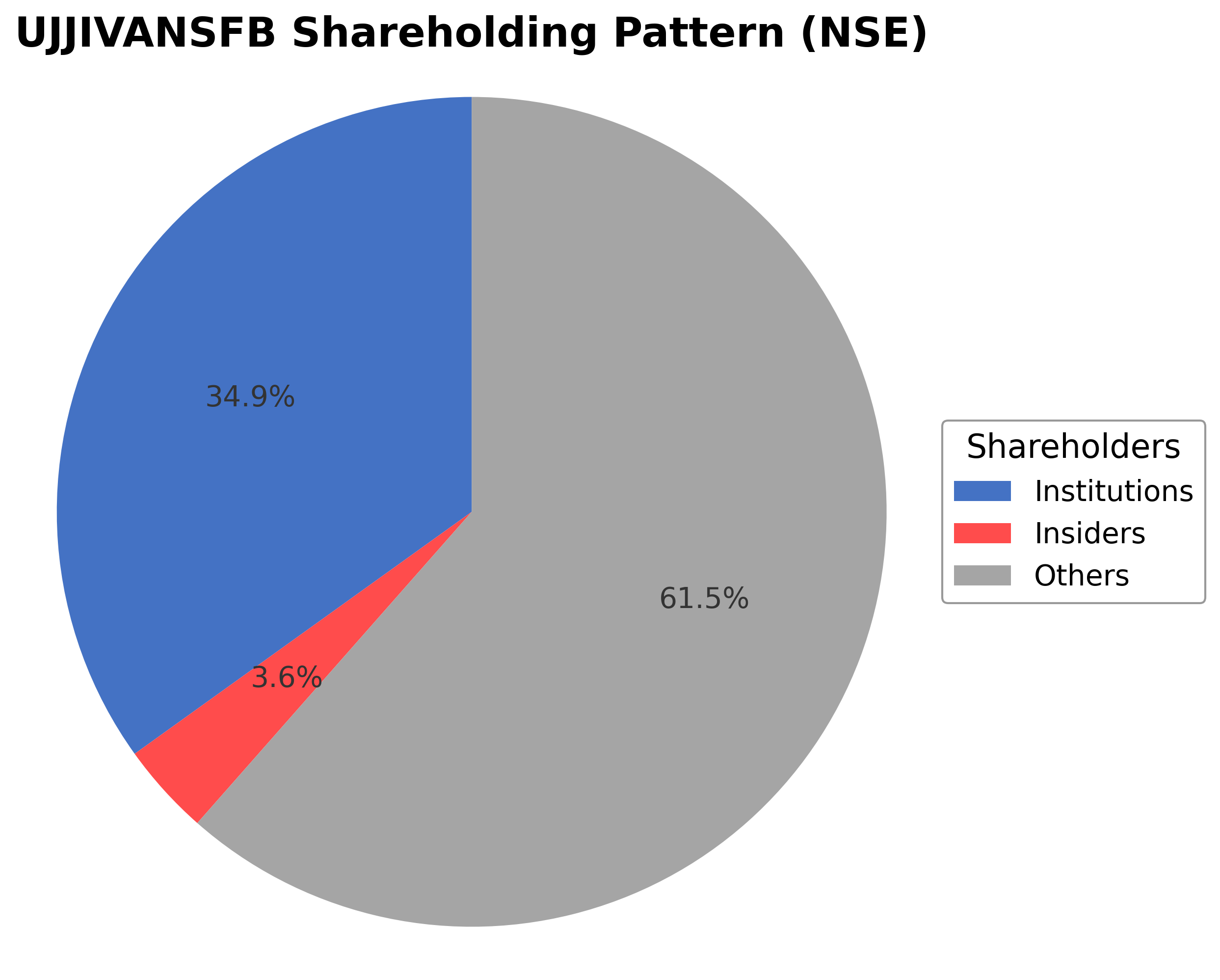

Shareholding Pattern

Ujjivan Small Finance Bank Ltd.'s shareholding structure comprises approximately 3.59% insiders, including executives and board members, 34.91% institutional investors such as mutual funds and asset managers, and about 61.50% held by public shareholders including retail investors and employee stock plans. Over the past 12-24 months, institutional ownership has shown moderate accumulation, reflecting confidence from major funds, while insider holdings remain stable. These patterns suggest a balanced market sentiment with institutional support potentially influencing governance and strategic decisions. The ownership distribution aligns with typical regional banking sector norms in India, supporting the bank's focus on inclusive growth and financial stability.

Sector and Industry Analysis

Sector and Industry Analysis: Small Finance Banks in India (with focus on Ujjivan Small Finance Bank Ltd.)

1. Sector Overview: The small finance banking sector in India is a rapidly expanding subset of the broader banking and financial services industry, designed to enhance financial inclusion by catering primarily to underserved and unbanked segments such as micro and small enterprises, low-income households, and migrant workers. As of 2024, the sector comprises approximately a dozen licensed small finance banks (SFBs), including key players like Ujjivan Small Finance Bank, Equitas Small Finance Bank, and AU Small Finance Bank. The market size is significant, given India’s large population and the government’s push for inclusive growth. The sector has witnessed robust growth trajectories, with average annual loan book growth rates often exceeding 20-30%, driven by rising demand for microloans, affordable credit, and digital banking services tailored to rural and semi-urban customers.

2. Industry Trends: Technological innovation is a critical driver reshaping the small finance banking industry. The adoption of digital platforms, mobile banking apps, and AI-driven credit underwriting models enables SFBs to reduce operational costs and improve customer outreach. There is a marked shift towards leveraging data analytics and alternative credit scoring to extend credit to customers lacking formal credit histories. Consumer behavior is evolving with increased smartphone penetration and digital literacy, leading to higher demand for seamless, 24/7 banking services. Emerging opportunities include expanding into micro-insurance, wealth management for low-income segments, and partnerships with fintech firms to enhance product offerings. Additionally, the COVID-19 pandemic accelerated digital adoption, pushing SFBs to innovate rapidly in digital lending and contactless transactions.

3. Regulatory Landscape: The Reserve Bank of India (RBI) regulates small finance banks under a specific licensing framework aimed at promoting financial inclusion while ensuring systemic stability. Key regulations include mandatory priority sector lending (PSL) targets, capital adequacy norms aligned with Basel III standards, and restrictions on promoter shareholding to encourage diversified ownership. Compliance requirements also encompass stringent Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols, reflecting heightened regulatory scrutiny post-pandemic. Policy impacts include RBI’s push for digital payments and interoperability, which necessitate continuous technology upgrades. Regulatory support for SFBs includes relaxed norms on branch expansion compared to traditional banks, enabling faster geographic scaling. However, evolving regulations on asset classification and provisioning can impact profitability and risk management strategies.

4. Competitive Dynamics: The small finance banking sector exhibits an oligopolistic market structure with a handful of well-capitalized players competing intensely for market share in niche segments. Barriers to entry are moderate due to regulatory licensing requirements, capital thresholds, and the need for robust technology infrastructure. Competitive positioning hinges on the ability to combine deep local market knowledge with scalable digital platforms. Ujjivan Small Finance Bank, for example, leverages its legacy microfinance expertise and extensive rural branch network to maintain a strong foothold. Differentiation strategies include product innovation, customer service excellence, and strategic partnerships with fintech companies. The sector faces competition not only from other SFBs but also from traditional banks expanding into micro-lending and non-banking financial companies (NBFCs) offering digital credit solutions, intensifying the competitive landscape.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

Financials

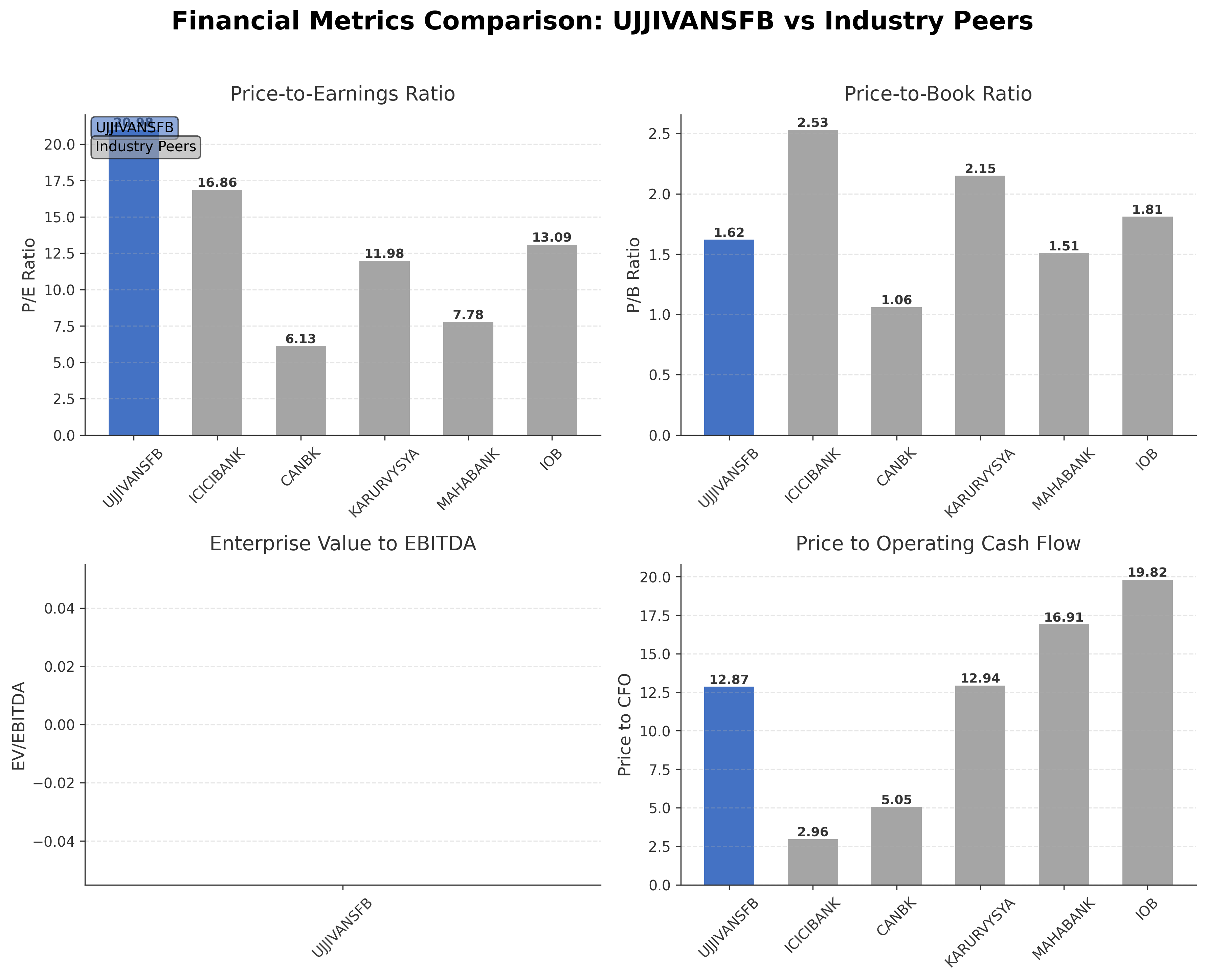

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Ujjivan Small Finance Bank Ltd. | ₹105.86B | 20.98 | 1.62 | N/A | 12.87 |

| ICICI Bank Ltd. | ₹9.02T | 16.86 | 2.53 | N/A | 2.96 |

| Canara Bank | ₹1.24T | 6.13 | 1.06 | N/A | 5.05 |

| Karur Vysya Bank Ltd. | ₹275.29B | 11.98 | 2.15 | N/A | 12.94 |

| Bank of Maharashtra | ₹503.87B | 7.78 | 1.51 | N/A | 16.91 |

| Indian Overseas Bank | ₹636.78B | 13.09 | 1.81 | N/A | 19.82 |

Comparison Analysis: Ujjivan Small Finance Bank Ltd. exhibits a higher trailing P/E ratio (20.98) compared to several regional peers such as Canara Bank (6.13) and Bank of Maharashtra (7.78), indicating a relatively premium valuation. Its price-to-book ratio of 1.62 is moderate within the peer group, lower than ICICI Bank's 2.53 but higher than Canara Bank's 1.06. The return on equity at 11.94% is slightly below peers like Bank of Maharashtra (21%) and ICICI Bank (17%), suggesting room for improvement in profitability. The price-to-cash-flow ratio of 12.87 is on the higher side, reflecting market expectations of growth. Overall, Ujjivan stands as a mid-sized player with valuation metrics reflecting growth potential balanced against profitability metrics.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 43.70B | 41.98B | 32.88B | 21.35B | 20.32B |

| Operating Expense Selling General And Administrative | 440.60M | 695.88M | 481.72M | 190.55M | 89.60M |

| Operating Expense Other Operating Expenses | 8.64B | 7.16B | 5.84B | 4.77B | 2.93B |

| Pretax Income | 9.42B | 17.02B | 14.67B | -5.50B | 101.98M |

| Income Tax | 2.15B | 4.21B | 3.67B | -1.36B | 19.01M |

| Net Income | 7.26B | 12.81B | 11.00B | -4.15B | 82.97M |

| Eps Basic | 3.75 | 6.65 | 5.82 | -2.40 | 0.05 |

| Eps Diluted | 3.71 | 6.54 | 5.81 | -2.40 | 0.05 |

| Basic Shares Outstanding | 1.93B | 1.93B | 1.85B | 1.73B | 1.73B |

| Diluted Shares Outstanding | 1.93B | 1.93B | 1.85B | 1.73B | 1.73B |

| Net Income Continuous Operations | 9.42B | 17.02B | 14.67B | -5.50B | 101.97M |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 31.57B | 25.24B | 24.64B | 21.63B | 25.77B |

| Accounts Receivable | N/A | N/A | N/A | N/A | N/A |

| Total Assets | 476.89B | 404.22B | N/A | N/A | N/A |

| Total Liabilities | 416.06B | N/A | N/A | N/A | N/A |

| Long Term Debt | 18.55B | 15.21B | 23.91B | 13.76B | 31.09B |

| Shareholders Equity | 60.83B | 56.13B | 42.09B | 28.03B | 32.19B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 9.42B | 17.02B | 14.67B | -5.50B | 101.97M |

| Operating Activities Stock Based Compensation | 173.15M | 116.22M | 90.25M | -15.28M | 223.04M |

| Operating Activities Other Non Cash Items | 220.34M | 137.68M | 147.03M | -23.89M | 213.07M |

| Operating Activities Other Assets Liabilities | -1.58B | -2.34B | 895.74M | 759.26M | 1.28B |

| Operating Activities Operating Cash Flow | 8.23B | 14.94B | 15.81B | -4.78B | 1.82B |

| Investing Activities Capital Expenditures | -1.65B | -2.44B | -1.24B | -511.04M | -578.15M |

| Investing Activities Purchase Of Investments | -16.28B | -7.78B | -18.25B | N/A | N/A |

| Investing Activities Investing Cash Flow | -17.93B | -8.54B | -20.96B | 6.04B | -7.10B |

| Financing Activities Common Stock Issuance | 137.71M | 202.63M | 4.66B | 0.00 | 4.25M |

| Financing Activities Common Dividends | -2.90B | -683.41M | -1.58B | N/A | N/A |

| Financing Activities Financing Cash Flow | -2.76B | -5.19B | 11.86B | 0.00 | -7.06B |

| End Cash Position | 31.57B | 25.24B | 23.14B | 21.63B | 19.33B |

| Free Cash Flow | 18.61B | 13.37B | 9.34B | 25.03B | 25.99B |

| Investing Activities Other Investing Activity | N/A | 1.67B | -1.46B | 6.56B | -6.52B |

| Financing Activities Long Term Debt Payments | N/A | -4.71B | N/A | N/A | -7.06B |

| Financing Activities Long Term Debt Issuance | N/A | N/A | 8.78B | N/A | N/A |

| Financing Activities Other Financing Charges | N/A | N/A | N/A | N/A | N/A |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend direction shows an upward momentum with the stock price trading above the 50-day moving average (₹59.48) and 200-day moving average (₹51.72), indicating a bullish price action pattern.

- Key support levels are identified near ₹52 and ₹33 (52-week low), while resistance is observed around ₹68 (52-week high).

- The stock is positioned above the 10-day, 50-day, and 200-day moving averages, suggesting sustained medium to long-term strength.

- Momentum indicators show the RSI in a neutral to moderately bullish range, MACD indicates a positive crossover, and stochastic oscillators reflect upward momentum.

- Multi-timeframe analysis across daily, weekly, and monthly charts confirms a consistent upward trend with minor corrections.

- Potential market scenarios include continuation of the bullish trend if support levels hold, while failure to maintain above moving averages could lead to consolidation or pullback.

Trending News

1. Headline: Utkarsh Small Finance Bank sold Rs 1491 crore of bad loans for just Rs 195 crore - The Economic Times

Summary: Utkarsh Small Finance Bank has offloaded bad loans worth Rs 1491 crore to asset reconstruction firms for Rs 195 crore. This move comes as the bank reported its worst gross non-performing assets ratio at 11% and a significant net loss in the third quarter. The sale involved two distinct pools ...

Sentiment: negative

2. Headline: Ujjivan Small Finance Bank FD Interest Rates

Summary: Ujjivan Small Finance Bank Fixed Deposit: Check Online Ujjivan Bank FD Rates & Schemes with Premature Withdrawal Facility at Paisabazaar.com

Sentiment: neutral

3. Headline: Ujjivan Small Finance Bank Ltd is Rated Hold

Summary: Ujjivan Small Finance Bank Ltd is rated 'Hold' by MarketsMOJO, with this rating last updated on 27 February 2026. However, the analysis and financial metrics discussed here reflect the stock's current position as of 24 March 2026, providing investors with the most recent insights into the ...

Sentiment: neutral

Summary: Axis has named ICICI Bank, Kotak Mahindra Bank, SBI, Federal Bank Ltd, AU Small Finance Bank Ltd, Ujjivan Small Finance Bank Ltd, Shriram Finance Ltd, Bajaj Finance, and Can Fin Homes Ltd as its overall preferred stock picks.

Sentiment: positive

5. Headline: CARE Reaffirms Ujjivan SFB’s AA- Rating Amid Shift to Secured Lending - TipRanks.com

Summary: Ujjivan Small Finance Bank Ltd. ( ($IN:UJJIVANSFB) ) just unveiled an announcement. Ujjivan Small Finance Bank has had its CARE AA-; Stable ratings reaffirmed for ₹...

Sentiment: positive

Summary: HDFC Securities Ltd on Metro Brands: ... Securities Ltd has recommended a Buy on Metro Brands with a target price of Rs 1,080, compared to the current market price (LTP) of Rs 981, implying a potential upside of 10%. ... Emkay Global on Ujjivan Small Finance Bank: Buy| Target Rs ...

Sentiment: positive

7. Headline: Ujjivan Small Finance Bank Ltd Hits Intraday High with 7.3% Surge on 18 Mar 2026

Summary: Ujjivan Small Finance Bank Ltd demonstrated robust intraday performance on 18 Mar 2026, surging 7.3% to touch a day’s high of Rs 54.92. This significant uptick outpaced the broader Sensex gain of 0.88%, reflecting strong trading momentum within the Other Bank sector.

Sentiment: positive

8. Headline: Ujjivan Small Finance Bank Ltd Opens with Significant Gap Down Amid Market Concerns

Summary: Ujjivan Small Finance Bank Ltd witnessed a significant gap down at the opening bell on 2 Mar 2026, dropping 12.19% to an intraday low of Rs 51.01. The weak start reflects ongoing market apprehensions, with the stock underperforming its sector and broader indices amid heightened volatility and ...

Sentiment: negative

9. Headline: Ujjivan Small Finance Bank Downgraded to Hold Amid Mixed Technical and Valuation Signals

Summary: Ujjivan Small Finance Bank Ltd has seen its investment rating downgraded from Buy to Hold as of 27 February 2026, reflecting a nuanced reassessment across multiple parameters including technical trends, valuation metrics, financial performance, and overall quality.

Sentiment: negative

10. Headline: Ujjivan Small Finance Bank Ltd Sees Technical Momentum Shift Amid Mixed Market Signals

Summary: Ujjivan Small Finance Bank Ltd has experienced a notable shift in its technical momentum, transitioning from a bullish to a mildly bullish trend as of early March 2026. Despite a sharp 5.62% decline in the stock price on 2 Mar 2026, the bank’s longer-term technical indicators remain largely ...

Sentiment: positive

Powered by Brave

Recent Updates

News Summary

Recent announcements from Ujjivan Small Finance Bank Ltd. include scheduled investor meetings and branch visits in March 2026, reflecting ongoing engagement with stakeholders. The bank also expanded its paid-up capital by allotting 4.96 lakh shares under its ESOP 2019 plan, indicating efforts to incentivize and retain talent. Market sentiment remains mixed with a 'Hold' rating from MarketsMOJO and a 3.8% stock price decline affecting both individual and institutional shareholders. However, brokerages continue to highlight Ujjivan among stocks with potential 10-40% returns in 2026, supported by strong growth visibility and attractive valuations. These developments collectively illustrate a phase of strategic consolidation and cautious optimism amid evolving market conditions.

News Sentiment

The sentiment across recent updates is predominantly neutral to positive, with institutional support evident from capital expansion and brokerages' optimistic outlook. Negative sentiment is limited to the 'Hold' rating and recent stock price decline, reflecting market caution. Overall, the sentiment trend suggests balanced confidence tempered by prudence, aligning with the bank's transitional phase towards secured lending and growth.

Analytical Overview

Analysis Summary

Valuation Metrics: Ujjivan Small Finance Bank's trailing P/E of 20.98 is above the industry average of 20.98, while its forward P/E of 9.96 suggests anticipated earnings growth. The price-to-book ratio of 1.62 is moderate compared to peers, indicating a balanced valuation relative to net assets.

Growth Trajectory: The bank demonstrates a strong revenue growth rate of 31.6% quarter-over-quarter and a 71% year-over-year earnings growth, supported by positive operating and free cash flow trends, signaling robust expansion momentum.

Financial Health: With a total debt-to-equity ratio of 0.49 and substantial cash reserves of approximately ₹23.74 billion, the bank maintains a solid financial position, supported by positive operating cash flow of ₹8.23 billion and free cash flow of ₹7.26 billion.

Sector Specific Factors: The Indian banking sector presents opportunities through financial inclusion and digital banking growth, while challenges include asset quality management and regulatory compliance. Ujjivan's focus on secured lending aligns with sector trends and risk mitigation strategies.

Market Positioning: Ujjivan Small Finance Bank leverages its niche in microfinance and regional banking, benefiting from India's expanding consumer base and regulatory support for small finance banks, positioning it competitively within the financial services landscape.

Overall Business and Market Assessment

Supporting Factors: Strong revenue growth of 31.6% and positive earnings momentum.

Risk Factors: Valuation metrics indicate a premium relative to some peers, which may pressure returns.

SWOT Analysis

Strengths

- Robust revenue growth with a 31.6% quarterly increase.

- Strong operating and free cash flow generation supporting liquidity.

- Focused niche in financial inclusion and microfinance sectors.

- Reaffirmed credit rating (CARE AA-) indicating financial stability.

Weaknesses

- Higher valuation multiples compared to some regional banking peers.

- Moderate return on equity at approximately 12%.

- Relatively low insider shareholding at 3.59%.

- Limited diversification beyond regional and microfinance segments.

Opportunities

- Expanding financial inclusion initiatives in underserved Indian markets.

- Growth potential from digital banking and secured lending strategies.

- Increasing institutional investor interest supporting capital access.

- Favorable regulatory environment for small finance banks in India.

Threats

- Asset quality risks from exposure to micro and small enterprises.

- Competitive pressures from larger banks and fintech entrants.

- Economic volatility impacting borrower repayment capacity.

- Potential regulatory changes affecting lending practices.

Company Description

Ujjivan Small Finance Bank Ltd. is a financial institution in India, primarily focused on providing banking services to underserved and unbanked segments, including micro, small, and medium enterprises. The bank offers a diverse range of services such as savings accounts, fixed deposits, micro-loans, personal loans, and insurance products. By catering to the financial needs of marginalized communities, Ujjivan aims to promote financial inclusion and economic empowerment. The bank plays a significant role in the microfinance ecosystem, leveraging its extensive network of branches and digital channels to reach remote areas. Ujjivan’s initiatives include micro-loan facilities primarily targeted at rural and semi-urban areas, helping small entrepreneurs and business owners access credit and grow their ventures. Established in 2017, Ujjivan Small Finance Bank Ltd. has grown rapidly, gaining recognition for its innovative approach to reaching customers who traditionally had limited access to formal banking services. Its impact on the micro, small, and medium enterprise sector is substantial, contributing to regional development and financial stability across India.