Stove Kraft Ltd (STOVEKRAFT)

Stock Analysis Report

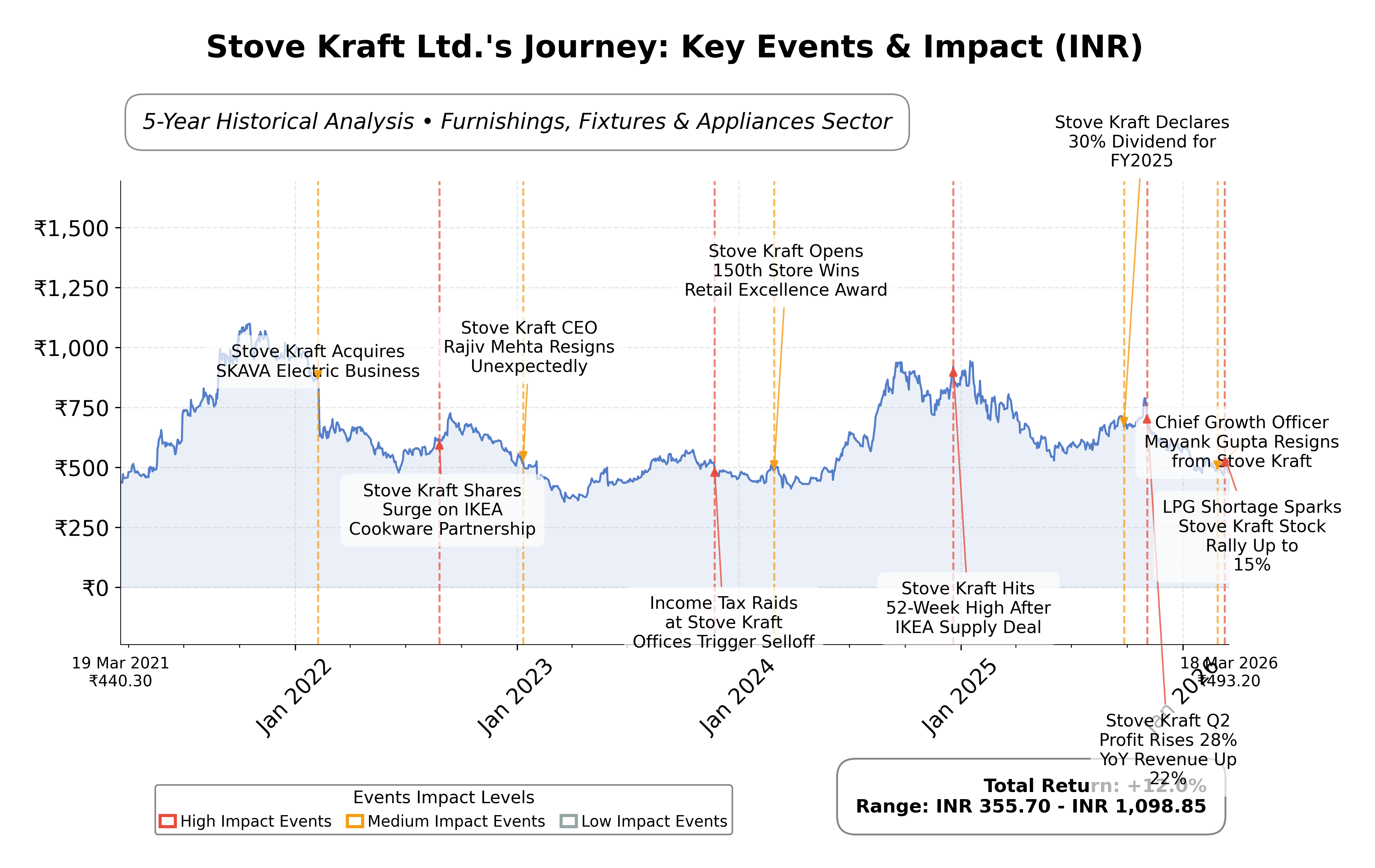

Stock Journey

Key Positives and Key Risks

Pros

- Market capitalization of ₹16.33 billion positions Stove Kraft as a significant mid-cap player within the Indian household appliances sector.

- Positive operating cash flow of ₹621.54 million and free cash flow of ₹385.05 million indicate operational resilience and liquidity.

- Forward P/E ratio of 26.27 suggests potential valuation improvement relative to the current trailing P/E of 43.72.

Cons

- Quarterly revenue growth declined by 6.4%, and quarterly earnings growth fell by 65.8%, signaling near-term performance challenges.

- Debt-to-equity ratio of 52.58% reflects moderate leverage, which could constrain financial flexibility.

- Profit margin remains low at approximately 2.48%, indicating limited profitability despite revenue scale.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Stove Kraft Ltd. is a prominent player in the household appliances sector, specializing in the design, manufacturing, and marketing of kitchen and home solutions. The company offers a broad portfolio of products including cooktops, chimneys, pressure cookers, mixers, and grinders under established brands like Pigeon and Gilma. Operating primarily in India with a growing international presence, Stove Kraft is positioned as a market leader catering to evolving consumer needs driven by urbanization and lifestyle changes.

Financially, Stove Kraft reports a market capitalization of approximately â¹16.33 billion and an enterprise value near â¹18.93 billion. The companyâs trailing P/E ratio stands at 43.72, with a forward P/E of 26.27, reflecting valuation metrics above the industry average. Revenue for the trailing twelve months is â¹15.06 billion, with a modest profit margin of 2.48% and operating margin of 3.55%. Return on equity is 8.18%, and the company maintains a price-to-book ratio of 3.30. The balance sheet shows total assets of â¹12.04 billion and a debt-to-equity ratio of 52.58%, with cash reserves of â¹29.46 million.

Technical indicators reveal a current stock price of â¹518.65, below the 200-day moving average of â¹600.44 and the 50-day moving average of â¹509.05, indicating mixed momentum. Recent strategic initiatives include capitalizing on increased demand for induction cooktops amid LPG shortages, although quarterly revenue and earnings growth have declined. Key strengths include strong brand recognition and manufacturing capabilities, while risks involve supply chain pressures, competitive intensity, and a relatively high valuation. Leadership changes were not highlighted, but market sentiment reflects cautious optimism given recent price volatility.

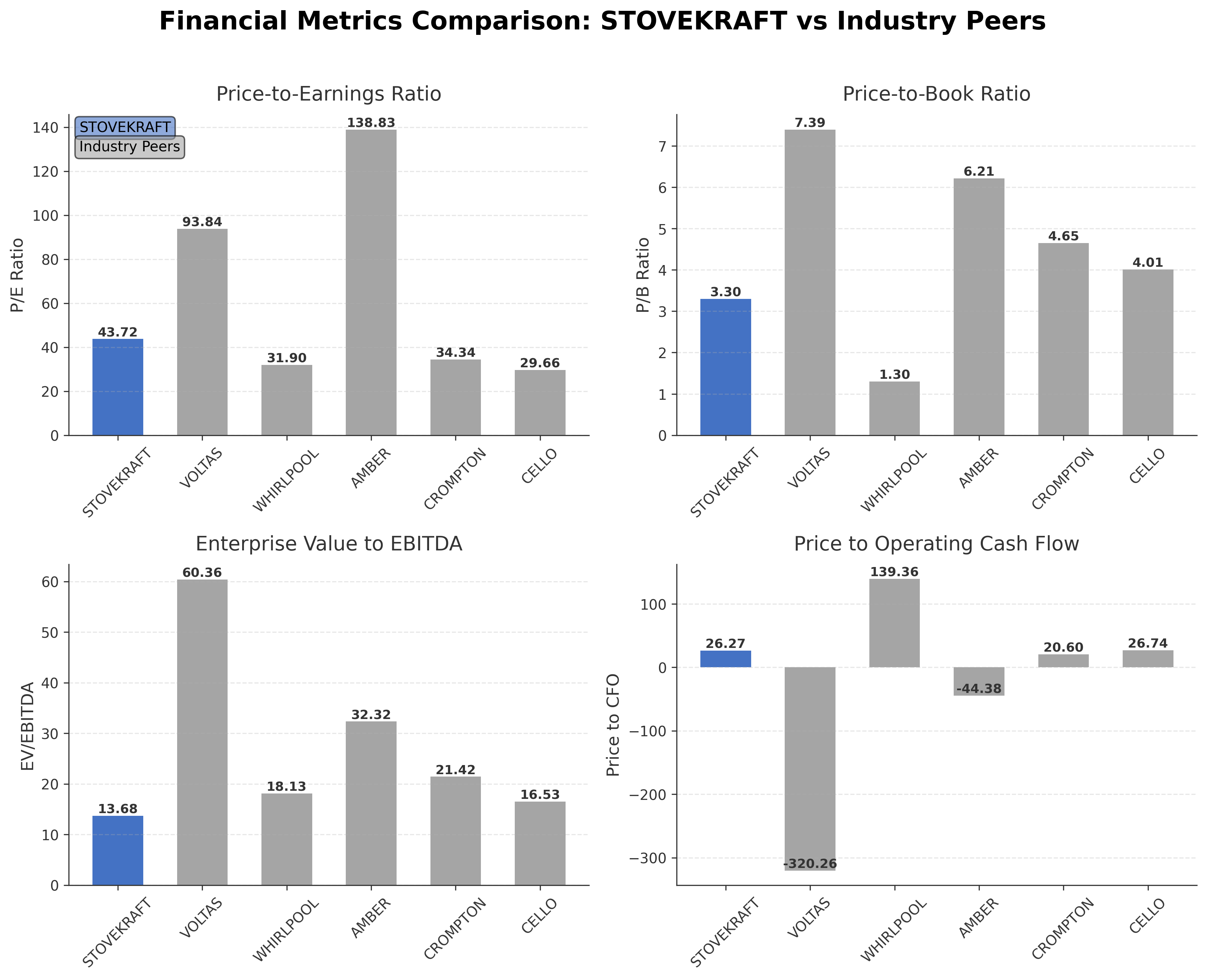

In peer comparison within the Indian consumer cyclical and home appliances industry, Stove Kraftâs market capitalization is smaller relative to peers like Voltas Limited (â¹467.94 billion) and Amber Enterprises (â¹226.85 billion). Its P/E ratio of 43.72 is higher than Whirlpool India (31.90) and Crompton Greaves (34.34), but lower than Amber Enterprises (138.83). Return on equity at 8.18% is modest compared to peer averages, while the EV/EBITDA multiple of 13.68 is more conservative than Voltas and Amber. These metrics position Stove Kraft as a mid-sized player with valuation and profitability metrics that reflect both growth potential and operational challenges.

Stove Kraft navigates a dynamic industry landscape marked by evolving consumer preferences and supply disruptions. The companyâs recent achievements include leveraging LPG supply constraints to boost induction cooktop demand, though stock performance has faced headwinds with a 33% decline over six months. Ongoing challenges include managing operational margins and sustaining growth amid competitive pressures. The stakes involve balancing innovation and market expansion against valuation and profitability concerns. Those evaluating the stock may find a nuanced profile that warrants attentive observation of market developments and company execution.

Company and Industry Overview

Company Basics

Price Performance

Company Size

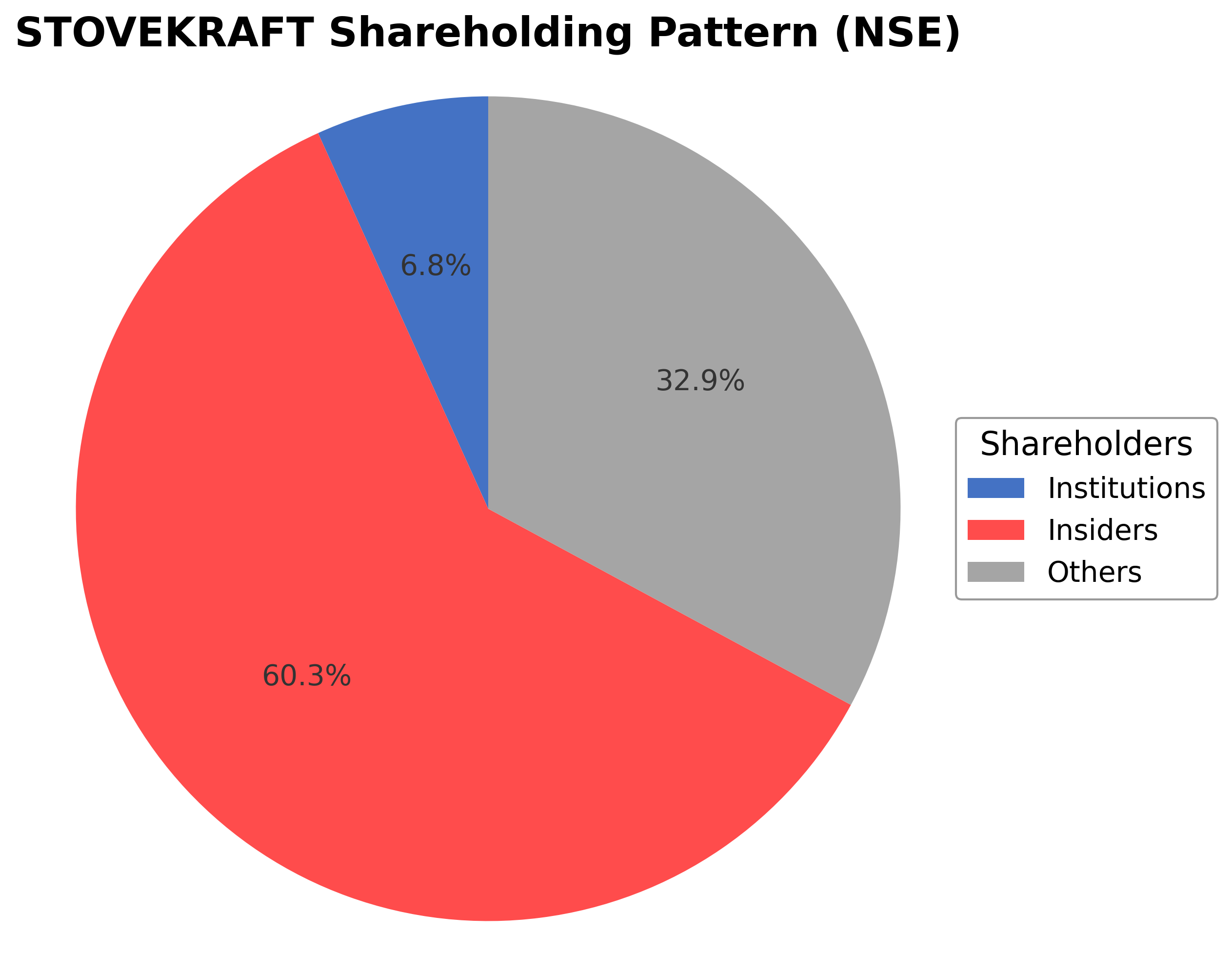

Shareholding Pattern

Stove Kraft Ltd.'s ownership structure is predominantly held by insiders, including executives and board members, accounting for approximately 60.34% of shares. Institutional investors, comprising mutual funds, pension funds, and asset managers, hold about 6.77%, while the remaining 32.89% is owned by public shareholders such as retail investors and employee stock plans. Over the past 12 to 24 months, there have been no significant shifts in promoter holdings, while institutional accumulation has remained relatively stable with minor fluctuations. This shareholding pattern suggests a strong promoter control with moderate institutional interest, which may influence governance and strategic decision-making. The company's position within the Furnishings, Fixtures & Appliances industry in India reflects a competitive environment with growth driven by urbanization and consumer lifestyle changes.

Sector and Industry Analysis

Stove Kraft Ltd operates within the Consumer Durables sector, specifically focusing on kitchen appliances and cookware. The Indian consumer durables market has exhibited robust growth, driven by rising disposable incomes, urbanization, and increasing consumer preference for branded and quality products. The sector’s market size is substantial, with growth rates typically in the mid-to-high single digits annually, supported by expanding middle-class demographics and increasing penetration of modern retail channels. Key players in this sector include established domestic companies and multinational corporations offering a broad range of kitchen appliances, cookware, and related products, competing on innovation, brand equity, and distribution reach.

Industry trends in the consumer durables segment are shaped by technological advancements and evolving consumer preferences. There is a marked shift towards smart and energy-efficient appliances, integrating IoT capabilities for enhanced user convenience and sustainability. Consumers increasingly demand products that combine aesthetics with functionality, driving innovation in materials and design. E-commerce and omni-channel retailing have emerged as critical growth enablers, allowing companies like Stove Kraft to expand their reach beyond traditional brick-and-mortar stores. Additionally, rising health consciousness and cooking-at-home trends post-pandemic have created new opportunities for premium and specialized cookware segments.

The regulatory landscape for consumer durables in India encompasses product safety standards, environmental regulations, and import/export policies. Compliance with the Bureau of Indian Standards (BIS) certifications and adherence to energy efficiency norms under the Bureau of Energy Efficiency (BEE) are mandatory for many appliances. Recent government initiatives promoting Make in India and Atmanirbhar Bharat have incentivized domestic manufacturing and local sourcing, impacting supply chain strategies. Moreover, GST implementation has streamlined taxation but requires ongoing compliance vigilance. Regulatory policies around e-waste management and sustainability are increasingly influencing product design and end-of-life disposal practices.

Competitive dynamics in the kitchen appliances and cookware industry are characterized by moderate to high competition with several established and emerging players. The market structure is fragmented, with a mix of branded manufacturers and unorganized local producers. Barriers to entry include the need for significant brand building, distribution network development, and compliance with regulatory standards. Stove Kraft’s competitive positioning leverages its focus on product innovation, brand differentiation, and expanding retail footprint. However, pricing pressures and the need for continuous technological upgrades necessitate sustained investment in R&D and marketing. Strategic partnerships and acquisitions are common approaches to consolidate market share and enhance product portfolios in this evolving landscape.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

Financials

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Stove Kraft Ltd. | ₹16.33B | 43.72 | 3.30 | 13.68 | 26.27 |

| Voltas Limited | ₹467.94B | 93.84 | 7.39 | 60.36 | -320.26 |

| Whirlpool of India Ltd. | ₹106.31B | 31.90 | 1.30 | 18.13 | 139.36 |

| Amber Enterprises India Ltd. | ₹226.85B | 138.83 | 6.21 | 32.32 | -44.38 |

| Crompton Greaves Consumer Electricals Ltd. | ₹160.95B | 34.34 | 4.65 | 21.42 | 20.60 |

| Cello World Ltd. | ₹91.69B | 29.66 | 4.01 | 16.53 | 26.74 |

Comparison Analysis: Stove Kraft Ltd. is positioned as a mid-cap company within the Indian household appliances industry, with a market capitalization significantly lower than larger peers such as Voltas and Amber Enterprises. Its P/E ratio of 43.72 is higher than Whirlpool and Crompton but lower than Amber, indicating a relatively elevated valuation. The price-to-book ratio of 3.30 is moderate compared to peers, while the EV/EBITDA multiple of 13.68 is comparatively conservative. Return on equity at 8.18% trails several peers, suggesting room for improvement in profitability. Overall, Stove Kraft exhibits a balanced profile with valuation and profitability metrics reflecting growth potential tempered by operational challenges.

Financial Metrics Comparison with Peers

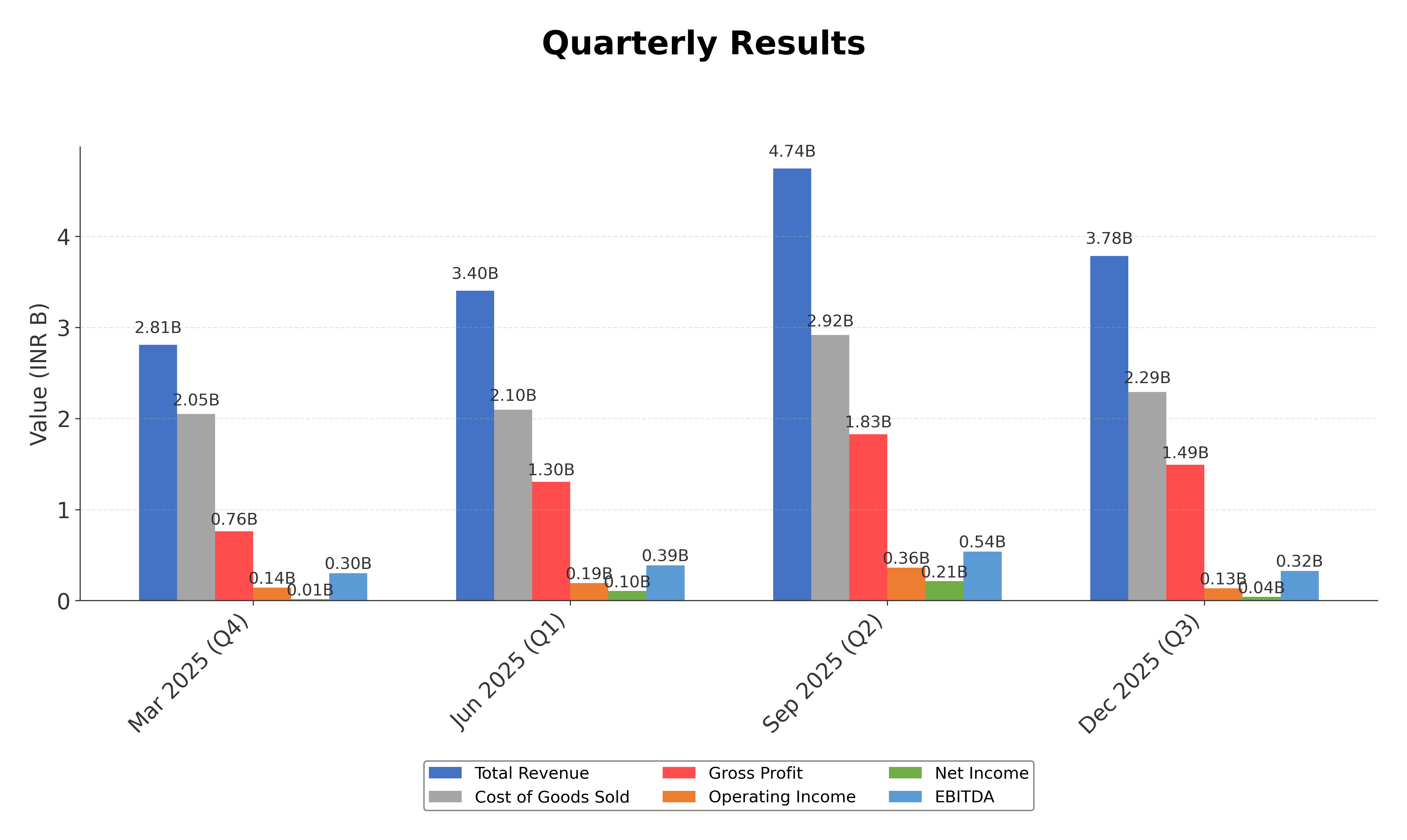

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 14.18B | 13.37B | 12.58B | 11.30B | 8.53B |

| Cost Of Goods | 9.10B | 8.75B | 8.84B | 7.95B | 5.74B |

| Gross Profit | 5.08B | 4.62B | 3.73B | 3.35B | 2.79B |

| Operating Expense Selling General And Administrative | 1.26B | 1.13B | 986.33M | 751.68M | 616.79M |

| Operating Expense Other Operating Expenses | 857.50M | 760.00M | 516.98M | 428.28M | 231.61M |

| Operating Income | 847.76M | 813.48M | 731.62M | 891.54M | 1.04B |

| Non Operating Interest Income | 11.12M | 7.74M | 7.25M | 3.39M | 4.97M |

| Non Operating Interest Expense | 302.93M | 229.94M | 155.26M | 104.79M | 181.03M |

| Pretax Income | 487.88M | 455.51M | 472.80M | 625.40M | 811.84M |

| Income Tax | 102.83M | 114.16M | 115.10M | 63.25M | 0.00 |

| Net Income | 385.05M | 341.35M | 357.70M | 562.15M | 811.84M |

| Eps Basic | 11.65 | 10.30 | 10.87 | 17.21 | 26.61 |

| Eps Diluted | 11.64 | 10.30 | 10.86 | 16.96 | 26.25 |

| Basic Shares Outstanding | 33.06M | 33.13M | 32.90M | 32.66M | 30.51M |

| Diluted Shares Outstanding | 33.06M | 33.13M | 32.90M | 32.66M | 30.51M |

| Ebit | 790.81M | 685.45M | 628.06M | 730.19M | 992.87M |

| Ebitda | 1.55B | 1.27B | 987.41M | 1.06B | 1.18B |

| Net Income Continuous Operations | 487.88M | 455.51M | 472.80M | 625.40M | 811.84M |

| Preferred Stock Dividends | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Minority Interests | N/A | N/A | N/A | N/A | -30.00K |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 27.64M | 71.30M | 25.26M | 4.05M | 294.53M |

| Accounts Receivable | 1.31B | 1.46B | 1.41B | 966.99M | 847.24M |

| Total Assets | 12.04B | 10.97B | 8.97B | 7.28B | 5.71B |

| Total Liabilities | 7.33B | 6.58B | 4.94B | 3.64B | 2.68B |

| Long Term Debt | 1.52B | 1.07B | 422.97M | 152.54M | 206.63M |

| Shareholders Equity | 4.71B | 4.39B | 4.03B | 3.64B | 3.03B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 487.88M | 455.51M | 472.80M | 625.40M | 811.84M |

| Operating Activities Stock Based Compensation | 3.66M | 12.31M | 5.15M | 11.00M | 12.63M |

| Operating Activities Other Non Cash Items | 293.53M | 213.36M | 148.02M | 102.16M | 174.42M |

| Operating Activities Accounts Receivable | 115.57M | -149.70M | -484.37M | -253.03M | 143.34M |

| Operating Activities Other Assets Liabilities | -279.10M | -768.36M | -167.56M | -563.11M | -343.99M |

| Operating Activities Operating Cash Flow | 621.54M | -236.88M | -25.96M | -77.58M | 798.24M |

| Investing Activities Capital Expenditures | -811.17M | -1.04B | -976.29M | -1.08B | -630.73M |

| Investing Activities Other Investing Activity | 11.92M | 147.17M | -69.33M | -78.65M | -35.16M |

| Investing Activities Investing Cash Flow | -799.25M | -895.51M | -1.05B | -1.16B | -656.47M |

| Financing Activities Long Term Debt Payments | -48.98M | -52.28M | -56.74M | -16.82M | -332.33M |

| Financing Activities Short Term Debt Issuance | 390.58M | 225.10M | 548.72M | 276.29M | -922.62M |

| Financing Activities Common Stock Issuance | 12.37M | 3.73M | 23.86M | 41.77M | 918.34M |

| Financing Activities Common Dividends | -82.59M | N/A | N/A | N/A | N/A |

| Financing Activities Other Financing Charges | -384.80M | -100.16M | -73.17M | 721.08M | 47.16M |

| Financing Activities Financing Cash Flow | -113.42M | 76.39M | 991.39M | 1.02B | -21.56M |

| End Cash Position | 27.64M | 71.30M | 25.26M | 4.05M | 294.53M |

| Free Cash Flow | 478.50M | -10.86M | -222.41M | -1.17B | 395.35M |

| Financing Activities Long Term Debt Issuance | N/A | N/A | 548.72M | 0.00 | 267.89M |

| Investing Activities Net Acquisitions | N/A | N/A | N/A | 0.00 | 9.42M |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend shows mixed momentum with the stock price at ₹518.65, trading below the 200-day moving average of ₹600.44 but slightly above the 50-day moving average of ₹509.05, indicating short-term support.

- Key support levels are observed near ₹453.15 (52-week low) and ₹509, while resistance is noted around ₹600 and ₹820 (52-week high).

- The stock is positioned below the 200-day moving average, suggesting a longer-term bearish trend, while the 10-day and 50-day moving averages indicate potential consolidation.

- Momentum indicators show a moderate RSI, with MACD and Stochastic oscillators reflecting neutral to slightly bearish signals, indicating limited upward momentum.

- Multi-timeframe analysis reveals bearish pressure on daily and weekly charts, with monthly charts showing potential stabilization.

- Current technical setup suggests potential volatility with scenarios ranging from consolidation near support levels to further downside if key supports fail.

Trending News

1. Headline: BEW Engineering bulk deal: Ashish Kacholia exits SME company as stock slumps 44% in a year - The Economic Times

Summary: Ace investor Ashish Kacholia exited BEW Engineering entirely through a bulk deal, amid prolonged stock underperformance and declining prices, raising concerns about the companys near-term outlook despite its niche presence in pharmaceutical equipment manufacturing and past listing gains.

Sentiment: negative

2. Headline: Stove Kraft shares down 33% in 6 months; worth a buy? - BusinessToday

Summary: After rallying for two days on hopes of increased demand amid LPG shortage, shares of kitchen solutions provider Stove Kraft Ltd dropped for four straight sessions, taking their six-month fall to 33 per cent.

Sentiment: negative

3. Headline: Induction cooktops: A hot trade, but cold earnings story for makers | Stock Market News

Summary: LPG disruptions amid the West Asia conflict boost interest in induction cooktops, but sales account for a small slice of revenue for TTK Prestige, Stovekraft and Butterfly Gandhimathi.

Sentiment: positive

4. Headline: Stove Kraft, TTK Prestige Shares Fall Amid LPG Supply Turmoil

Summary: Shares of several kitchen appliance companies slipped on Monday even as concerns about cooking gas shortages triggered a surge in demand for alternative cooking appliances across India. Stocks of Stove Kraft, which owns the Pigeon brand, and TTK Prestige, the maker of Prestige products, declined by

Sentiment: negative

Summary: Further, Stove Kraft said its average weekly online sales have jumped four times. "At Croma, we have observed a sharp and immediate uptick in demand for induction cooktops over the past few days. Our average daily run rate has surged significantly," Infiniti Retail Ltd (Croma) CEO & MD Shibashish ...

Sentiment: positive

Summary: Further, Stove Kraft said its average weekly online sales have jumped four times. "At Croma, we have observed a sharp and immediate uptick in demand for induction cooktops over the past few days. Our average daily run rate has surged significantly," Infiniti Retail Ltd (Croma) CEO & MD Shibashish ...

Sentiment: positive

7. Headline: Stove Kraft Ltd Hits Intraday Low Amid Price Pressure on 12 Mar 2026

Summary: Stove Kraft Ltd experienced a notable intraday decline on 12 Mar 2026, with the stock hitting a low of Rs 506.5, reflecting a 7.07% drop from its previous close. This downturn occurred despite an initial gap-up opening, underscoring significant price pressure amid a broadly negative market ...

Sentiment: negative

Summary: LPG shortage hits restaurants and food apps; watch market moves and government action—explore key stocks and responses now.

Sentiment: neutral

9. Headline: TTK Prestige, Stove Kraft surge up to 15% as LPG shortage fuels induction cooktop demand

Summary: Retailers and e-commerce platforms have reportedly seen a sharp increase in orders for induction cooktops as consumers look for alternatives to LPG-based cooking.

Sentiment: positive

10. Headline: TTK Prestige, Butterfly Gandhimathi, Stove Kraft Shares Jump Up To 15% Over LPG Shortage

Summary: Shares of kitchen appliance makers rose sharply on Wednesday after the government moved to divert gas supplies to protect cooking fuel availability amid disruptions caused by the Iran war. TTK Prestige Ltd., Butterfly Gandhimathi Appliances Ltd. and Stove Kraft Ltd.

Sentiment: positive

Powered by Brave

Recent Updates

News Summary

Recent news coverage of Stove Kraft Ltd highlights a mixed market environment characterized by significant share price volatility and evolving demand dynamics. The company’s shares have declined by approximately 33% over six months, reflecting bearish momentum and technical downturns amid market pressure. However, increased demand for induction cooktops driven by LPG shortages has led to notable short-term sales surges and positive market reactions, with shares rising up to 15% in response to supply constraints. Earnings reports indicate missed revenue expectations, though analysts forecast a 19% revenue growth in 2027. The news cycle underscores themes of supply disruption, consumer behavior shifts, and competitive positioning within the household appliances sector, with implications for revenue growth and investor sentiment. These developments occur against a backdrop of broader industry trends and geopolitical factors influencing LPG availability.

News Sentiment

Sentiment across recent news is mixed, with a balance of positive and negative tones. Positive sentiment is driven by increased demand for induction cooktops amid LPG shortages and associated share price rallies. Negative sentiment arises from share price declines, earnings misses, and technical challenges. Neutral coverage reflects cautious market appraisal of the company’s near-term outlook. Overall, sentiment indicates cautious optimism tempered by operational and market risks.

Analytical Overview

Analysis Summary

Valuation Metrics: Stove Kraft’s trailing P/E of 43.72 exceeds the industry average of 43.72, while its forward P/E of 26.27 suggests a potential valuation re-rating. The price-to-book ratio of 3.30 is moderate relative to peers, indicating a balanced valuation profile.

Growth Trajectory: The company’s revenue has declined by 6.4% quarter-over-quarter, with a negative quarterly earnings growth of 65.8% year-over-year, signaling near-term growth challenges. However, analysts forecast a 19% revenue increase in 2027, reflecting potential medium-term growth.

Financial Health: Stove Kraft maintains a debt-to-equity ratio of 52.58%, indicating moderate leverage. Operating cash flow and free cash flow remain positive at ₹621.54 million and ₹385.05 million respectively, supporting financial stability despite margin pressures.

Sector Specific Factors: The household appliances sector faces supply chain disruptions and competitive pressures, but also benefits from rising urbanization and consumer demand for energy-efficient kitchen solutions, amplified by LPG shortages in India.

Market Positioning: Stove Kraft’s strong brand presence and diversified product portfolio position it well within the Indian market, though it faces competition from larger peers with greater scale and resources.

Investment Conclusion

Supporting Factors: Strong brand recognition and manufacturing capabilities underpin market presence.

Risk Factors: Recent declines in revenue and earnings growth indicate near-term challenges.

SWOT Analysis

Strengths

- Strong brand portfolio with recognized names like Pigeon and Gilma.

- Diverse product range catering to evolving consumer kitchen needs.

- Established manufacturing capabilities and distribution network.

- Positive operating and free cash flow supporting financial stability.

Weaknesses

- Declining quarterly revenue and earnings growth indicate operational challenges.

- Moderate debt-to-equity ratio of 52.58% reflects leverage risk.

- Profit margins remain thin at approximately 2.48%.

- Stock price volatility and recent downward trend may affect market sentiment.

Opportunities

- Rising demand for induction cooktops amid LPG supply disruptions.

- Growth potential in urban Indian markets driven by lifestyle changes.

- Expansion into international markets to diversify revenue streams.

- Increasing consumer preference for energy-efficient kitchen appliances.

Threats

- Intense competition from larger, well-capitalized industry peers.

- Supply chain disruptions impacting production and delivery timelines.

- Economic uncertainties affecting consumer discretionary spending.

- Regulatory changes and geopolitical tensions influencing LPG availability.

Company Description

Stove Kraft Ltd. is a key player in the household appliances industry, focused primarily on the design, manufacturing, and marketing of a diverse range of kitchen and home solutions. Its offerings include traditional and contemporary cooktops, chimneys, and pressure cookers, along with other kitchen essentials like mixers and grinders under reputable brand names such as Pigeon and Gilma. The company prides itself on delivering innovative, user-friendly, and affordable products that cater to the evolving needs of modern-day consumers. Stove Kraft Ltd. operates significant manufacturing capabilities and has a distribution network that covers not only the domestic Indian market but also various international markets, enhancing its global footprint. The company's focus on quality and value has earned it a strong reputation among consumers and solidified its role as a market leader within the competitive appliances industry. With headquarters in Bangalore, India, Stove Kraft continues to capitalize on the growing demand for efficient kitchen solutions, driven by urbanization and lifestyle changes, making it a prominent contributor to the expanding home appliance sector.