Punjab National Bank (PNB)

Stock Analysis Report

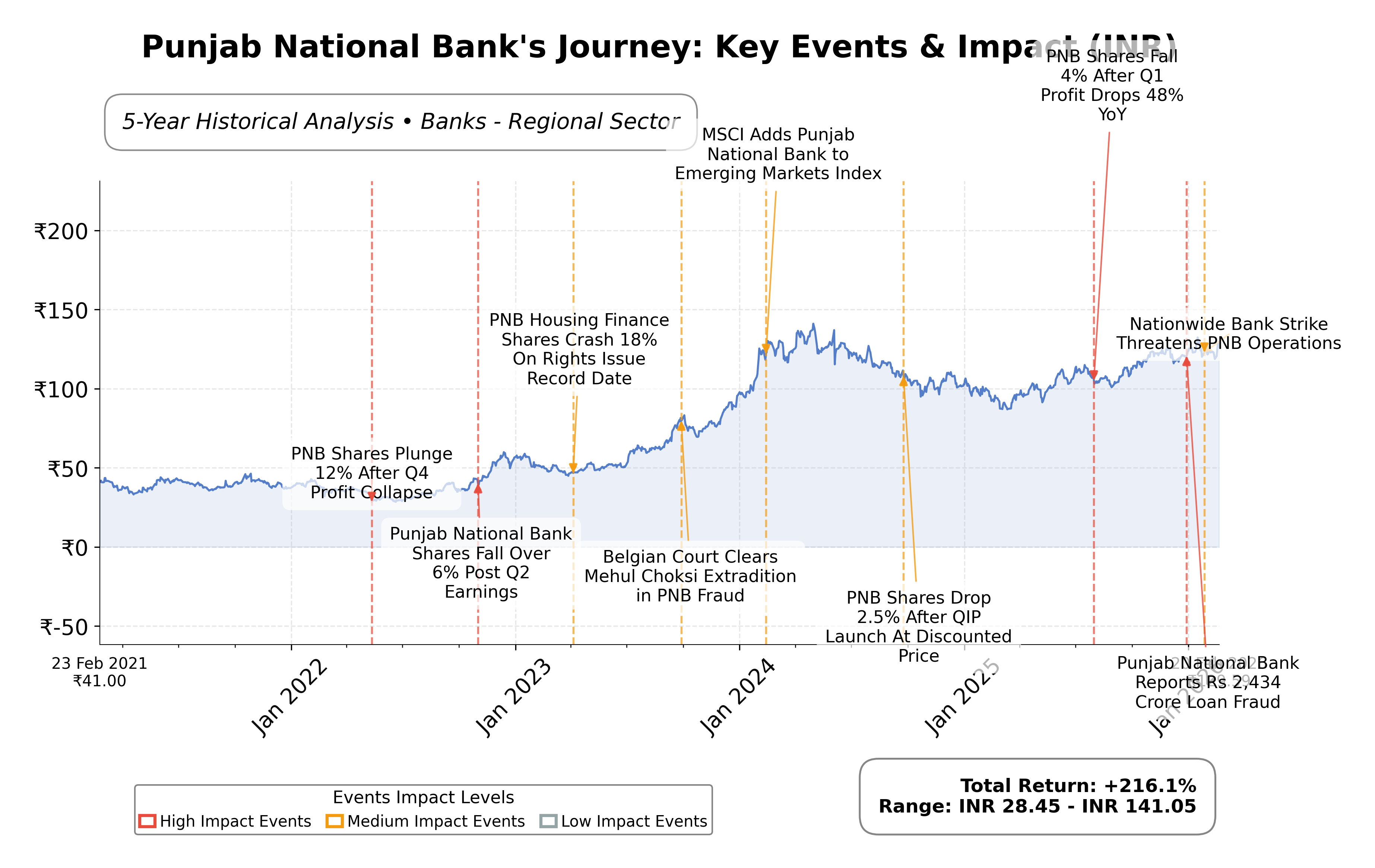

Stock Journey

Key Positives and Key Risks

Pros

- Market capitalization of ₹1.49 trillion positions PNB as a leading player in the Indian regional banking sector, indicating scale and market presence.

- Trailing P/E ratio of 8.37 aligns with industry average, suggesting valuation consistency and potential value relative to earnings.

- Strong operating margin of 44.09% and net income growth of 15.7% year-over-year reflect operational efficiency and profitability.

Cons

- Quarterly revenue declined by 2.3%, indicating potential near-term growth headwinds.

- Debt-to-equity ratio of 0.77, while moderate, requires monitoring amid regulatory transitions impacting credit risk.

- Ongoing fraud investigations and operational disruptions pose reputational and governance risks.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Punjab National Bank (PNB) is a leading public sector bank in India, operating within the regional banking industry. Established in 1894, it offers a broad spectrum of financial services including deposit mobilization, lending to individuals and SMEs, treasury operations, and wealth management. The bank holds a significant market position with an extensive branch network across urban and rural India, supporting financial inclusion and economic growth.

Financially, PNB exhibits a market capitalization of approximately â¹1.49 trillion and trades at a trailing P/E ratio of 8.37, closely aligned with the industry average. The bank maintains a price-to-book ratio near 1.00 and a forward P/E of 8.02, indicating valuation metrics consistent with its sector peers. Profit margins stand at 34.67%, with operating margins at 44.09%, and a return on equity of 12.71%. The bank reported a slight quarterly revenue decline of 2.3%, while net income grew by 15.7% year-over-year. Its debt-to-equity ratio is moderate at 0.77, supported by substantial cash reserves of over â¹1.5 trillion.

Technically, PNBâs stock price is currently near â¹130.27, within a 52-week range of â¹85.46 to â¹135.15, reflecting an upside potential of approximately 3.7% to the 52-week high. The stock trades above its 50-day and 200-day moving averages, indicating a generally positive trend. Recent strategic initiatives include enhanced digital HRMS services and active management of non-performing assets, as evidenced by auctioning of debt. Leadership and regulatory developments, including ongoing fraud case proceedings, present both governance challenges and operational risks. The bankâs strengths lie in its robust asset base and government backing, while risks include regulatory transitions and operational disruptions.

In comparison with regional peers such as Bandhan Bank, Bank of India, Indian Bank, Yes Bank, and RBL Bank, PNB holds the largest market capitalization and trades at a relatively lower P/E ratio, suggesting more conservative valuation. Its price-to-book ratio is competitive, and price to cash flow from operations is moderate relative to peers. While some peers exhibit higher growth multiples, PNBâs scale and public sector status provide a distinctive positioning within the Indian banking sector.

Punjab National Bank navigates a complex industry landscape marked by regulatory reforms, competitive pressures, and evolving market dynamics. Recent achievements include steady earnings growth and enhanced operational capabilities, while challenges encompass regulatory transitions and reputational risks from fraud cases. The bank stands at a pivotal juncture where its strategic execution and risk management will influence its market stature and financial performance. Given the current financial and technical profile, a balanced approach emphasizing monitoring of developments and valuation metrics may align with the prevailing market context.

Company and Industry Overview

Company Basics

Price Performance

Company Size

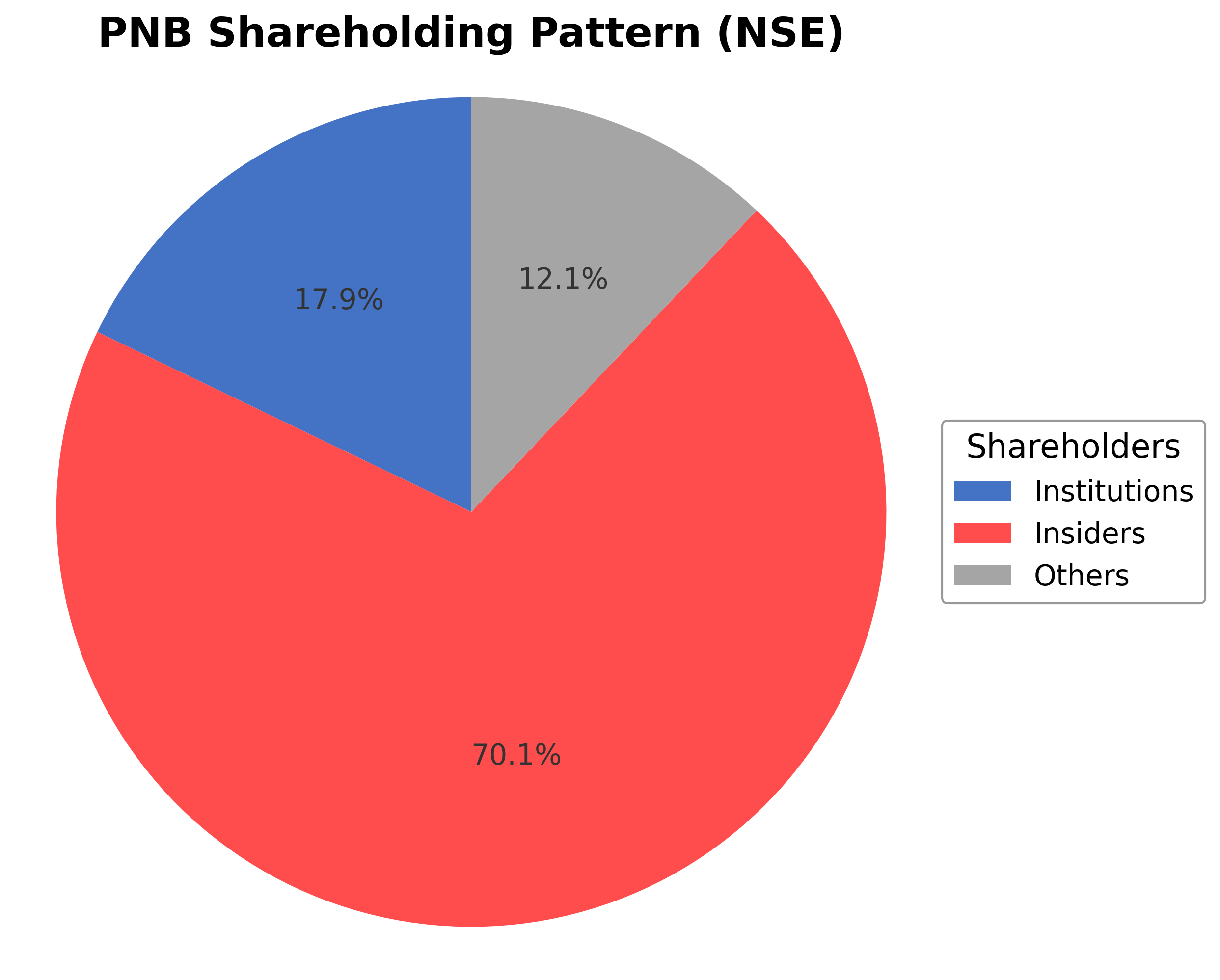

Shareholding Pattern

Punjab National Bank's ownership structure comprises approximately 0.70% held by insiders including executives and board members, 17.86% by institutional investors such as mutual funds and pension funds, and the remaining 81.44% by public shareholders including retail investors and employee stock plans. Over the past 12 to 24 months, institutional holdings have shown moderate accumulation, reflecting sustained interest from major funds. This shareholding pattern indicates a broad market participation with significant institutional involvement, which may influence governance practices and strategic decisions. The current ownership distribution suggests a balanced alignment between public accountability and institutional oversight within the Indian regional banking sector.

Sector and Industry Analysis

Sector and Industry Analysis: Indian Banking Sector with Focus on Punjab National Bank (PNB)

1. Sector Overview: The Indian banking sector is a critical component of the country’s financial system, encompassing a broad range of institutions including public sector banks (PSBs), private sector banks, foreign banks, and regional rural banks. As of 2026, the sector commands a market capitalization exceeding $500 billion, with public sector banks like Punjab National Bank (market cap approx. $16.4 billion) playing a pivotal role in financial intermediation. The sector has witnessed steady growth driven by India’s expanding economy, rising financial inclusion, and increasing credit demand from retail, corporate, and agricultural segments. Key players include State Bank of India (SBI), ICICI Bank, HDFC Bank, and PNB, with PSBs collectively holding a significant share of total banking assets and deposits.

2. Industry Trends: The Indian banking industry is undergoing rapid digital transformation, with technology adoption such as mobile banking, UPI (Unified Payments Interface), and AI-driven credit assessment reshaping consumer interactions and operational efficiency. There is a marked shift towards digital-first banking models, driven by changing consumer behavior favoring convenience and instant services. Additionally, the sector is exploring emerging opportunities in fintech partnerships, blockchain for secure transactions, and sustainable finance aligned with ESG principles. The rise of digital lending platforms and increased focus on MSME (Micro, Small, and Medium Enterprises) financing also present growth avenues. However, legacy challenges such as non-performing assets (NPAs) and capital adequacy remain focal points for ongoing reform.

3. Regulatory Landscape: The Indian banking sector operates under the regulatory oversight of the Reserve Bank of India (RBI), which enforces prudential norms, capital requirements (Basel III compliance), and consumer protection guidelines. Recent regulatory initiatives emphasize strengthening risk management, enhancing transparency, and promoting financial inclusion through schemes like Jan Dhan Yojana. The Insolvency and Bankruptcy Code (IBC) has been instrumental in addressing stressed assets. Additionally, the government’s disinvestment policies and recapitalization plans for PSBs, including PNB, impact operational strategies. Compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) norms remains stringent, with increasing emphasis on cybersecurity frameworks to safeguard digital banking infrastructure.

4. Competitive Dynamics: The Indian banking sector is characterized by an oligopolistic market structure dominated by a few large PSBs and private banks. Barriers to entry are high due to regulatory capital requirements, extensive branch networks, and brand trust. Punjab National Bank, as a major PSB, benefits from government backing and a wide customer base but faces intense competition from agile private sector banks that leverage technology for superior customer experience. Competitive positioning hinges on factors such as asset quality, cost of funds, digital capabilities, and geographic reach. Consolidation trends, including mergers among PSBs, aim to create stronger entities capable of competing effectively. Innovation in product offerings and customer service, alongside regulatory compliance, are critical for sustaining market share in this competitive environment.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

Financials

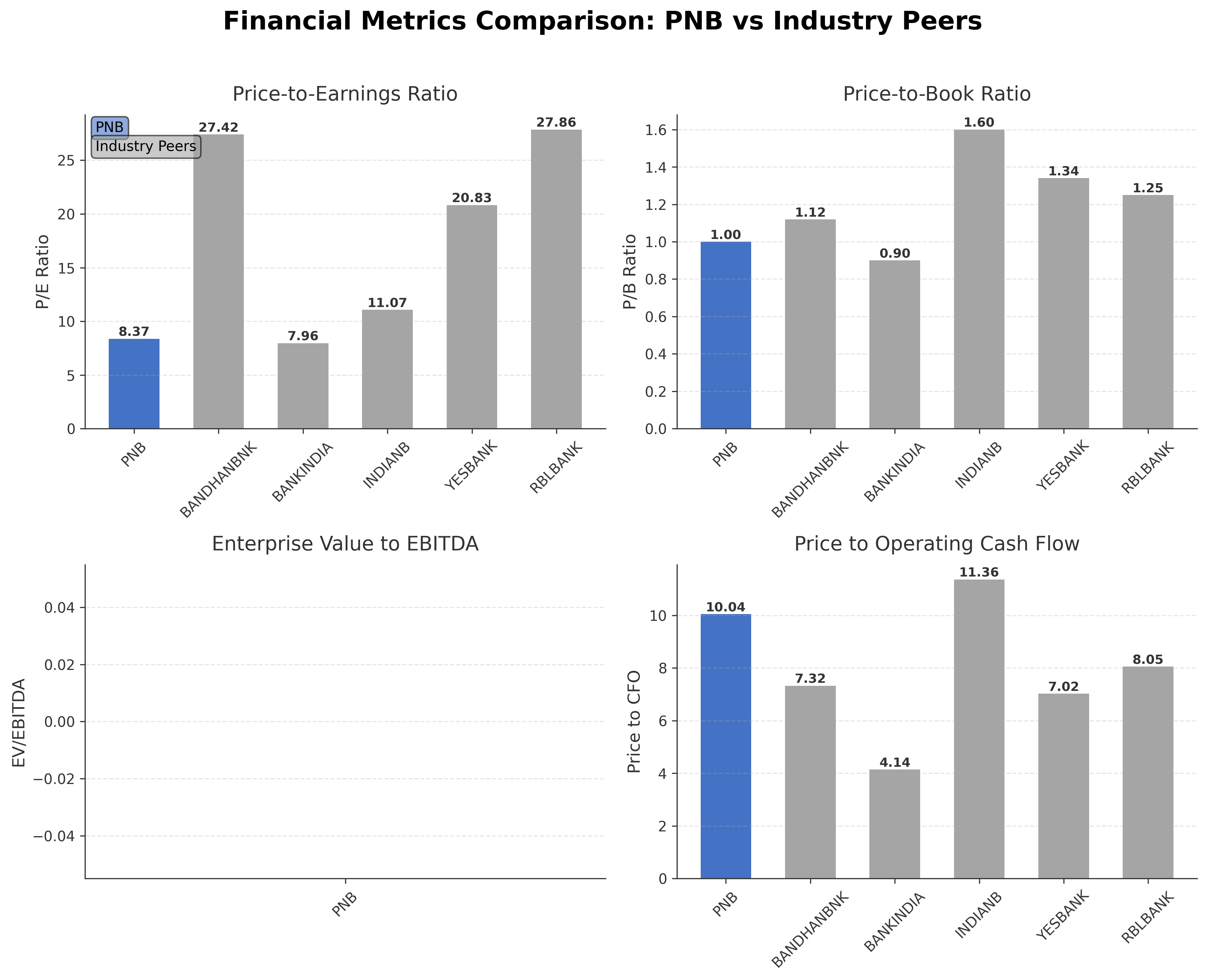

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Punjab National Bank | ₹1.49T | 8.37 | 1.0 | N/A | 10.04 |

| Bandhan Bank Ltd. | ₹276.04B | 27.42 | 1.12 | N/A | 7.32 |

| Bank of India | ₹781.69B | 7.96 | 0.9 | N/A | 4.14 |

| Indian Bank | ₹1.28T | 11.07 | 1.6 | N/A | 11.36 |

| Yes Bank Ltd. | ₹660.84B | 20.83 | 1.34 | N/A | 7.02 |

| RBL Bank Ltd. | ₹203.21B | 27.86 | 1.25 | N/A | 8.05 |

Comparison Analysis: Punjab National Bank holds the largest market capitalization among its regional banking peers in India, with a valuation that reflects a more conservative P/E ratio of 8.37 compared to higher multiples seen in Bandhan Bank and RBL Bank. Its price-to-book ratio of 1.00 is competitive, indicating valuation close to book value, while its price to cash flow from operations is moderate at 10.04. Peers such as Indian Bank exhibit higher P/E and P/B ratios, suggesting differing growth expectations. Overall, PNB's scale and valuation metrics position it as a key player with stable fundamentals relative to its regional competitors.

Financial Metrics Comparison with Peers

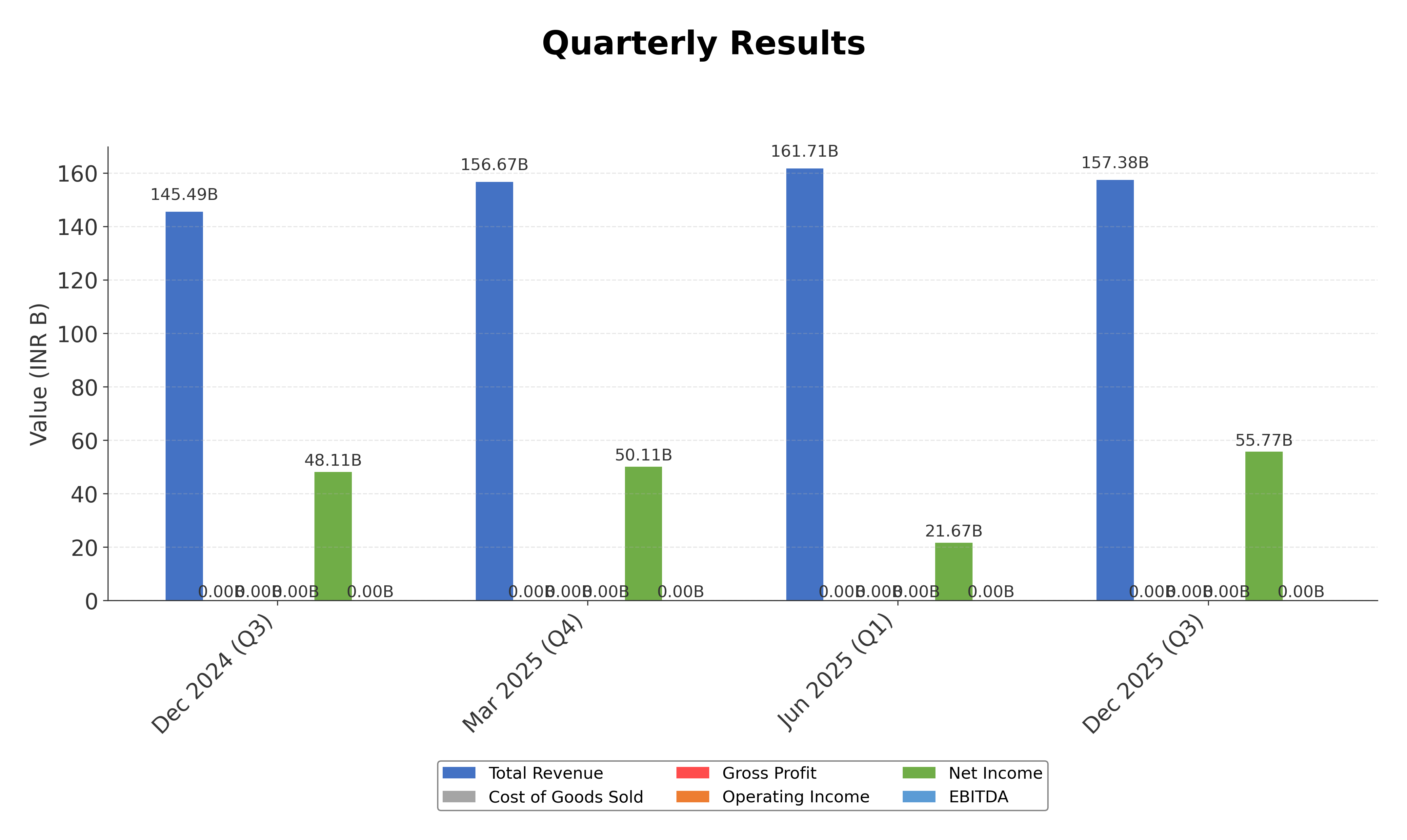

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 597.61B | 552.61B | 470.92B | 411.54B | 436.00B |

| Operating Expense Selling General And Administrative | 3.17B | 3.08B | 2.85B | 2.47B | 2.38B |

| Operating Expense Other Operating Expenses | 64.27B | 67.04B | 55.96B | 52.49B | 48.28B |

| Pretax Income | 260.15B | 141.60B | 51.51B | 48.26B | 43.25B |

| Income Tax | 86.13B | 50.03B | 17.92B | 9.19B | 16.30B |

| Net Income | 185.53B | 91.57B | 33.59B | 39.08B | 26.95B |

| Eps Basic | 16.42 | 8.27 | 3.04 | 3.53 | 2.64 |

| Eps Diluted | 16.42 | 8.27 | 3.04 | 3.53 | 2.64 |

| Basic Shares Outstanding | 11.26B | 11.01B | 11.01B | 10.95B | 9.71B |

| Diluted Shares Outstanding | 11.26B | 11.01B | 11.01B | 10.95B | 9.71B |

| Net Income Continuous Operations | 270.93B | 141.10B | 51.41B | 47.79B | 41.94B |

| Minority Interests | -723.20M | -499.50M | -103.30M | -468.50M | -1.33B |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-12-31 | 2025-06-30 | 2025-03-31 | 2024-12-31 | 2024-09-30 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 1510.05B | 1407.40B | 1507.60B | 1389.98B | 1186.14B |

| Accounts Receivable | N/A | N/A | N/A | N/A | N/A |

| Total Assets | 19762.28B | 18737.15B | 18575.44B | 17963.82B | 17226.52B |

| Total Liabilities | 18266.24B | 17349.24B | 17237.77B | 16646.06B | 15953.95B |

| Long Term Debt | 1147.58B | 934.72B | 719.99B | 901.47B | 944.96B |

| Shareholders Equity | 1496.04B | 1387.91B | 1337.66B | 1317.76B | 1272.58B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 270.93B | 141.10B | 51.41B | 47.79B | 41.94B |

| Operating Activities Other Non Cash Items | 31.16B | 29.70B | 24.68B | 22.02B | 19.93B |

| Operating Activities Other Assets Liabilities | -153.72B | 43.87B | 12.24B | 52.25B | -159.42B |

| Operating Activities Operating Cash Flow | 148.37B | 214.67B | 88.32B | 122.07B | -97.55B |

| Investing Activities Capital Expenditures | -15.86B | -11.44B | -5.52B | -5.36B | -7.87B |

| Investing Activities Net Acquisitions | 81.50M | -3.63B | -1.80B | -6.68B | 0.00 |

| Investing Activities Other Investing Activity | -100.00K | N/A | N/A | -100.00K | N/A |

| Investing Activities Investing Cash Flow | -15.78B | -15.06B | -7.32B | -12.04B | -7.87B |

| Financing Activities Common Stock Issuance | 49.88B | N/A | 0.00 | 17.93B | 37.77B |

| Financing Activities Common Dividends | -16.52B | -7.16B | -7.05B | N/A | N/A |

| Financing Activities Other Financing Charges | 676.50M | 1.01B | -140.90M | -133.20M | 1.26B |

| Financing Activities Financing Cash Flow | 34.04B | -6.14B | -7.19B | 17.80B | 39.03B |

| End Cash Position | 1507.60B | 1314.00B | 1573.28B | 1341.94B | 1133.34B |

| Free Cash Flow | 204.74B | -290.83B | 220.40B | 194.96B | 4.53B |

Data provided by Twelve Data

Technical Analysis

Key Insights

- PNB's current trend shows a positive price momentum trading above both the 50-day moving average (₹123.44) and 200-day moving average (₹114.70), indicating an upward trend in the medium to long term.

- Key support levels are identified near ₹114.70 (200-day MA) and ₹123.44 (50-day MA), while resistance is observed near the 52-week high of ₹135.15.

- The stock price is currently above the 10-day, 50-day, and 200-day moving averages, suggesting bullish momentum across short, medium, and long-term timeframes.

- Momentum indicators show RSI in a neutral to slightly bullish range, MACD lines indicating positive crossover, and stochastic oscillators reflecting upward momentum in the short term.

- Multi-timeframe analysis reveals consistent strength on daily, weekly, and monthly charts, supporting sustained positive price action.

- Potential market scenarios include continuation of the upward trend if resistance near ₹135.15 is breached, or consolidation near current support levels if profit-taking occurs.

Trending News

1. Headline: Stocks to buy: What's the outlook for Nifty for February 23-27 week? Check list of top stock recommendations

Summary: Sudeep Shah, Head of Technical Research, includes Punjab National Bank among stocks recommended for the week of February 23-27, highlighting its market relevance and technical positioning. The recommendation reflects ongoing interest in PNB within the broader Indian stock market context.

Sentiment: Neutral

2. Headline: PSU banks extends rally, gain up to 4%; SBI, BoB, Indian Bank hit new highs

Summary: Public sector banks including Punjab National Bank have contributed to a rally in the PSU Bank index, which gained 3.5% over two trading days, outperforming the Nifty 50. Other banks like SBI and Bank of Baroda reached new highs, reflecting positive market sentiment toward the sector.

Sentiment: Positive

3. Headline: Bullish Breakout: PNB Forms Ascending Triangle Pattern Hinting at Short-Term Upside

Summary: Technical analysis identifies an ascending triangle pattern on PNB's 30-minute chart, suggesting potential for a short-term bullish breakout. This pattern indicates consolidation with upward bias, which may attract trading interest.

Sentiment: Positive

4. Headline: CFM ARC leads race for Gammon India's ₹514-cr debt

Summary: CFM ARC is leading the bid to acquire ₹514 crore of Gammon India's debt from Punjab National Bank. The bank is conducting an electronic auction to maximize recovery, reflecting active management of non-performing assets and efforts to improve asset quality.

Sentiment: Positive

5. Headline: IDFC First Bank Rs 590-crore fraud: 'Even govt money is not safe in banks,' say netizens

Summary: Following a Rs 590-crore fraud at IDFC First Bank, social media users referenced a recent Rs 60-lakh gold loss at a Punjab National Bank locker, raising concerns about security and trust in banking institutions. The incident highlights reputational risks faced by banks including PNB.

Sentiment: Negative

Powered by Brave

Recent Updates

News Summary

Recent news highlights a surge in trading volume and positive momentum for Punjab National Bank, reflecting increased market activity and interest. The Enforcement Directorate's preparation to charge Rohan Choksi in the ongoing PNB scam case underscores continuing regulatory and legal scrutiny. Despite some negative sentiment due to broader market conditions and regulatory transitions, PNB remains a focus of foreign investor interest alongside other PSU banks. Operational challenges such as potential disruptions from nationwide bank strike calls have been communicated, while the bank anticipates financial impacts from transitioning to new credit rules. These developments collectively influence PNB's operational environment and market perception.

News Sentiment

The sentiment across recent news is mixed to positive, with notable optimism around trading activity and regulatory progress in fraud cases. Positive momentum is tempered by neutral and negative views related to regulatory transitions and operational risks. Overall, the sentiment reflects cautious optimism with attention to governance and market dynamics.

Analytical Overview

Analysis Summary

Valuation Metrics: Punjab National Bank's P/E ratio of 8.37 and forward P/E of 8.02 are in line with the industry average of 8.37, indicating valuation consistency within the regional banking sector. The PEG ratio of 0.64 suggests valuation relative to growth is moderate.

Growth Trajectory: The bank experienced a slight quarterly revenue decline of 2.3%, but net income increased by 15.7% year-over-year, supported by stable operating margins and positive cash flow trends. Operating cash flow and free cash flow remain robust, indicating healthy internal liquidity.

Financial Health: With a debt-to-equity ratio of 0.77 and total cash reserves exceeding ₹1.5 trillion, PNB maintains a balanced financial structure. Cash flow from operations and free cash flow metrics support operational stability, while moderate leverage suggests manageable financial risk.

Sector Specific Factors: The Indian banking sector faces regulatory transitions, including new credit rules impacting PNB with an estimated $1 billion effect. Opportunities exist in expanding financial inclusion and digital banking, while challenges include fraud risk management and operational disruptions.

Market Factors: India's regulatory environment, evolving consumer banking trends, and economic outlook influence PNB's market positioning. The bank's extensive branch network and government backing provide competitive advantages amid sector reforms.

Investment Conclusion

Supporting Factors: Valuation metrics align closely with industry averages, reflecting fair pricing.

Risk Factors: Regulatory transitions may impact earnings and operational processes.

SWOT Analysis

Strengths

- Established legacy as one of India's oldest public sector banks.

- Extensive branch network supporting financial inclusion across urban and rural areas.

- Robust cash flow generation and moderate debt levels.

- Government backing providing stability and market confidence.

Weaknesses

- Exposure to regulatory transitions impacting credit operations.

- Reputational risks from ongoing fraud investigations.

- Slight recent decline in quarterly revenue growth.

- Limited dividend yield relative to some peers.

Opportunities

- Expansion of digital banking and HRMS services enhancing operational efficiency.

- Active management of non-performing assets through auctions and recoveries.

- Growing demand for SME and retail banking products in India.

- Potential for increased institutional investor interest.

Threats

- Operational disruptions from nationwide bank strike calls.

- Competitive pressures from private sector and new fintech entrants.

- Macroeconomic uncertainties affecting credit quality.

- Negative public sentiment related to security incidents.

Company Description

Punjab National Bank is a prominent public sector bank in India, providing a range of banking and financial services to individuals, businesses, and corporations. Established in 1894, this bank is one of India's oldest and most trusted financial institutions. Its primary function is deposit mobilization, offering products like savings accounts, current accounts, and fixed deposits. Punjab National Bank also plays a critical role in lending through personal loans, home loans, and credit facilities to small and medium enterprises (SMEs), thereby significantly contributing to the country's economic growth. Notable for its extensive network, Punjab National Bank operates a large number of branches across urban and rural areas, facilitating financial inclusion by providing banking services to underserved regions. It also engages in treasury operations, international banking, and offers services such as wealth management, insurance, and investment solutions. In the financial market, Punjab National Bank holds significant importance, managing a substantial portion of the domestic banking sector's assets and liabilities. Its historical legacy, extensive reach, and comprehensive service offerings make it a key player in supporting India's financial ecosystem.