NOCIL Ltd (NOCIL)

Stock Analysis Report

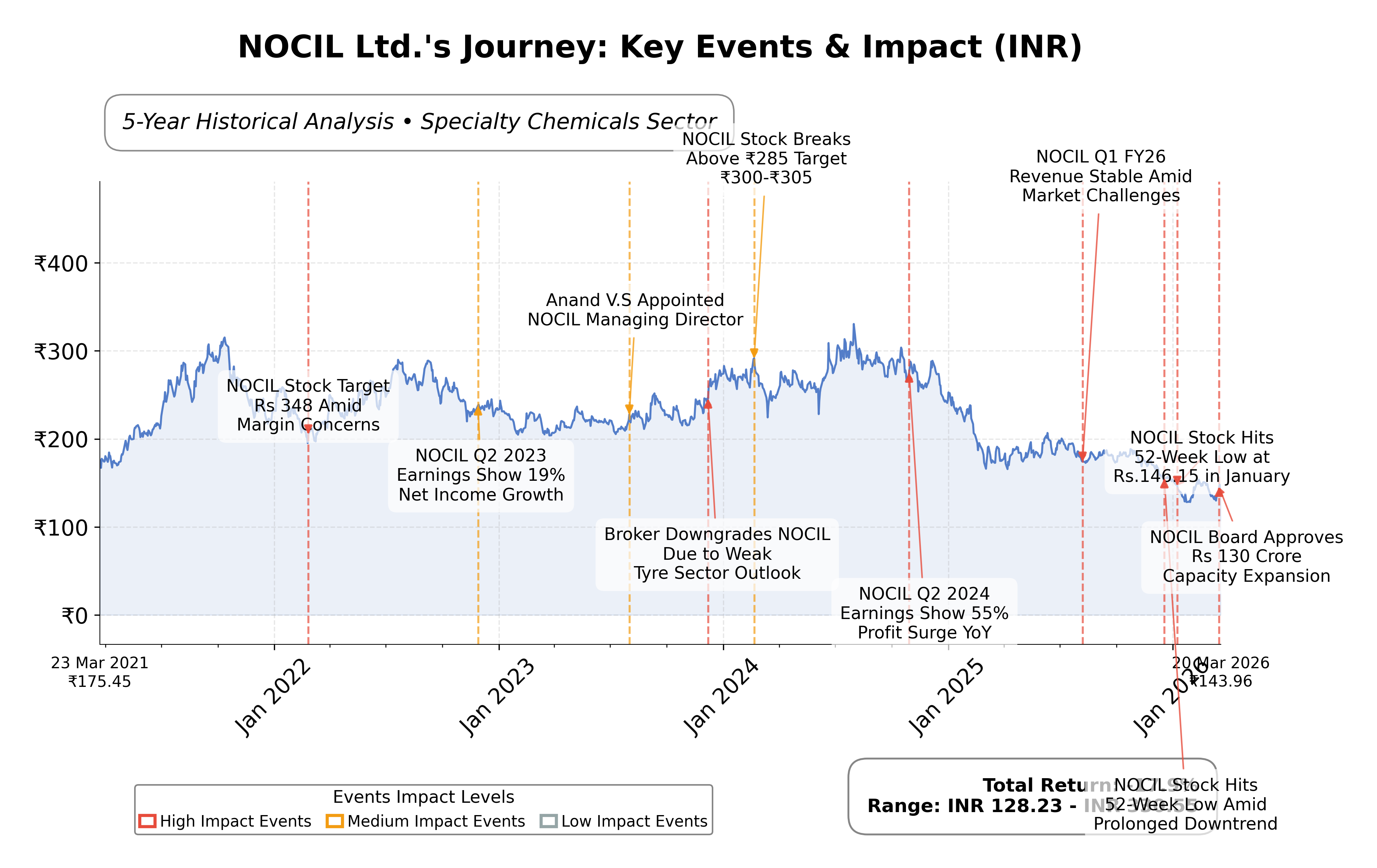

Stock Journey

Key Positives and Key Risks

Pros

- Strong liquidity with a current ratio of 5.82 and low total debt of ₹93.4 million supports financial stability.

- Forward P/E ratio of 23.22 is lower than trailing P/E of 40.44, indicating potential valuation moderation.

- Capacity expansion at Dahej plant with ₹130 crore investment signals growth initiatives.

Cons

- Negative quarterly revenue growth of -0.7% and year-over-year earnings decline of 28.3% indicate near-term performance challenges.

- High price-to-cash-flow ratio of 145.02 suggests potential overvaluation relative to cash flow generation.

- Return on equity is modest at approximately 5.84%, below several industry peers.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

NOCIL Ltd. operates as a leading manufacturer in the specialty chemicals sector, focusing primarily on rubber chemicals essential for the rubber and tire industries. Positioned as the largest rubber chemical manufacturer in India, the company supports automotive and industrial applications with a broad product portfolio including accelerators and anti-degradants. Its operations are headquartered in Mumbai, and it maintains a global outlook emphasizing innovation and sustainability within the basic materials sector.

Financially, NOCIL reports a market capitalization of approximately â¹24.04 billion with a trailing P/E ratio of 40.44 and a forward P/E of 23.22, reflecting valuation metrics somewhat elevated relative to earnings growth. The companyâs revenue for the trailing twelve months stands near â¹13.12 billion, with a modest profit margin of 4.53% and a return on equity of approximately 5.84%. Liquidity appears strong with a current ratio above 5.8 and low debt levels, while dividend yield is near 4.99% forward, indicating shareholder returns alongside operational cash flow generation.

From a technical and strategic perspective, recent initiatives include a â¹130 crore capacity expansion at the Dahej plant, signaling growth ambitions. Technical indicators show mixed momentum with recent price surges contrasted by some bearish signals, reflecting market uncertainty. Insider shareholding is around 42%, with institutional holdings near 8%, suggesting stable ownership but limited institutional accumulation. Key risks include earnings volatility and sector cyclicality, while strengths lie in market leadership and product specialization.

Peer analysis within the Indian specialty chemicals industry shows NOCIL as a smaller-cap player relative to peers like Aarti Industries and Jubilant Ingrevia, with valuation multiples generally lower than some larger peers but higher than others such as Balaji Amines. Return on equity is modest compared to industry leaders, and valuation metrics such as EV/EBITDA and price-to-CFO ratios indicate a mixed financial profile. This positions NOCIL as a niche participant with room for operational leverage and growth.

NOCIL navigates a competitive and evolving industry landscape marked by capacity expansions and shifting market dynamics. Recent achievements include strategic capital investments and operational resilience, while challenges persist in maintaining earnings growth and managing market sentiment. The company stands at a pivotal juncture where its capacity enhancements and financial discipline could influence future positioning. Given the current data, a balanced stance reflecting cautious observation of operational execution and market developments may be appropriate for those assessing the companyâs equity.

Company and Industry Overview

Company Basics

Price Performance

Company Size

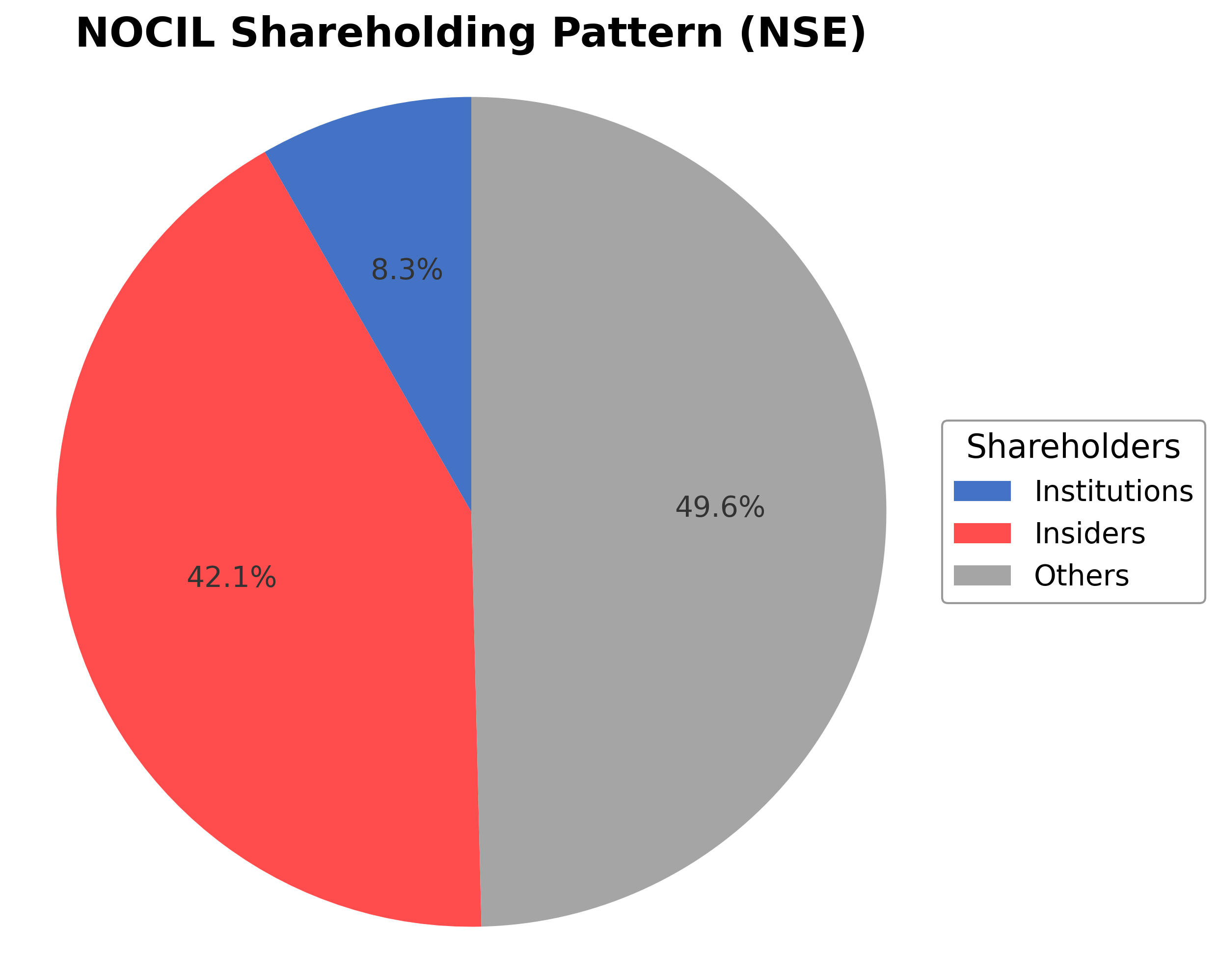

Shareholding Pattern

NOCIL Ltd.'s shareholding structure comprises approximately 42.10% held by insiders including executives and board members, 8.29% by institutional investors such as mutual funds and asset managers, and the remaining 49.61% by public shareholders including retail investors and employee stock plans. Over the past 12-24 months, insider holdings have remained relatively stable, while institutional ownership has seen minor fluctuations without significant accumulation or distribution trends. Major institutional stakeholders have maintained consistent positions, reflecting a neutral market sentiment. This ownership distribution suggests a governance framework with strong promoter influence balanced by public participation, which may impact strategic decisions and corporate actions in line with industry norms within the Indian specialty chemicals sector.

Sector and Industry Analysis

NOCIL Ltd operates within the Indian specialty chemicals sector, specifically focusing on rubber chemicals, a niche but critical segment of the broader chemical industry. The specialty chemicals sector in India is sizable and growing, driven by expanding end-use industries such as automotive, manufacturing, and infrastructure. The Indian specialty chemicals market is projected to grow at a CAGR of approximately 9-11% over the next five years, fueled by increasing domestic demand and export opportunities. Key players in this sector include both domestic firms like NOCIL and multinational corporations such as Dow Inc. and LyondellBasell Industries, which compete on technology, product quality, and global supply chain integration.

Industry trends in the specialty chemicals space are shaped by technological advancements emphasizing sustainable and eco-friendly chemical formulations, driven by growing environmental awareness and regulatory pressures. There is a notable shift towards green chemistry and bio-based chemicals, with companies investing in R&D to develop products that reduce environmental impact. Consumer behavior in downstream industries, particularly automotive and tire manufacturing, is evolving with a preference for higher-performance and longer-lasting materials, which increases demand for advanced rubber chemicals. Emerging opportunities include the development of specialty additives for electric vehicle tires and industrial applications, as well as expanding exports to emerging markets in Asia and Africa.

The regulatory landscape for specialty chemicals in India is complex and evolving, governed by agencies such as the Ministry of Environment, Forest and Climate Change (MoEFCC) and the Central Pollution Control Board (CPCB). Compliance with environmental regulations related to emissions, effluent treatment, and chemical handling is mandatory, with increasing enforcement of hazardous waste management and chemical safety standards under the Manufacture, Storage and Import of Hazardous Chemical Rules. Additionally, policies promoting Make in India and export incentives support domestic manufacturing growth but also impose quality and safety standards aligned with global norms. Regulatory uncertainty and evolving standards require companies to maintain robust compliance frameworks and invest in sustainable manufacturing processes.

Competitive dynamics in the rubber chemicals industry are characterized by moderate concentration with a few large incumbents like NOCIL commanding significant market share due to established customer relationships, technical expertise, and backward integration capabilities. Barriers to entry include high capital intensity, stringent environmental compliance, and the need for specialized R&D capabilities to innovate product formulations. Competitive positioning hinges on product quality, cost efficiency, and the ability to customize solutions for diverse industrial applications. Global players leverage scale and technology transfer, while domestic firms focus on cost competitiveness and local market knowledge. The industry also experiences cyclical demand linked to the automotive and manufacturing sectors, necessitating operational agility and diversified product portfolios.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

Financials

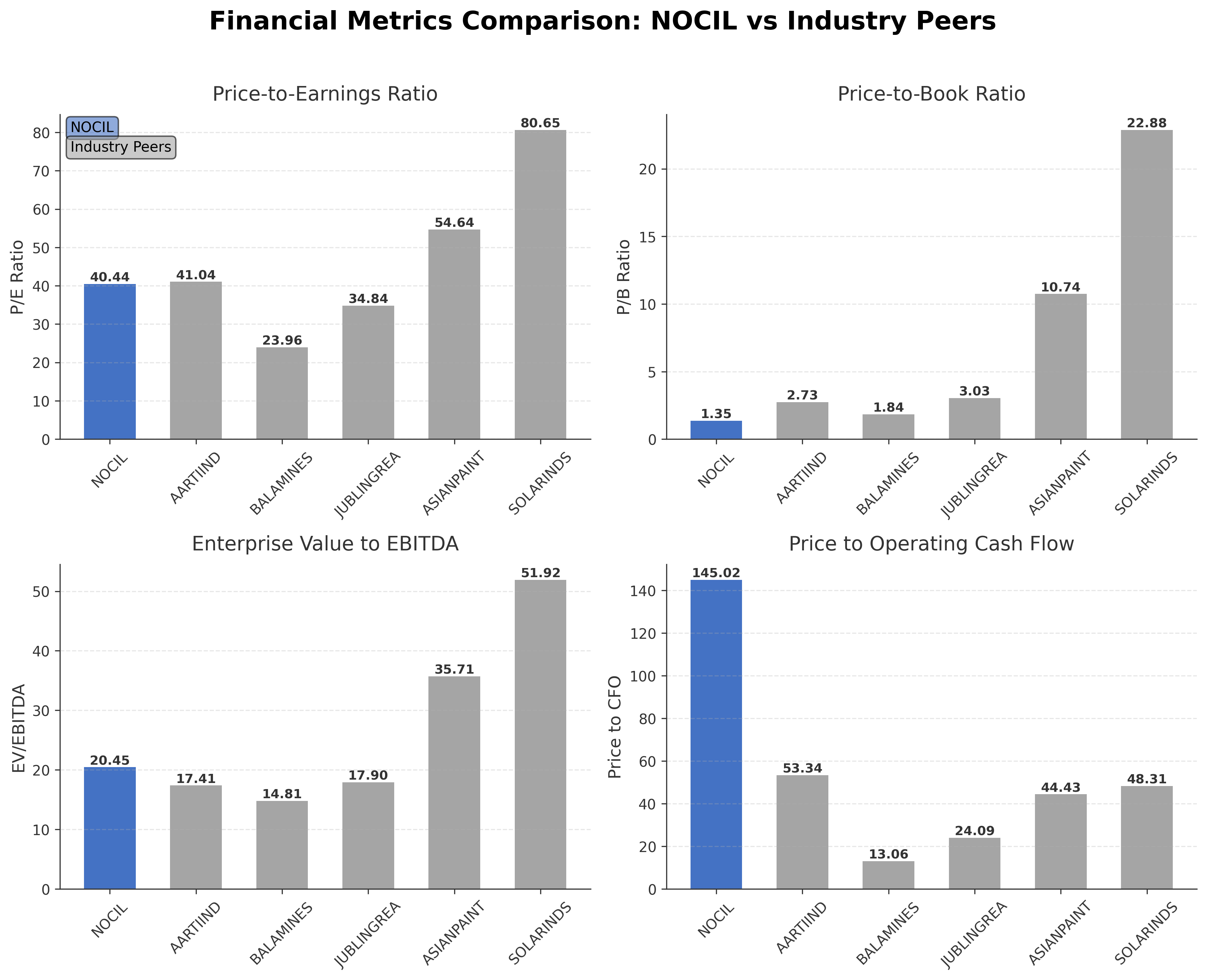

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| NOCIL Ltd. | ₹24.04B | 40.44 | 1.35 | 20.45 | 145.02 |

| Aarti Industries Ltd. | ₹155.19B | 41.04 | 2.73 | 17.41 | 53.34 |

| Balaji Amines Ltd. | ₹34.58B | 23.96 | 1.84 | 14.81 | 13.06 |

| Jubilant Ingrevia Ltd. | ₹92.22B | 34.84 | 3.03 | 17.9 | 24.09 |

| Asian Paints Ltd. | ₹2.10T | 54.64 | 10.74 | 35.71 | 44.43 |

| Solar Industries India Ltd. | ₹1.17T | 80.65 | 22.88 | 51.92 | 48.31 |

Comparison Analysis: NOCIL Ltd. is positioned as a smaller-cap entity within the Indian specialty chemicals sector compared to peers such as Aarti Industries and Jubilant Ingrevia. Its P/E ratio of 40.44 aligns closely with Aarti Industries but is higher than Balaji Amines and Jubilant Ingrevia, indicating relatively elevated valuation. The price-to-book ratio at 1.35 is lower than most peers, suggesting a more conservative valuation on book value. NOCIL's EV/EBITDA multiple of 20.45 is moderate but higher than Balaji Amines, reflecting operational leverage differences. The notably high price-to-CFO ratio at 145.02 contrasts with peers, indicating potential cash flow valuation disparities. Return on equity is modest at 6%, below larger peers like Asian Paints and Solar Industries, highlighting opportunities for improved profitability.

Financial Metrics Comparison with Peers

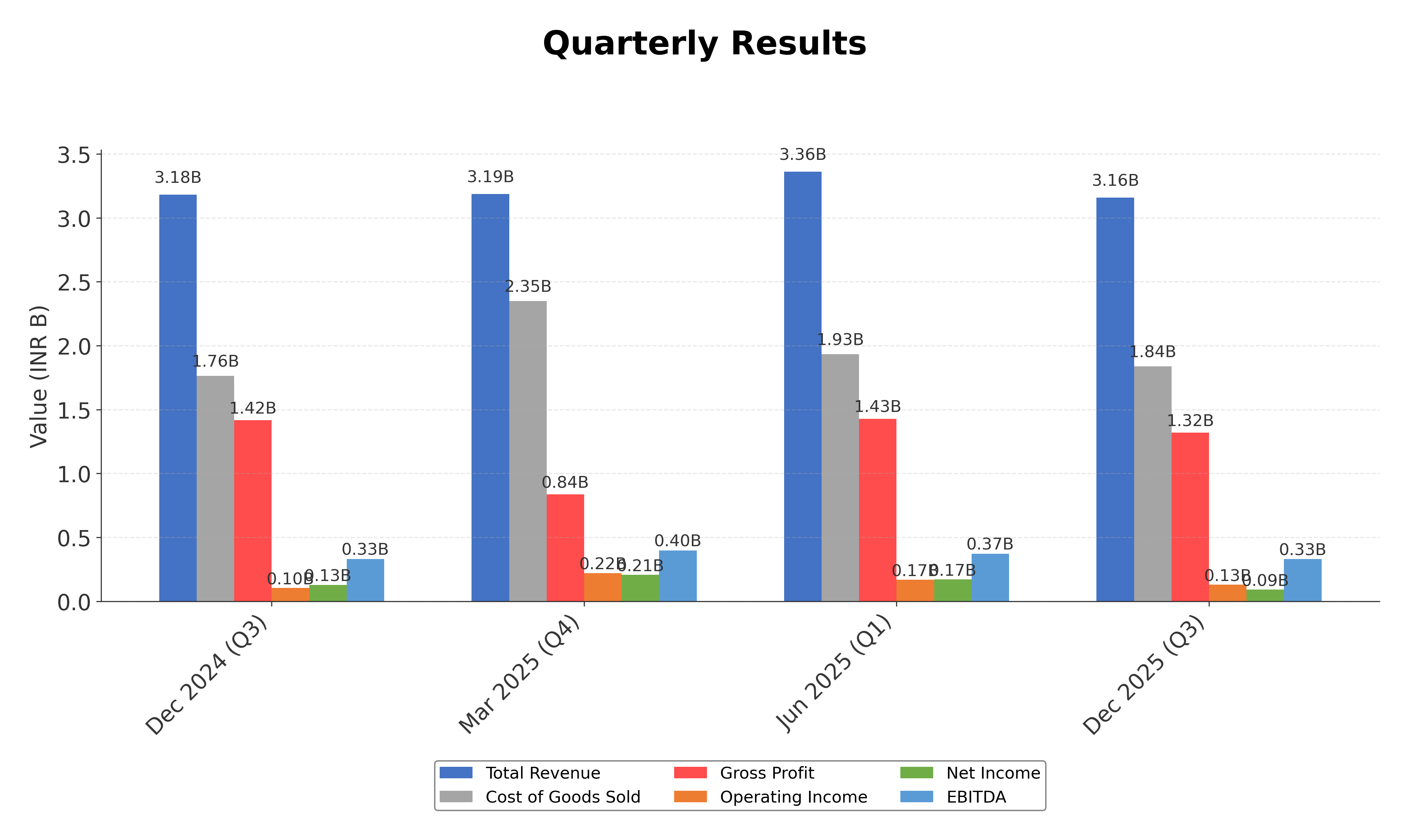

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 13.72B | 14.37B | 16.11B | 15.61B | 9.13B |

| Cost Of Goods | 8.35B | 8.50B | 9.28B | 8.97B | 5.31B |

| Gross Profit | 5.37B | 5.88B | 6.83B | 6.64B | 3.82B |

| Operating Expense Selling General And Administrative | 1.17B | 1.02B | 1.07B | 1.09B | 745.20M |

| Operating Expense Other Operating Expenses | 2.07B | 2.04B | 2.38B | 1.94B | 1.16B |

| Operating Income | 852.40M | 1.42B | 1.98B | 2.39B | 942.00M |

| Non Operating Interest Income | 212.40M | 166.90M | 43.70M | 11.10M | 117.60M |

| Non Operating Interest Expense | 17.90M | 16.20M | 12.00M | 10.90M | 9.70M |

| Pretax Income | 1.14B | 1.80B | 2.02B | 2.41B | 1.07B |

| Income Tax | 112.80M | 469.90M | 529.40M | 645.10M | 187.20M |

| Net Income | 1.03B | 1.33B | 1.49B | 1.76B | 884.10M |

| Eps Basic | 6.17 | 7.98 | 8.95 | 10.58 | 5.33 |

| Eps Diluted | 6.15 | 7.95 | 8.92 | 10.55 | 5.32 |

| Basic Shares Outstanding | 166.83M | 166.65M | 166.62M | 166.44M | 165.87M |

| Diluted Shares Outstanding | 166.83M | 166.65M | 166.62M | 166.44M | 165.87M |

| Ebit | 1.16B | 1.82B | 2.03B | 2.42B | 1.08B |

| Ebitda | 1.61B | 2.13B | 2.58B | 2.90B | 1.44B |

| Net Income Continuous Operations | 1.14B | 1.80B | 2.02B | 2.41B | 1.07B |

| Minority Interests | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Preferred Stock Dividends | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 299.40M | 918.00M | 235.70M | 121.70M | 448.50M |

| Accounts Receivable | 3.10B | 3.40B | 3.46B | 4.50B | 3.09B |

| Total Assets | 20.57B | 20.15B | 18.57B | 18.30B | 16.15B |

| Total Liabilities | 2.95B | 3.17B | 3.05B | 3.85B | 3.30B |

| Long Term Debt | 71.30M | 108.60M | 68.30M | 28.60M | 38.60M |

| Shareholders Equity | 17.62B | 16.99B | 15.52B | 14.45B | 12.85B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 1.14B | 1.80B | 2.02B | 2.41B | 1.07B |

| Operating Activities Stock Based Compensation | 30.10M | 7.80M | 13.80M | 3.70M | 9.60M |

| Operating Activities Other Non Cash Items | -204.70M | -162.50M | -36.00M | -4.10M | -112.50M |

| Operating Activities Accounts Receivable | 304.50M | 81.20M | 1.06B | -1.39B | -1.04B |

| Operating Activities Other Assets Liabilities | -1.11B | 522.30M | 633.90M | -1.62B | -134.30M |

| Operating Activities Operating Cash Flow | 165.80M | 2.25B | 3.69B | -606.60M | -207.70M |

| Investing Activities Capital Expenditures | -1.20B | -159.10M | -291.30M | -333.40M | -261.80M |

| Investing Activities Net Intangibles | -5.70M | -9.90M | -2.80M | -28.60M | -3.60M |

| Investing Activities Purchase Of Investments | -7.06B | -7.76B | -3.19B | -1.79B | -1.36B |

| Investing Activities Sale Of Investments | 7.68B | 7.03B | 1.29B | 2.45B | 987.50M |

| Investing Activities Other Investing Activity | 3.30M | 3.70M | 4.10M | 3.90M | 4.60M |

| Investing Activities Investing Cash Flow | -583.30M | -886.00M | -2.19B | 323.50M | -632.90M |

| Financing Activities Long Term Debt Issuance | 40.50M | 220.10M | 200.00M | 400.60M | 0.00 |

| Financing Activities Long Term Debt Payments | -40.50M | -220.10M | -200.00M | -400.60M | 0.00 |

| Financing Activities Common Stock Issuance | 46.80M | 500.00K | 11.50M | 29.10M | 37.00M |

| Financing Activities Common Dividends | -502.20M | -500.70M | -499.90M | -331.70M | -7.10M |

| Financing Activities Financing Cash Flow | -455.40M | -500.20M | -488.40M | -302.60M | 29.90M |

| End Cash Position | 299.50M | 918.00M | 235.70M | 121.70M | 448.50M |

| Free Cash Flow | -975.60M | 1.65B | 2.52B | -664.40M | 666.10M |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend shows mixed price action with recent upward momentum evidenced by a 6.92% surge, though broader indicators suggest volatility.

- Key support levels are identified near ₹125.31 (52-week low) and around the 50-day moving average at ₹139.87, while resistance is observed near the 52-week high of ₹211 and the 200-day moving average at ₹167.78.

- The stock price is currently above the 50-day moving average but below the 200-day moving average, indicating intermediate-term strength with longer-term resistance.

- Momentum indicators present mixed signals: RSI levels suggest neutral momentum, MACD shows recent bullish crossover but with weakening histogram, and stochastic oscillators indicate potential overbought conditions.

- Multi-timeframe analysis reveals daily charts with short-term bullishness, weekly charts showing consolidation, and monthly charts indicating a longer-term sideways trend.

- Potential market scenarios include continuation of short-term rallies if support holds, or a pullback towards key moving averages if resistance levels prove strong.

Trending News

1. Headline: NOCIL Ltd is Rated Strong Sell

Summary: NOCIL Ltd is rated Strong Sell by MarketsMOJO, with this rating last updated on 06 Feb 2025. However, the analysis and financial metrics discussed here reflect the company’s current position as of 18 March 2026, providing investors with an up-to-date view of the stock’s fundamentals, valuation, ...

Sentiment: neutral

2. Headline: NOCIL Ltd Technical Momentum Shifts Amid Mixed Indicator Signals

Summary: NOCIL Ltd, a small-cap player in the Specialty Chemicals sector, has experienced a notable shift in its technical momentum, reflected in a 6.92% surge in its share price to ₹146.00 on 18 Mar 2026. Despite this intraday strength, the stock’s broader technical indicators present a complex ...

Sentiment: positive

3. Headline: NOCIL Board Approves ₹130 Crore Dahej Plant Expansion for Rubber Chemicals

Summary: Gurukripa Trust pledged 9,00,000 NOCIL shares (0.54% of total capital) to Aditya Birla Capital Ltd for loan purposes on March 05, 2026. The trust, holding 18.16% stake in NOCIL, now has total encumbered shares of 67,00,000 (4.01%).

Sentiment: neutral

4. Headline: NOCIL Approves Capacity Expansion At Dahej Plant — TradingView News

Summary: Nocil Ltd NSE:NOCIL:

Sentiment: positive

5. Headline: Indices trade with minor cuts; VIX drops over 5% | Capital Market News - Business Standard

Summary: IT shares declined for sixth consecutive trading session.

Sentiment: negative

6. Headline: Top stocks in news: RIL, AEL, Tata Motors, RVNL, Sun Pharma, LTTS, Zydus Life, GMDC, Nocil - BusinessToday

Summary: Stocks including RIL, Adani Enterprises, Tata Motors, RVNL, Sun Pharma, LTTS, Zydus Life, GMDC, Power Mech, NOCIL and more will be in the spotlight on Tuesday, March 17.

Sentiment: neutral

7. Headline: Northern Right Dumps 790,000 NCLH Shares Worth $19.5 Million | The Motley Fool

Summary: Norwegian Cruise Line Holdings operates a global fleet across multiple brands, catering to premium and luxury travel markets worldwide.

Sentiment: negative

8. Headline: NOCIL Ltd,NOCIL Ltd LIVE, NOCIL Ltd price NSE, NOCIL Ltd price BSE, NOCIL Ltdprice today, Live Price today

Summary: NOCIL Ltd share price today. Find NOCIL Ltd price live updates on MarketsMojo. NOCIL Ltd price, NOCIL Ltd share price, NSE/BSE details with 52 week high/low, dividend, technical, result analysis

Sentiment: neutral

9. Headline: NOCIL Ltd Technical Momentum Shifts Amid Bearish Sentiment

Summary: NOCIL Ltd, a key player in the specialty chemicals sector, has experienced a notable shift in its technical momentum, with recent indicators signalling a bearish trend. Despite some mixed signals from monthly and weekly oscillators, the overall technical outlook has deteriorated, prompting ...

Sentiment: negative

10. Headline: From uniforms to AI, Arvind Mafatlal Group aims to be a forerunner in education sector - The Economic Times

Summary: Mafatlal Industries, which has a legacy spanning over 120 years, is a leading player in school, corporate and hospital uniforms. The other group firms include rubber chemicals maker NOCIL Ltd, future skills-focused learning startup Get Set Learn, and IT firm Vrata Tech Solutions.

Sentiment: neutral

Powered by Brave

Recent Updates

News Summary

Recent news coverage of NOCIL Ltd highlights a strategic focus on capacity expansion, particularly with the Board's approval of a ₹130 crore investment at the Dahej plant to boost rubber chemical production. This development aligns with the company's growth ambitions in the specialty chemicals sector. Technical momentum has shown mixed signals, with a recent price surge tempered by broader indicator uncertainty. Market sentiment remains cautious, reflected in a Strong Sell rating by MarketsMOJO as of early 2025, though some technical analyses indicate short-term positive shifts. The company’s financial metrics and operational initiatives suggest a balancing act between sustaining growth and managing valuation pressures within a competitive industry environment.

News Sentiment

Sentiment across recent news is mixed to neutral, with positive undertones from capacity expansion announcements and technical momentum shifts, counterbalanced by cautious market ratings and sector volatility. The overall tone reflects measured optimism tempered by recognition of challenges in sustaining earnings growth and navigating market conditions.

Analytical Overview

Analysis Summary

NOCIL Ltd’s valuation metrics show a trailing P/E of 40.44 and forward P/E of 23.22, which are in line with the specialty chemicals industry average P/E of 40.44, indicating valuation consistent with sector norms but elevated relative to earnings growth. The price-to-book ratio of 1.35 is comparatively lower than many peers, suggesting a more conservative valuation on net assets.

The company’s revenue growth is slightly negative at -0.7% quarterly, with operating cash flow positive but modest at ₹165.8 million TTM and free cash flow at ₹1.03 billion TTM, indicating stable but cautious growth trajectory. Earnings growth has declined year-over-year by approximately 28.3%, highlighting near-term challenges.

Financial health appears solid with a low total debt to equity ratio of 0.53 and a strong current ratio above 5.8, reflecting ample liquidity and manageable leverage. Cash reserves exceed ₹3 billion, supporting operational flexibility.

Sector-specific challenges include cyclical demand in the rubber chemicals market and competitive pressures, while opportunities arise from capacity expansions and increasing focus on sustainability. India-specific factors such as regulatory environment and growing automotive sector demand may influence future performance.

Investment Conclusion

Supporting Factors: Primary supporting factors include strong liquidity and low leverage, strategic capacity expansion at Dahej, and market leadership in rubber chemicals within India.

Risk Factors: Main risk factors to monitor are earnings growth volatility, sector cyclicality, and market sentiment shifts reflected in technical indicators.

SWOT Analysis

Strengths

- Market leader in rubber chemicals in India with a comprehensive product portfolio.

- Strong liquidity position with a current ratio above 5.8 and low debt levels.

- Strategic capacity expansion approved at Dahej plant to support growth.

- Focus on sustainability and adherence to environmental standards.

Weaknesses

- Modest profit margins and return on equity indicating limited profitability.

- Negative quarterly revenue growth and declining earnings year-over-year.

- High price-to-cash-flow ratio suggesting potential overvaluation in cash flow terms.

- Relatively low institutional ownership limiting broader market support.

Opportunities

- Growing demand in automotive and industrial rubber sectors in India.

- Capacity expansion could enhance production capabilities and market share.

- Increasing focus on specialty chemicals with sustainability trends.

- Potential to improve operational efficiencies and profitability.

Threats

- Cyclical nature of the rubber chemicals industry impacting earnings stability.

- Competitive pressures from larger and diversified chemical manufacturers.

- Market volatility reflected in mixed technical momentum and bearish signals.

- Regulatory changes affecting chemical manufacturing and environmental compliance.

Company Description

NOCIL Ltd. is a prominent player in the chemical manufacturing sector, specializing in the production of rubber chemicals. It serves a critical function in supplying essential components for the rubber and tire industries, which are fundamental to automotive and industrial applications worldwide. Notable for its comprehensive portfolio, NOCIL Ltd. offers a range of products including accelerators, anti-degradants, and specialty chemicals used to enhance the durability and performance of rubber products. As the largest rubber chemical manufacturer in India, the company's influence extends both domestically and internationally, ensuring competitive advantage through innovation and quality. Recognized for its strong focus on sustainability and adherence to stringent environmental standards, NOCIL Ltd. operates with a global outlook from its headquarters in Mumbai. By supporting the performance and longevity of rubber goods, NOCIL Ltd. holds a significant role in the supply chain, highlighting the intersection of industrial growth and environmental responsibility within the financial markets.