LIC Housing Finance Ltd (LICHSGFIN)

Stock Analysis Report

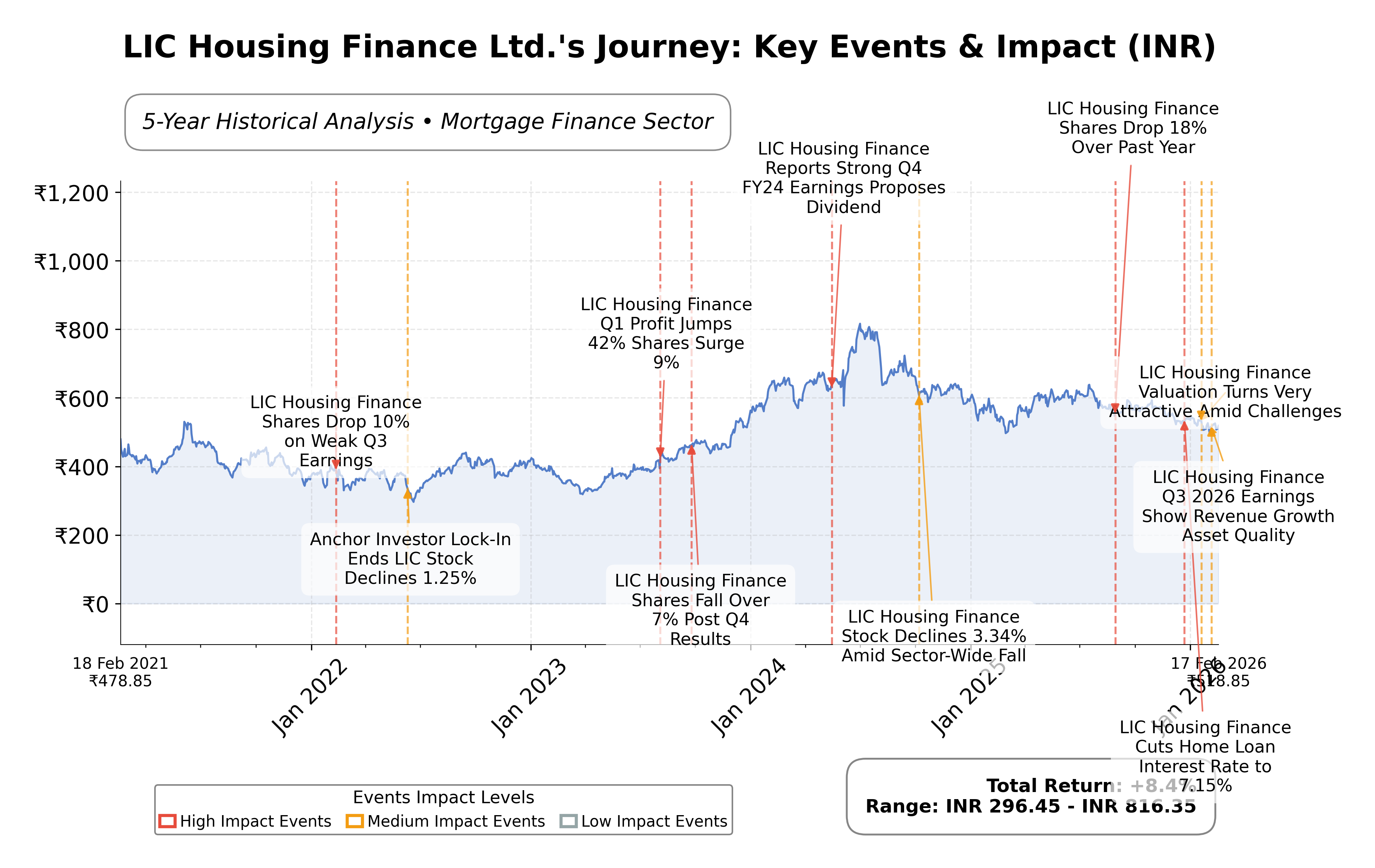

Stock Journey

Key Positives and Key Risks

Pros

- Low trailing P/E ratio of 5.09 indicates potential undervaluation relative to industry peers.

- Strong profit margin of 65.18% and operating margin of 83.05% demonstrate operational efficiency.

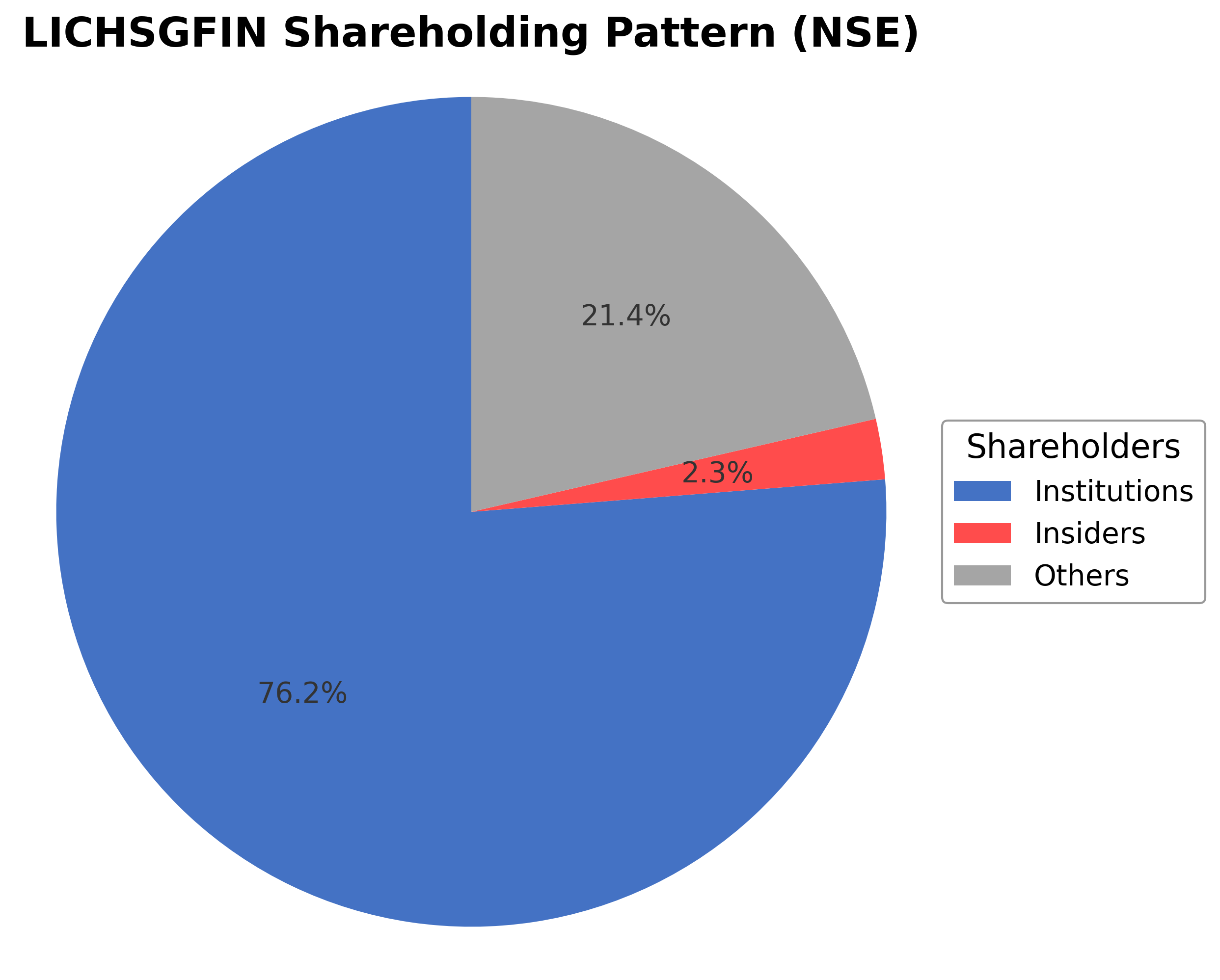

- High institutional ownership at 76.25% suggests stable governance and investor confidence.

Cons

- Elevated debt-to-equity ratio of 7.22 reflects significant financial leverage and associated risks.

- Negative operating cash flow of ₹-14.10 billion raises concerns about cash generation capabilities.

- Price to cash flow ratio is negative (-19.80), indicating cash flow inefficiencies.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

LIC Housing Finance Ltd. operates primarily in the mortgage finance industry in India, focusing on providing long-term housing loans to individuals, builders, and corporate entities. As a subsidiary of Life Insurance Corporation of India, the company leverages strong brand trust and extensive distribution networks to support home ownership and government housing initiatives. Its core business underpins the real estate sector by bridging financial gaps for prospective homeowners, positioning it as a key player in India's housing finance market.

Financially, LIC Housing Finance reports a market capitalization of approximately â¹279.24 billion with a trailing P/E ratio of 5.09 and a forward P/E of 4.91, indicating relatively low valuation multiples compared to industry peers. The company shows a profit margin of 65.18% and an operating margin of 83.05%, with a return on equity around 15%. Despite a slight decline in quarterly revenue and earnings growth, the firm maintains a substantial net income of â¹54.85 billion and a dividend yield near 1.97%, supported by a payout ratio of 10%. However, the company carries significant debt, with a debt-to-equity ratio exceeding 7.2.

From a strategic and technical perspective, LIC Housing Finance has maintained steady revenue growth but faces challenges from negative operating cash flow and high leverage. The companyâs shareholding pattern reveals strong institutional ownership at approximately 76%, with minimal insider holdings, suggesting stable governance. The stock trades below its 52-week high, with technical indicators showing a price below the 200-day moving average, reflecting cautious market sentiment. No recent leadership changes or major strategic shifts have been reported, though ongoing macroeconomic factors and regulatory environment remain critical considerations.

In comparison to regional peers such as Can Fin Homes, PNB Housing Finance, and Aadhar Housing Finance, LIC Housing Finance exhibits lower valuation multiples, particularly in P/E and P/B ratios, signaling potential undervaluation or market concerns regarding growth prospects. Its market capitalization is among the largest in the sector, but its price to cash flow ratio is negative, contrasting with some peers exhibiting positive cash flow metrics. This peer context highlights both competitive strengths and areas requiring attention.

LIC Housing Finance stands at a pivotal juncture within the Indian housing finance sector, balancing robust profitability against elevated leverage and cash flow challenges. The companyâs established market position and backing by a major insurance entity provide resilience, yet the evolving economic landscape and sector-specific risks present ongoing challenges. The outcomes of current strategies and market conditions will significantly influence its trajectory, with implications for financial stability and growth potential. Observers may find a neutral stance appropriate, monitoring developments closely to assess future performance dynamics.

Company and Industry Overview

Company Basics

Price Performance

Company Size

Shareholding Pattern

LIC Housing Finance Ltd.'s ownership structure is characterized by a dominant institutional investor presence at 76.25%, with insiders holding approximately 2.35%. The remaining shares are held by other shareholders, including retail investors and employee stock plans, though specific percentages are not detailed. Over the past 12-24 months, institutional accumulation appears stable with no significant shifts reported. Major investment firms maintain consistent positions, reflecting steady market confidence. This ownership pattern suggests strong governance oversight and strategic alignment with institutional priorities, potentially influencing corporate actions and long-term planning within the mortgage finance sector in India.

Sector and Industry Analysis

LIC Housing Finance Ltd. (LICHSGFIN) operates within the Indian housing finance sector, a critical sub-segment of the broader financial services industry focused on mortgage lending and related credit products. The housing finance sector in India has witnessed robust growth over the past decade, driven by rising urbanization, increasing disposable incomes, and government initiatives promoting affordable housing. The market size is substantial, with outstanding housing loans exceeding several trillion INR, and is expected to maintain a healthy compound annual growth rate (CAGR) in the mid-to-high single digits, supported by sustained demand for home ownership and real estate development. Key players include LIC Housing Finance, HDFC Ltd., and other non-banking financial companies (NBFCs) specializing in housing finance, alongside banks with significant mortgage portfolios.

Industry trends reveal a gradual but marked shift towards digitization and technology integration in underwriting, loan processing, and customer engagement. The adoption of data analytics, AI-driven credit scoring, and online platforms has enhanced efficiency and customer experience, enabling faster approvals and better risk management. Consumer behavior is evolving with millennials and first-time homebuyers increasingly seeking transparent, convenient, and customized financing solutions. Additionally, there is a growing emphasis on affordable housing loans and green home financing, reflecting both regulatory encouragement and market demand. Emerging opportunities lie in tier-2 and tier-3 cities, where housing demand is rising, and in leveraging government schemes such as the Pradhan Mantri Awas Yojana (PMAY) to expand the borrower base.

The regulatory landscape governing the housing finance sector in India is shaped primarily by the National Housing Bank (NHB), which acts as the sector’s regulator, alongside the Reserve Bank of India (RBI) for NBFCs and banks. Key regulations include capital adequacy norms, provisioning requirements, and guidelines on loan-to-value ratios and interest rate disclosures. Compliance with anti-money laundering (AML) and know-your-customer (KYC) norms is stringent, given the sector’s sensitivity to fraud and credit risk. Policy initiatives such as tax incentives on home loans and subsidies under affordable housing schemes materially impact demand and lending patterns. Regulatory stability and clarity remain crucial for sustaining investor confidence and sector growth.

Competitive dynamics in the housing finance industry are characterized by a mix of large, well-capitalized institutions and smaller NBFCs, creating a moderately concentrated market with significant competitive intensity. Barriers to entry include regulatory compliance costs, the need for extensive distribution networks, and the requirement for robust risk management frameworks. LIC Housing Finance benefits from its association with the Life Insurance Corporation of India, providing brand strength and access to a broad customer base. However, competition from banks offering competitive interest rates and fintech platforms innovating in customer acquisition and loan servicing is intensifying. Market positioning hinges on product differentiation, pricing strategies, and the ability to leverage technology for operational efficiency and customer retention.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

Financials

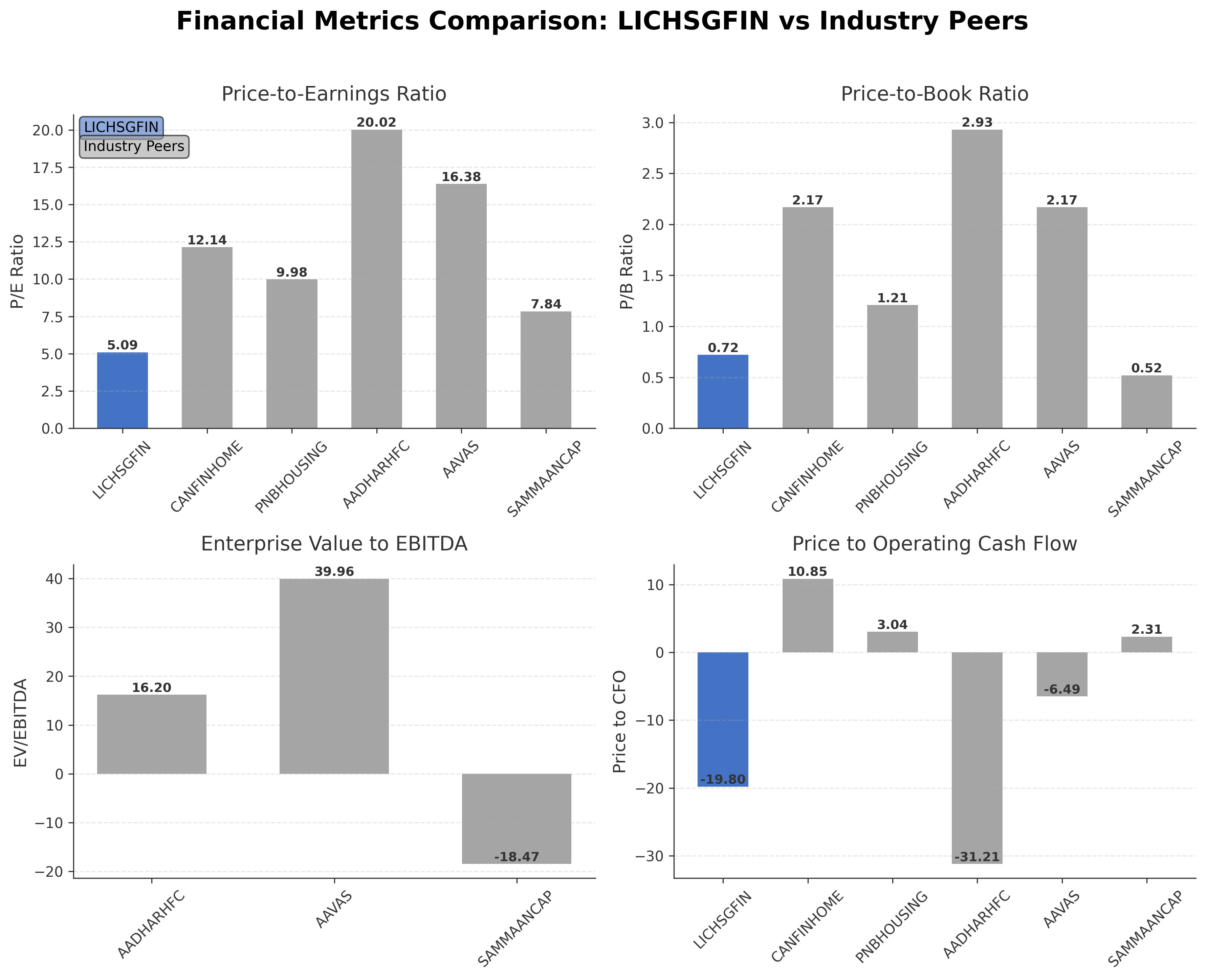

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| LIC Housing Finance Ltd. | ₹279.24B | 5.09 | 0.72 | N/A | -19.80 |

| Can Fin Homes Ltd. | ₹117.77B | 12.14 | 2.17 | N/A | 10.85 |

| PNB Housing Finance Ltd. | ₹217.80B | 9.98 | 1.21 | N/A | 3.04 |

| Aadhar Housing Finance Ltd. | ₹202.43B | 20.02 | 2.93 | 16.20 | -31.21 |

| Aavas Financiers Ltd. | ₹101.89B | 16.38 | 2.17 | 39.96 | -6.49 |

| Sammaan Capital Ltd. | ₹117.51B | 7.84 | 0.52 | -18.47 | 2.31 |

Comparison Analysis: LIC Housing Finance Ltd. presents lower P/E and P/B ratios compared to its regional peers, indicating a more conservative valuation. Its market capitalization is the largest among the group, reflecting its significant scale in the mortgage finance sector. However, the company’s negative price to cash flow ratio contrasts with several peers showing positive cash flow metrics, highlighting potential operational cash flow concerns. Peers such as Can Fin Homes and PNB Housing Finance exhibit higher valuation multiples, suggesting expectations of stronger growth or profitability. Overall, LIC Housing Finance stands out for its scale and valuation but faces challenges in cash flow efficiency relative to competitors.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 81.95B | 87.17B | 63.80B | 56.66B | 52.72B |

| Operating Expense Selling General And Administrative | 594.80M | 580.70M | 551.10M | 397.10M | 589.00M |

| Operating Expense Other Operating Expenses | 3.55B | 2.35B | 2.12B | 1.92B | 1.57B |

| Pretax Income | 68.79B | 60.64B | 35.61B | 27.87B | 33.65B |

| Income Tax | 14.36B | 13.05B | 6.70B | 5.01B | 6.24B |

| Net Income | 54.43B | 47.60B | 28.91B | 22.86B | 27.41B |

| Eps Basic | 98.95 | 86.52 | 52.55 | 43.12 | 54.32 |

| Eps Diluted | 98.95 | 86.52 | 52.55 | 43.12 | 54.32 |

| Basic Shares Outstanding | 550.06M | 550.06M | 550.06M | 530.16M | 504.66M |

| Diluted Shares Outstanding | 550.06M | 550.06M | 550.06M | 530.16M | 504.66M |

| Net Income Continuous Operations | 68.79B | 60.64B | 35.61B | 27.78B | 33.65B |

| Minority Interests | -4.70M | -3.50M | -4.10M | -3.50M | -4.10M |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-09-30 | 2024-03-31 | 2023-09-30 | 2023-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 14.38B | 10.11B | 16.80B | 16.58B | 8.44B |

| Accounts Receivable | N/A | N/A | N/A | N/A | N/A |

| Total Assets | 3140.40B | 2993.15B | 2913.34B | N/A | N/A |

| Total Liabilities | 2776.85B | 2657.00B | 2598.54B | N/A | N/A |

| Long Term Debt | 2625.38B | 2500.92B | 2431.98B | 2327.28B | 2339.60B |

| Shareholders Equity | 363.56B | 336.15B | 314.80B | 292.29B | 271.88B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 68.79B | 60.64B | 35.61B | 27.78B | 33.65B |

| Operating Activities Other Non Cash Items | -82.12B | -85.01B | -57.49B | -53.39B | -3.86B |

| Operating Activities Other Assets Liabilities | -767.10M | N/A | N/A | 1.80B | -28.10M |

| Operating Activities Operating Cash Flow | -14.10B | -24.37B | -21.88B | -23.81B | 29.77B |

| Investing Activities Capital Expenditures | -732.50M | -366.50M | -405.40M | -348.60M | -108.20M |

| Investing Activities Purchase Of Investments | -9.82B | -884.30M | -7.86B | -22.03B | -5.57B |

| Investing Activities Sale Of Investments | 1.16B | 7.12B | 262.10M | 6.27B | 14.25B |

| Investing Activities Other Investing Activity | 2.40M | 3.50M | 2.70M | 4.90M | 4.30M |

| Investing Activities Investing Cash Flow | -9.39B | 5.87B | -8.00B | -16.11B | 8.58B |

| Financing Activities Long Term Debt Issuance | 1727.51B | 1464.20B | 1821.51B | 1523.14B | 1203.85B |

| Financing Activities Long Term Debt Payments | -1531.26B | -1369.53B | -1545.65B | -1362.44B | -1095.04B |

| Financing Activities Common Dividends | -4.95B | -4.68B | -4.62B | -4.68B | -4.04B |

| Financing Activities Other Financing Charges | -16.55B | -16.01B | -68.24B | -535.60M | 58.16B |

| Financing Activities Financing Cash Flow | 174.75B | 73.99B | 203.00B | 178.84B | 162.92B |

| End Cash Position | 12.89B | 14.23B | 6.41B | 8.22B | 13.32B |

| Free Cash Flow | -166.83B | -71.88B | -196.96B | -167.75B | -171.51B |

| Financing Activities Common Stock Issuance | N/A | 0.00 | 0.00 | 23.34B | 0.00 |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend shows a downward price action with the stock trading below its 200-day moving average at ₹569.03, indicating potential bearish momentum.

- Key support levels are near the 52-week low of ₹483.7, while resistance is observed around the 52-week high of ₹646.5 and the 50-day moving average at ₹525.72.

- The stock price is below both the 50-day and 200-day moving averages, suggesting a weakening trend in the medium to long term.

- Momentum indicators such as RSI and MACD are not explicitly provided, but the low beta of 0.18 suggests limited volatility and subdued momentum.

- Multi-timeframe analysis indicates consistent price weakness across daily and weekly charts, with no significant bullish reversal patterns identified.

- Current technical setup suggests a cautious market scenario with potential for further downside if support levels are breached, while a recovery would require overcoming resistance near moving averages.

Trending News

1. Headline: LIC Housing Finance Uploads Q3 FY26 Investor Presentation for Stakeholders

Summary: LIC Housing Finance Ltd has released and uploaded its Q3 FY26 investor presentation, providing stakeholders with updated financial and operational insights. This update reflects the company’s ongoing commitment to transparency and engagement with its shareholder base, highlighting recent performance metrics and strategic priorities.

Sentiment: Positive

2. Headline: Buy, Sell Or Hold: BSE, LIC Housing, Kaynes, Dixon Tech, IRCTC, Raymond, HAL — Ask Profit

Summary: A market commentary discusses the positioning of LIC Housing Finance Ltd. shares alongside other companies, analyzing current market prices and investor considerations. The report provides a neutral perspective on the stock’s status without explicit recommendations, reflecting mixed market sentiment.

Sentiment: Neutral

3. Headline: LIC Housing Finance Ltd Spurts 3.46% Gains for Third Straight Session

Summary: LIC Housing Finance Ltd experienced a 3.46% increase in share price for the third consecutive session, reaching approximately ₹520.6. This short-term price movement reflects positive trading momentum, though broader market factors continue to influence overall performance.

Sentiment: Negative

4. Headline: LIC Housing Finance Ltd Q3 2026 Earnings Call Highlights: Steady Revenue Growth

Summary: During the Q3 2026 earnings call, LIC Housing Finance Ltd reported steady revenue growth, underscoring consistent operational performance. The company highlighted key financial metrics and addressed market conditions impacting the housing finance sector.

Sentiment: Positive

5. Headline: Those Who Invested in LIC Housing Finance Three Years Ago Are Up 44%

Summary: An analysis reveals that shareholders who invested in LIC Housing Finance Ltd three years prior have realized a 44% return, outperforming average market returns. This performance metric highlights the stock’s historical value creation despite recent volatility.

Sentiment: Negative

Powered by Brave

Recent Updates

News Summary

Recent updates for LIC Housing Finance Ltd. include the release of the Q3 FY26 investor presentation, providing detailed insights into the company’s financial performance and strategic outlook. Market commentary has offered a balanced view on the stock’s current positioning, reflecting mixed sentiments. The company’s share price showed a short-term upward trend with gains over three consecutive sessions, signaling positive trading momentum. Earnings call highlights from Q3 2026 emphasize steady revenue growth amid prevailing market conditions. Additionally, historical analysis points to a 44% return for shareholders investing three years ago, underscoring the company’s capacity for value creation over time.

News Sentiment

Sentiment across recent news is mixed to moderately positive, with investor presentations and earnings reports contributing to constructive outlooks, while some market analyses and price movements suggest caution. Positive earnings and steady revenue growth support confidence in operational stability, whereas short-term price volatility and neutral market commentaries indicate ongoing uncertainty in the sector.

Analytical Overview

Analysis Summary

LIC Housing Finance Ltd.’s valuation metrics, including a trailing P/E of 5.09 and forward P/E of 4.91, are significantly lower than the industry average, suggesting a relatively undervalued position within the mortgage finance sector. The price-to-book ratio of 0.72 also indicates the stock trades below its book value, which may reflect market concerns or conservative valuation.

The company’s growth trajectory shows a slight decline in quarterly revenue growth (-2.3%) and earnings growth (-2.6%), but steady revenue generation of approximately ₹84.14 billion and a strong profit margin of 65.18% support operational stability. Cash flow trends reveal negative operating cash flow but positive levered free cash flow, indicating mixed cash generation dynamics.

Financial health is challenged by a high debt-to-equity ratio exceeding 7.2, reflecting significant leverage, which could impact risk profile despite a strong equity base. The company maintains a reasonable dividend payout ratio of 10% with a yield near 2%, supporting shareholder returns.

Sector-specific challenges include regulatory scrutiny and macroeconomic factors affecting housing demand in India, while opportunities arise from government housing initiatives and increasing home ownership aspirations. The company’s strong institutional ownership and backing by LIC provide strategic advantages in navigating these factors.

Consideration of India-specific market factors such as evolving regulatory frameworks, consumer credit trends, and economic growth prospects is essential in assessing LIC Housing Finance’s positioning and future outlook.

Investment Conclusion

Supporting Factors: Primary supporting factors include the company’s low valuation multiples relative to peers, steady profitability with high margins, and strong institutional ownership providing governance stability.

Risk Factors: Main risk factors to monitor are the elevated leverage levels, negative operating cash flow, and modest revenue growth trends amid sector uncertainties.

SWOT Analysis

Strengths

- The company benefits from strong brand recognition as a subsidiary of Life Insurance Corporation of India.

- High profit and operating margins demonstrate operational efficiency.

- Significant institutional ownership supports governance and strategic direction.

- Large market capitalization positions the company as a leading player in the mortgage finance sector.

Weaknesses

- Elevated debt-to-equity ratio indicates high financial leverage.

- Negative operating cash flow raises concerns about cash generation.

- Declining quarterly revenue and earnings growth suggest potential growth challenges.

- Price-to-cash-flow ratio is negative, reflecting cash flow inefficiencies.

Opportunities

- Government housing initiatives create demand for affordable financing solutions.

- Expanding home ownership in India offers market growth potential.

- Strong distribution network enables access to diverse customer segments.

- Potential to improve cash flow management and reduce leverage.

Threats

- Regulatory changes in the housing finance sector could impact operations.

- Macroeconomic volatility may affect housing demand and credit quality.

- Competitive pressures from other housing finance companies.

- Interest rate fluctuations could influence borrowing costs and profitability.

Company Description

LIC Housing Finance Ltd. is a prominent player in the housing finance sector in India. It primarily focuses on providing long-term financial assistance to individuals for purchasing or constructing residences, as well as for renovation or extension of existing homes. The company engages across a broad spectrum of clients, including retail customers, builders, and other corporate entities, thereby underpinning the real estate sector's growth. LIC Housing Finance's operations are integral to enhancing home ownership rates in India by bridging the financial gap for prospective homeowners. As a subsidiary of Life Insurance Corporation of India, it benefits from a robust financial backing, extensive distribution network, and a well-established brand trust. The company plays a critical role in the financial market by enabling access to home financing solutions, which contribute to overall economic development. It caters not only to individual housing needs but also supports government initiatives aimed at housing for all by providing affordable financing solutions.