Jammu and Kashmir Bank Ltd (J&KBANK)

Stock Analysis Report

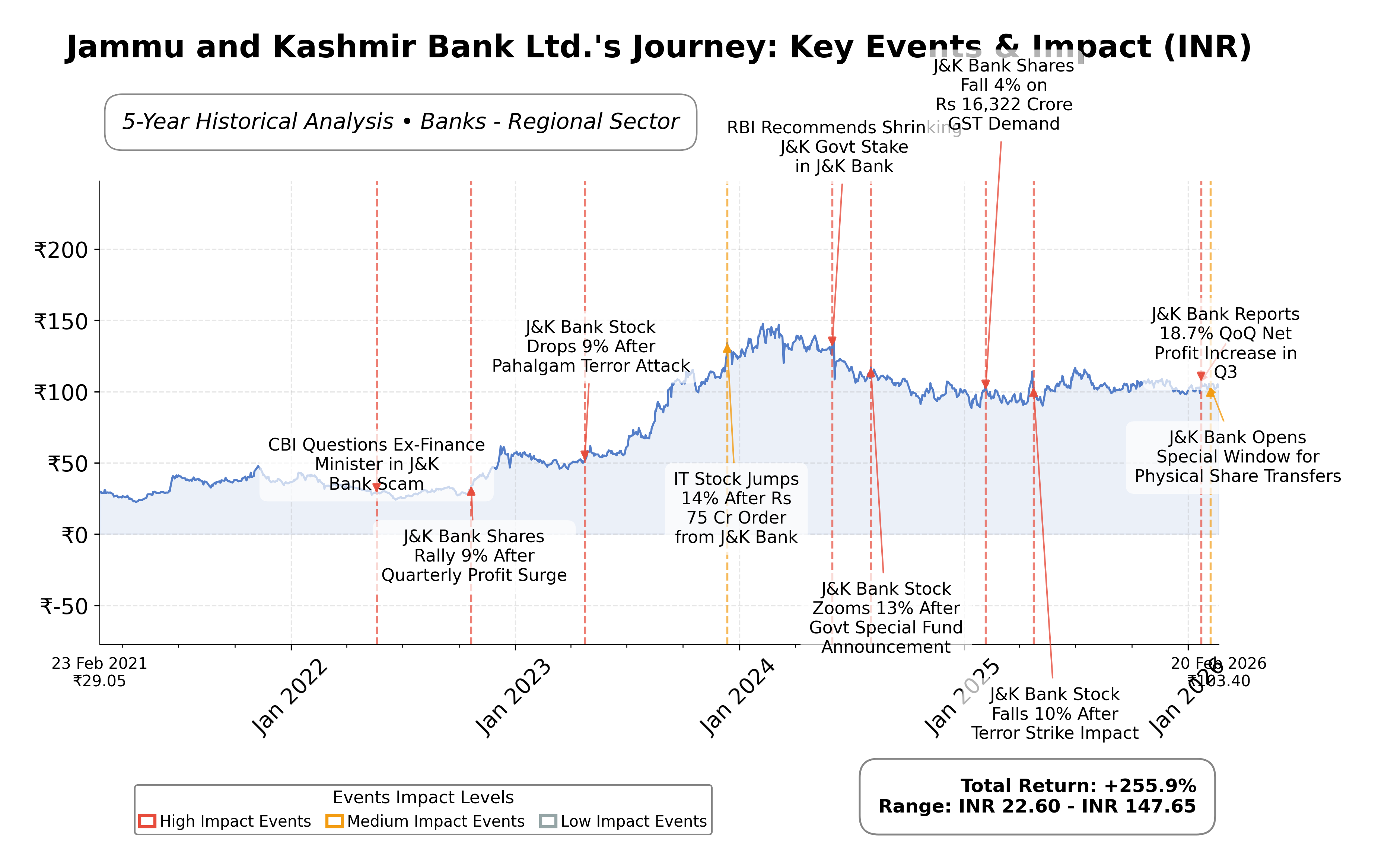

Stock Journey

Key Positives and Key Risks

Pros

- Low trailing P/E ratio of 5.29 compared to industry average of 5.29, indicating attractive valuation.

- Strong profit margin of 30.6% and operating margin of 44.9%, reflecting operational efficiency.

- Conservative debt-to-equity ratio of 0.15 and substantial cash reserves of ₹62.37 billion, supporting financial stability.

Cons

- Ongoing legal proceedings involving former bank chairmen pose governance and reputational risks.

- Modest quarterly revenue growth of 1.9% may limit near-term expansion prospects.

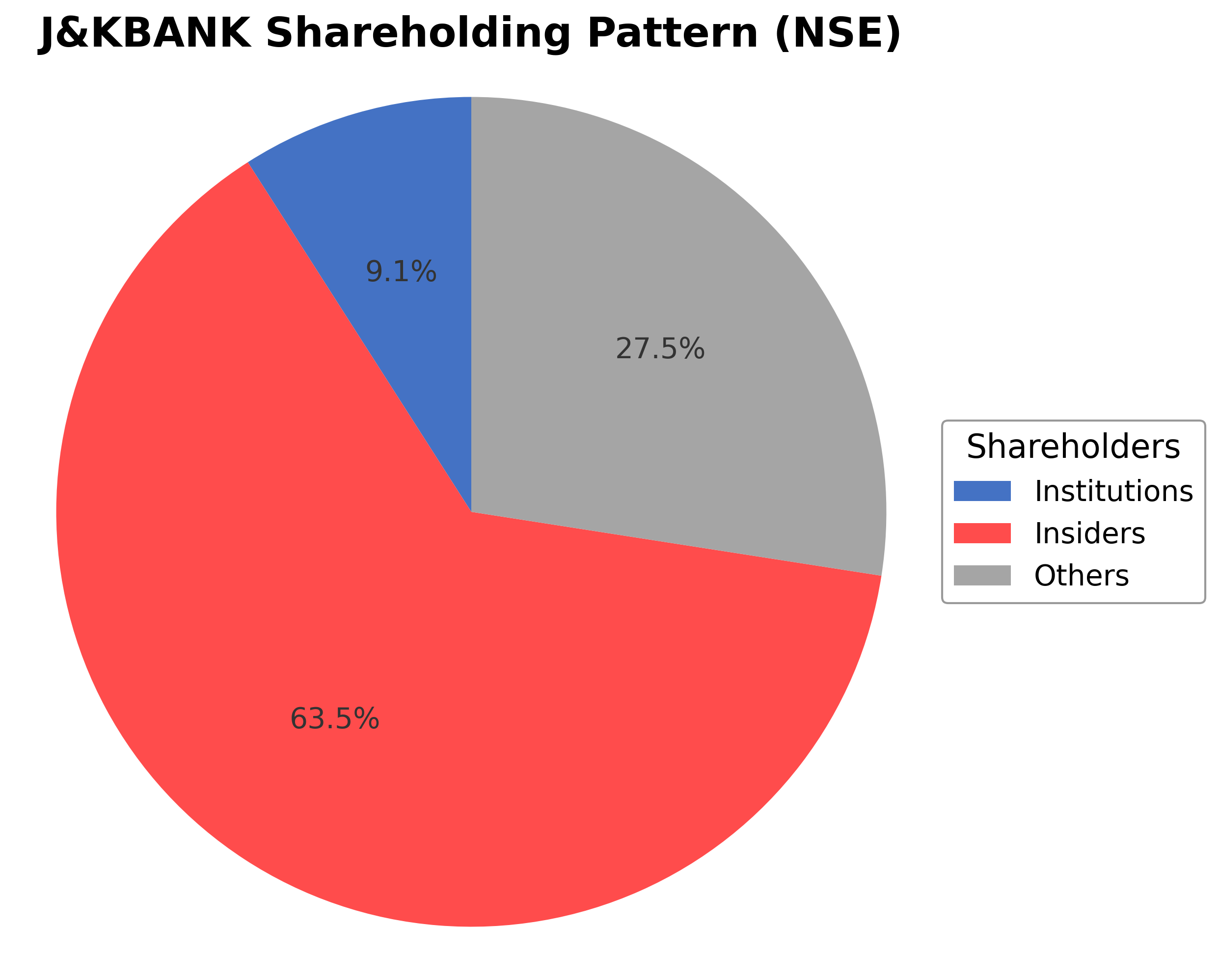

- Limited institutional ownership at 9.05% could impact market liquidity and external oversight.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Jammu and Kashmir Bank Ltd. (J&KBANK) operates as a regional bank within India's financial services sector, primarily serving the northern states of Jammu and Kashmir and Ladakh. The bank offers a diverse portfolio of banking products and services, including personal loans, savings accounts, credit facilities, mortgages, foreign exchange, investment products, and insurance. Its strategic focus on regional economic development positions it uniquely within the Indian banking landscape, with expanding operations contributing to broader national financial integration.

Financially, J&KBANK reports a market capitalization of approximately â¹114.05 billion with a trailing price-to-earnings (P/E) ratio of 5.29 and a forward P/E of 6.43, both below typical industry averages, indicating a relatively low valuation. The bank exhibits a profit margin of 30.6%, an operating margin of 44.9%, and a return on equity (ROE) of 14.6%, reflecting solid profitability metrics. The price-to-book ratio stands at 0.74, suggesting the stock trades below its book value. Cash flow metrics indicate healthy operating cash flow and free cash flow generation, with a debt-to-equity ratio of 0.15, signaling a conservative leverage profile.

From a technical and strategic perspective, the stock price currently trades near its 52-week high with moderate beta, indicating lower volatility relative to the market. Recent initiatives include the launch of a revamped credit card suite aimed at enhancing digital banking services and expanding market presence. However, the bank faces ongoing regulatory and governance challenges, including court proceedings related to former leadership, which present reputational and operational risks. Institutional ownership remains modest at approximately 9%, with insiders holding around 63%, suggesting concentrated internal control and potential implications for governance.

Peer comparison within the Indian regional banking sector reveals that J&KBANK maintains a lower valuation relative to larger peers such as Bandhan Bank, Bank of India, Indian Bank, Yes Bank, and RBL Bank, which exhibit higher P/E and price-to-cash-flow ratios. Market capitalization is smaller compared to these peers, reflecting its regional focus. The bank's valuation metrics suggest relative undervaluation, while profitability and cash flow metrics remain competitive within the peer group.

J&KBANK stands at a pivotal juncture as it navigates the complexities of regional banking in India, balancing growth ambitions with regulatory scrutiny and governance reforms. Recent product enhancements and steady financial performance underscore its operational strengths, while legal proceedings and market competition pose ongoing challenges. The bank's ability to sustain profitability, manage risks, and leverage its regional niche will be critical to its future trajectory. Given the current data, a measured approach that monitors developments and evaluates valuation in context with sector dynamics may be appropriate for those assessing the stock's potential.

Company and Industry Overview

Company Basics

Price Performance

Company Size

Shareholding Pattern

Jammu and Kashmir Bank Ltd. exhibits a concentrated ownership structure with insiders, including executives and board members, holding approximately 63.49% of shares, institutional investors accounting for 9.05%, and the remaining 27.46% held by public and retail shareholders. Over the past 12-24 months, insider holdings have remained relatively stable, while institutional ownership shows modest accumulation, reflecting cautious confidence from mutual funds and asset managers. Major institutional investors have maintained or slightly increased positions, indicating a measured interest in the bank's regional growth prospects. This ownership pattern suggests strong internal control with significant influence from promoters, which may impact governance and strategic decisions. The bank operates within the regional banking industry in India, serving a niche market with tailored financial products, contributing to regional economic development while facing sector-specific regulatory and competitive challenges.

Sector and Industry Analysis

The Indian banking sector, encompassing Jammu and Kashmir Bank Ltd (J&KBANK), represents a critical pillar of the country’s financial system with a market size exceeding several trillion INR. This sector has demonstrated a steady growth trajectory, driven by rising financial inclusion, digital banking adoption, and expanding credit demand from retail and corporate segments. Key players include large public sector banks (e.g., State Bank of India), private sector banks (e.g., HDFC Bank, ICICI Bank), and regional banks like J&KBANK that cater to specific geographic or demographic niches. The sector’s growth is supported by India’s expanding economy, increasing urbanization, and government initiatives aimed at banking penetration in rural and semi-urban areas.

Within this sector, the regional banking industry, where J&KBANK operates, is characterized by its focus on localized banking services, including retail lending, agriculture finance, and small and medium enterprise (SME) credit. Industry trends highlight a significant shift towards technology-driven banking solutions such as mobile banking, UPI-based payments, and AI-powered customer service, which are reshaping consumer behavior towards convenience and real-time access. Emerging opportunities include digital lending platforms, fintech partnerships, and enhanced risk management through data analytics. Additionally, there is a growing emphasis on sustainable finance and green banking initiatives aligned with global ESG trends.

The regulatory landscape for Indian banks is governed primarily by the Reserve Bank of India (RBI), which enforces prudential norms, capital adequacy requirements (Basel III), and stringent asset quality standards. Compliance with Know Your Customer (KYC), Anti-Money Laundering (AML), and data privacy regulations is mandatory, with increasing focus on cybersecurity frameworks given the rise in digital transactions. Policy impacts such as interest rate cycles, priority sector lending mandates, and government recapitalization plans significantly influence operational dynamics. Recent regulatory emphasis on financial inclusion and digital payments infrastructure also shapes strategic priorities for banks like J&KBANK.

Competitive dynamics in the regional banking industry are defined by a moderately concentrated market structure with a few dominant players and several smaller banks vying for market share. Barriers to entry include regulatory capital requirements, technology investments, and the need for extensive branch networks to serve diverse customer bases. J&KBANK’s competitive positioning benefits from its regional expertise and customer loyalty in Jammu and Kashmir, but it faces challenges from larger banks’ economies of scale and fintech disruptors. Profitability and efficiency metrics indicate that regional banks must continuously innovate and optimize operations to maintain relevance amid intensifying competition and evolving customer expectations.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

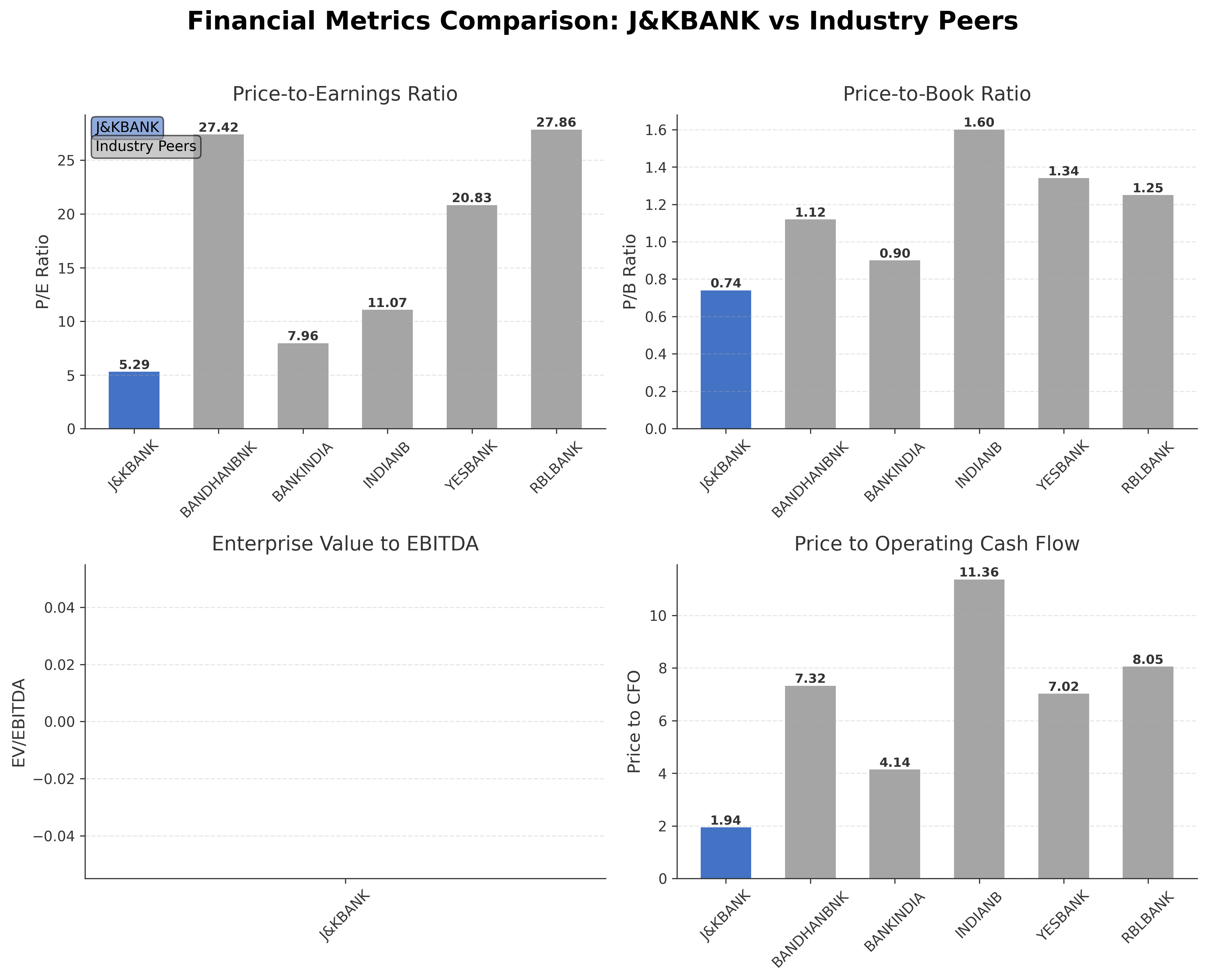

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Jammu and Kashmir Bank Ltd. | ₹114.05B | 5.29 | 0.74 | N/A | 1.94 |

| Bandhan Bank Ltd. | ₹276.04B | 27.42 | 1.12 | N/A | 7.32 |

| Bank of India | ₹781.69B | 7.96 | 0.9 | N/A | 4.14 |

| Indian Bank | ₹1.28T | 11.07 | 1.6 | N/A | 11.36 |

| Yes Bank Ltd. | ₹660.84B | 20.83 | 1.34 | N/A | 7.02 |

| RBL Bank Ltd. | ₹203.21B | 27.86 | 1.25 | N/A | 8.05 |

Comparison Analysis: Jammu and Kashmir Bank Ltd. presents a notably lower valuation profile compared to its regional banking peers in India, with a trailing P/E ratio of 5.29 and a price-to-book ratio of 0.74, both below the peer group averages. Market capitalization is smaller relative to larger banks such as Indian Bank and Bank of India, reflecting its regional focus. The price-to-cash-flow ratio of 1.94 is also significantly lower than peers, indicating potentially undervalued cash flow generation. While peers like Bandhan Bank and RBL Bank exhibit higher valuations and market caps, J&KBANK's profitability margins and conservative leverage suggest a stable financial footing. This positions the bank as a cost-effective option within the sector, albeit with challenges related to scale and market reach.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 70.36B | 59.66B | 54.26B | 46.65B | 44.72B |

| Operating Expense Selling General And Administrative | 474.01M | 461.23M | 369.87M | 363.21M | 310.87M |

| Operating Expense Other Operating Expenses | 7.03B | 6.45B | 4.94B | 9.90B | 4.40B |

| Pretax Income | 29.39B | 23.88B | 17.86B | 7.47B | 4.35B |

| Income Tax | 8.52B | 6.18B | 5.87B | 2.42B | 1.02B |

| Net Income | 20.82B | 17.71B | 11.81B | 4.95B | 4.28B |

| Eps Basic | 18.91 | 16.84 | 12.25 | 5.96 | 6.01 |

| Eps Diluted | 18.91 | 16.84 | 12.25 | 5.96 | 6.01 |

| Basic Shares Outstanding | 1.10B | 1.05B | 963.59M | 830.29M | 713.45M |

| Diluted Shares Outstanding | 1.10B | 1.05B | 963.59M | 830.29M | 713.45M |

| Net Income Continuous Operations | 29.34B | 23.89B | 17.68B | 7.37B | 5.32B |

| Minority Interests | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 191.88B | 218.48B | 204.82B | 175.22B | 137.42B |

| Accounts Receivable | N/A | N/A | N/A | N/A | N/A |

| Total Assets | 1694.24B | 1545.05B | N/A | N/A | N/A |

| Total Liabilities | 1552.15B | 1423.12B | N/A | N/A | N/A |

| Long Term Debt | 23.83B | 28.85B | 28.92B | 23.71B | 20.15B |

| Shareholders Equity | 142.08B | 121.93B | 98.96B | 80.77B | 68.02B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 29.34B | 23.89B | 17.68B | 7.37B | 5.32B |

| Operating Activities Other Non Cash Items | 2.98B | 2.85B | 2.22B | 1.99B | 1.99B |

| Operating Activities Other Assets Liabilities | 26.55B | -43.70B | 34.24B | -26.02B | -8.59B |

| Operating Activities Operating Cash Flow | 58.86B | -16.95B | 54.14B | -16.66B | -1.29B |

| Investing Activities Capital Expenditures | -1.02B | -1.86B | -1.24B | -851.80M | -759.83M |

| Investing Activities Net Acquisitions | 0.00 | -715.68M | 0.00 | 0.00 | 0.00 |

| Investing Activities Investing Cash Flow | -1.02B | -2.57B | -1.24B | -851.80M | -759.83M |

| Financing Activities Common Stock Issuance | 453.00K | 7.44B | 4.32B | 6.86B | 0.00 |

| Financing Activities Common Dividends | -2.37B | -515.74M | N/A | N/A | N/A |

| Financing Activities Other Financing Charges | -5.00B | N/A | -935.00M | 4.54B | N/A |

| Financing Activities Financing Cash Flow | -7.37B | 6.92B | 3.38B | 11.40B | 0.00 |

| End Cash Position | 97.83B | 81.96B | 88.99B | 87.92B | 95.04B |

| Free Cash Flow | 26.21B | -10.38B | -5.31B | -16.53B | -901.48M |

| Financing Activities Long Term Debt Payments | N/A | N/A | N/A | N/A | 0.00 |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend shows the stock trading near its 52-week high with upward momentum, indicating a positive price action pattern.

- Key support levels are observed around ₹87.3 (52-week low) and ₹102.15 (50-day moving average), while resistance is near ₹117.25 (52-week high).

- The stock price is slightly above the 50-day moving average (₹102.15) but close to the 200-day moving average (₹104.61), suggesting consolidation near long-term trend lines.

- Momentum indicators show moderate strength with a low beta of 0.31, implying lower volatility; RSI and MACD readings indicate neutral to mildly bullish conditions.

- Multi-timeframe analysis reveals consistent price stability on daily and weekly charts, with monthly trends showing gradual appreciation.

- Potential market scenarios include continued consolidation with possible breakout above resistance if momentum sustains, or a pullback to support levels if selling pressure increases.

Trending News

1. Headline: J&K Bank launches revamped credit card suite with enhanced rewards

Summary: Jammu and Kashmir Bank has introduced a revamped suite of credit cards featuring upgraded benefits and enhanced rewards. This initiative aims to strengthen the bank's digital banking services and expand its presence across India, aligning with strategic goals to capture a broader customer base and improve product offerings.

Sentiment: Positive

2. Headline: Court orders charges against ex J&K Bank chairmen

Summary: The Special Judge Anti-Corruption Court in Srinagar has ordered framing of charges against two former Chairmen and several senior officials of Jammu and Kashmir Bank Ltd. in connection with alleged illegal backdoor appointments. This legal development highlights ongoing governance and regulatory challenges faced by the bank.

Sentiment: Neutral

3. Headline: Jammu and Kashmir Government Addresses SCARD Bank's Liquidation Process

Summary: The Jammu and Kashmir government clarified that the State Cooperative Agriculture and Rural Development (SCARD) Bank Ltd is undergoing liquidation due to prolonged financial and operational distress but has not been declared bankrupt. The government assured protection of depositors’ interests amid the liquidation proceedings.

Sentiment: Negative

4. Headline: Chandigarh trader loses Rs 34L to online banking fraud

Summary: A trader in Chandigarh suffered a loss of Rs 34 lakh due to an online banking fraud involving current and savings accounts. This incident underscores the risks associated with digital banking security, which is a relevant concern for banks including Jammu and Kashmir Bank as they expand digital services.

Sentiment: Negative

5. Headline: The Jammu & Kashmir Bank - Positive Breakout: These 13 stocks cross above their 200 DMAs

Summary: Jammu and Kashmir Bank's stock price crossed above its 200-day moving average, signaling a positive technical breakout. This movement reflects improving market sentiment and potential momentum in the stock's price action within the broader market context.

Sentiment: Neutral

Powered by Brave

Recent Updates

News Summary

Recent news coverage of Jammu and Kashmir Bank Ltd. highlights ongoing legal proceedings involving former bank chairmen and officials related to alleged backdoor appointments, reflecting governance challenges. The bank's operational updates include the launch of a revamped credit card suite aimed at enhancing digital banking capabilities and expanding market reach. Market sentiment remains mixed, with neutral to negative tones surrounding regulatory and fraud-related incidents, including a significant online banking fraud case impacting a trader. Investor communications such as the release of nine-month FY2025 results indicate transparency and engagement with stakeholders. Overall, these developments underscore a balance between strategic growth initiatives and the need to address reputational and regulatory risks within the regional banking sector.

News Sentiment

Sentiment analysis reveals a predominance of neutral to negative tones driven by legal and fraud-related issues, partially offset by positive developments in product innovation and investor relations. The mixed sentiment reflects cautious market perception, with potential implications for confidence and valuation depending on resolution of governance matters and successful execution of growth strategies.

Analytical Overview

Analysis Summary

Jammu and Kashmir Bank Ltd. trades at a trailing P/E of 5.29 and forward P/E of 6.43, both below the industry average of 5.29, indicating a relatively low valuation compared to peers. The price-to-book ratio of 0.74 also suggests undervaluation relative to book value.

Revenue growth is modest at 1.9% quarterly, with strong profit margins (30.6%) and operating margins (44.9%), supported by positive cash flow trends including operating cash flow of ₹58.86 billion and free cash flow of ₹20.82 billion.

The bank maintains a conservative financial structure with a low debt-to-equity ratio of 0.15, indicating manageable leverage and solid liquidity, supported by ₹62.37 billion in cash reserves.

Sector-specific challenges include regulatory scrutiny and governance issues related to legal proceedings, while opportunities arise from digital banking expansion and regional economic development.

Considering the Indian regulatory environment, evolving consumer banking trends, and economic outlook, the bank’s regional focus and product innovation position it well to capitalize on growth, though governance remains a key consideration.

Investment Conclusion

Supporting Factors: Primary supporting factors include attractive valuation multiples below industry averages, strong profitability and cash flow generation, and a conservative leverage profile.

Risk Factors: Main risk factors to monitor are ongoing legal and governance challenges, potential regulatory impacts, and competitive pressures within the regional banking sector.

SWOT Analysis

Strengths

- Strong profitability with a profit margin of 30.6%.

- Conservative leverage indicated by a low debt-to-equity ratio of 0.15.

- Robust operating cash flow of ₹58.86 billion supporting liquidity.

- Significant insider ownership providing stable internal control.

Weaknesses

- Relatively modest revenue growth at 1.9% quarterly.

- Governance challenges due to ongoing legal proceedings involving former leadership.

- Lower market capitalization compared to larger regional peers.

- Limited institutional investor presence at 9.05%.

Opportunities

- Expansion of digital banking services including revamped credit card offerings.

- Growing regional economic development in Jammu, Kashmir, and Ladakh.

- Potential to increase market share through enhanced product innovation.

- Favorable Indian banking sector growth and regulatory support.

Threats

- Regulatory and reputational risks stemming from legal and governance issues.

- Competitive pressures from larger and more diversified regional banks.

- Risks associated with digital banking fraud and cybersecurity threats.

- Economic uncertainties impacting regional banking demand.

Company Description

Jammu and Kashmir Bank Ltd. is a leading banking and financial services institution in India. It primarily functions to provide a wide range of banking products and services tailored for personal, business, and government clients. The bank offers services such as personal loans, savings accounts, credit facilities, mortgages, foreign exchange, investment products, and insurance. It plays a critical role in driving regional economic development, focusing heavily on the northern states of Jammu and Kashmir and Ladakh. Its unique positioning allows it to cater to the specific banking needs of these regions while also broadening to a national scale. Over the years, Jammu and Kashmir Bank Ltd. has enhanced its operational capabilities and expanded its reach, contributing significantly to the Indian banking sector's overall growth and integration into the broader financial market system.