Hindustan Copper Ltd (HINDCOPPER)

Stock Analysis Report

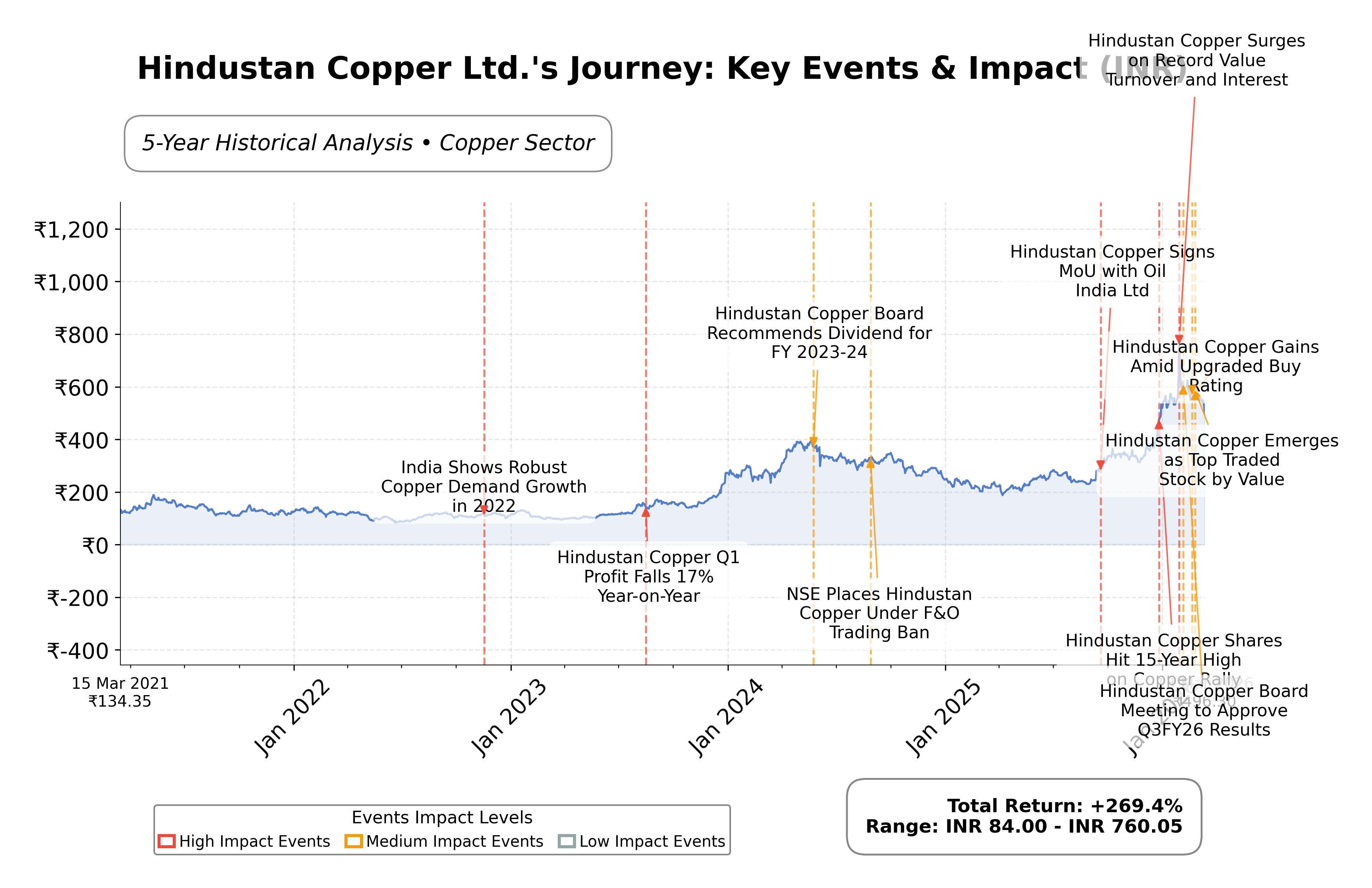

Stock Journey

Key Positives and Key Risks

Pros

- Revenue growth of 9.7% quarterly indicates strong top-line expansion supporting business momentum.

- Profit margin of 24.93% and return on equity of 17.48% reflect operational efficiency and profitability.

- Operating cash flow of ₹5.63 billion and free cash flow of ₹4.65 billion demonstrate solid cash generation capacity.

Cons

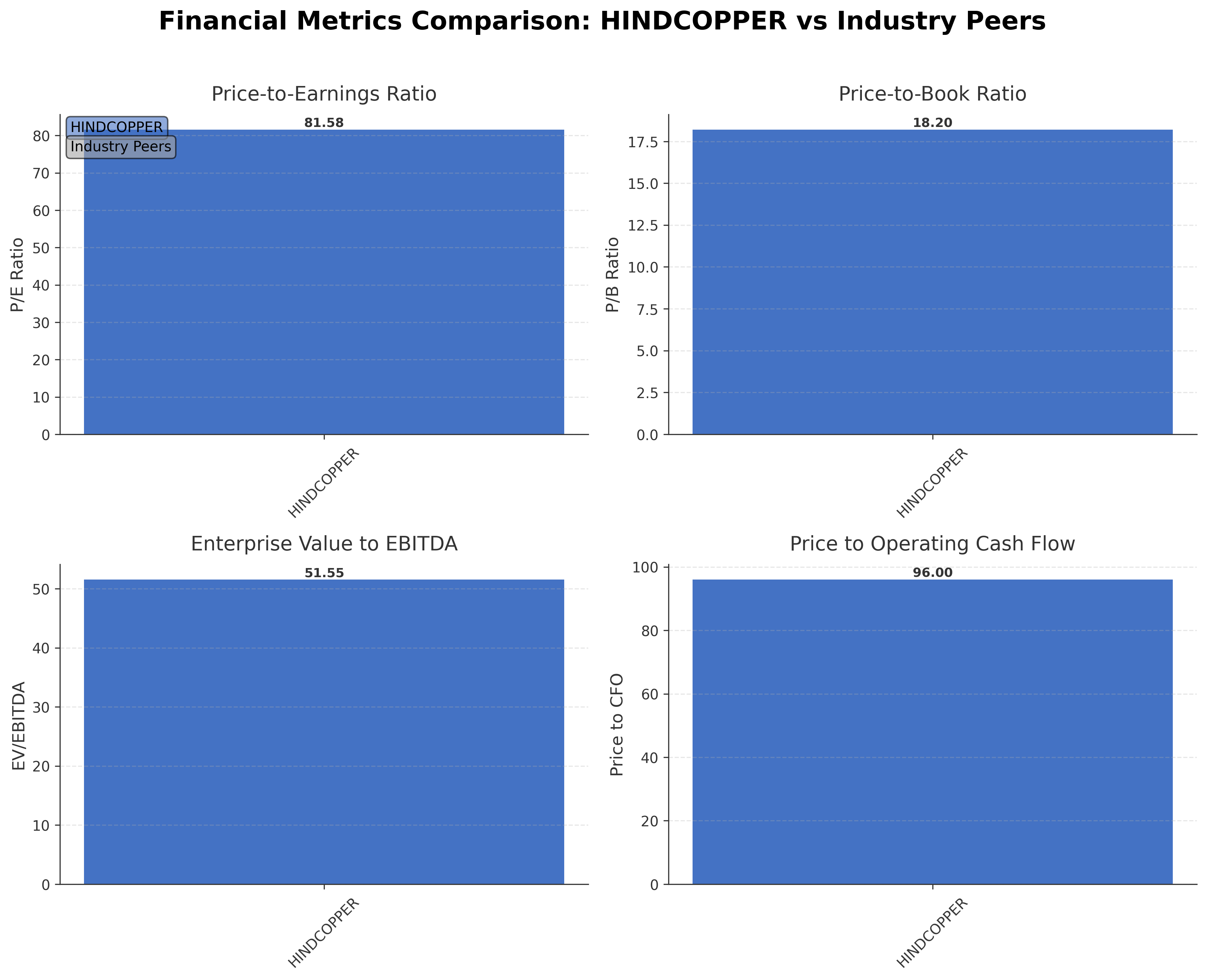

- Trailing P/E ratio of 81.58 and price-to-book ratio of 18.20 suggest elevated valuation levels relative to earnings and equity.

- Total debt to equity ratio of 4.78 indicates significant leverage, posing financial risk.

- Downside risk of 53.68% from 52-week high to current price highlights potential price volatility.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Hindustan Copper Ltd. (HINDCOPPER) is a government-owned enterprise operating in the copper mining, smelting, and refining industry in India. The company is a central public sector undertaking focused on harnessing domestic copper resources and producing a wide range of copper products, including cathodes and wire rods. Positioned as a key player in India's basic materials sector, Hindustan Copper supports critical industries such as transportation, electrical, construction, and telecommunications by supplying essential copper products.

Financially, the company exhibits a market capitalization of approximately â¹540.39 billion with a trailing P/E ratio of 81.58 and a forward P/E of 26.83, indicating a significant valuation premium relative to earnings. The price-to-book ratio stands at 18.20, and the enterprise value to EBITDA is notably high at 51.55. Revenue growth is positive with a quarterly increase of 9.7%, and profitability metrics such as a 24.93% profit margin and a return on equity of 17.48% reflect operational efficiency. Cash flow generation remains robust with operating cash flow of â¹5.63 billion and free cash flow of â¹4.65 billion.

On the strategic front, recent leadership changes include the appointment of Shri Anupam Misra as CMD, bringing extensive experience in marketing and international trade. The company has also secured regulatory approvals safeguarding its mining operations in Jharkhand. Technical indicators reveal a stock price currently trading above the 200-day moving average but below the 50-day average, with momentum oscillators showing mixed signals. Key risks include commodity price volatility and geopolitical tensions impacting input costs, while strengths lie in government backing and integrated operations.

Peer analysis is limited due to the absence of listed comparable companies in the same industry and region within the provided data. However, Hindustan Copperâs valuation multiples are relatively elevated compared to typical industry benchmarks, suggesting a premium positioning. The companyâs dominant domestic presence and government ownership distinguish it from potential regional competitors.

Hindustan Copper navigates a complex industry landscape marked by fluctuating commodity prices, regulatory scrutiny, and evolving market demand. Recent achievements such as strong revenue growth, leadership renewal, and operational safeguards position the company for continued relevance. Challenges remain in managing cost pressures and sustaining profitability amid market volatility. The stakes involve balancing growth ambitions with operational resilience. Given the current financial and strategic profile, maintaining a watchful stance may be appropriate for those assessing the stock, considering both the companyâs strengths and the inherent risks in the copper sector.

Company and Industry Overview

Company Basics

Price Performance

Company Size

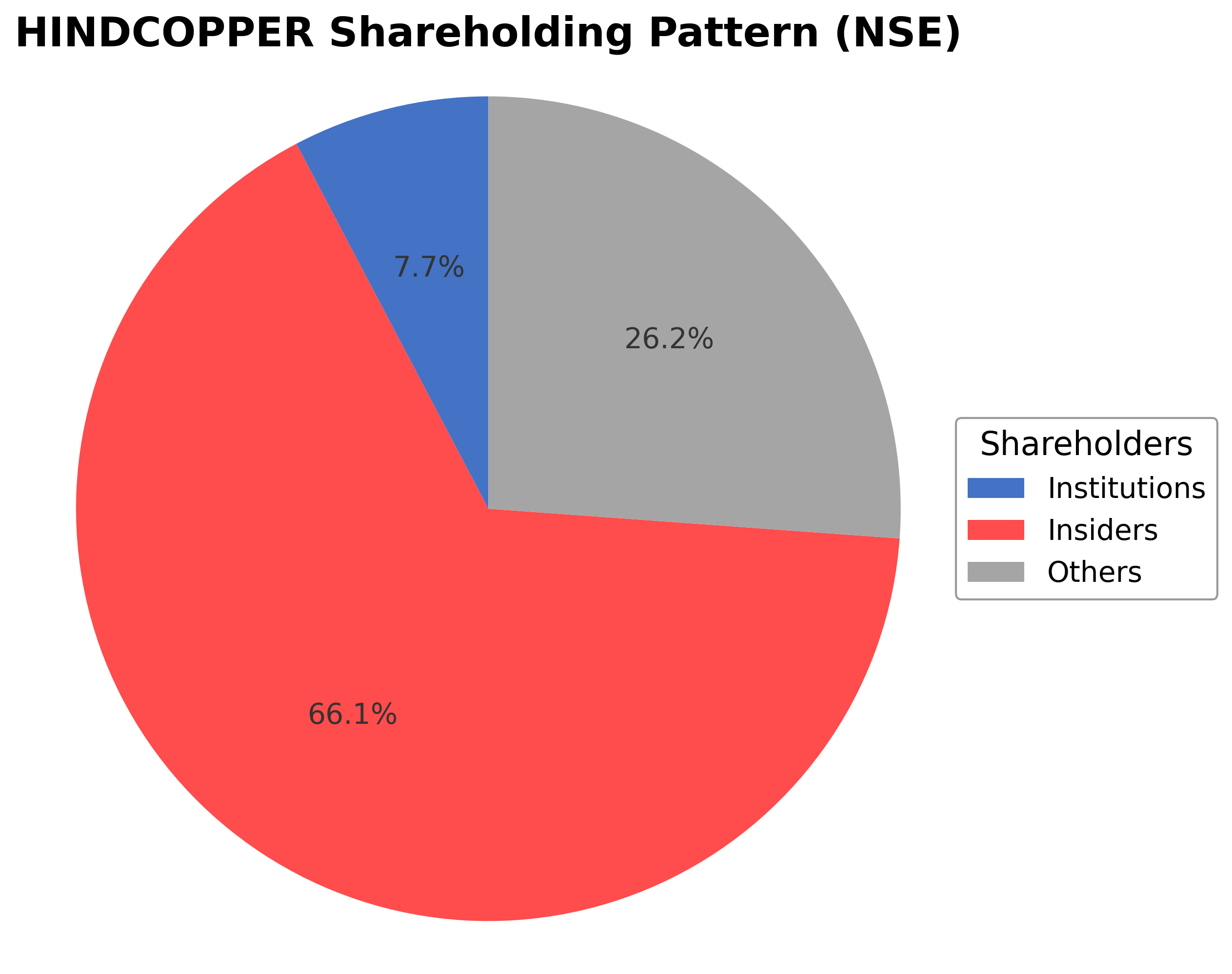

Shareholding Pattern

Hindustan Copper Ltd.'s ownership structure is predominantly held by insiders, including executives and government-affiliated entities, accounting for approximately 66.14% of shares. Institutional investors such as mutual funds and pension funds hold around 7.71%, while the remaining 26.15% is held by public shareholders including retail investors and employee stock plans. Over the past 12-24 months, there have been no significant shifts in promoter holdings, while institutional ownership has remained relatively stable with minor fluctuations. This shareholding pattern reflects a strong government influence and stable institutional interest, suggesting a governance framework aligned with public sector objectives and strategic national interests. The ownership distribution supports continuity in corporate strategy and may influence future decisions on capital allocation and operational priorities.

Sector and Industry Analysis

Hindustan Copper Ltd. operates within the broader metals and mining sector, specifically focusing on copper production—a critical industrial metal with extensive applications in electrical, construction, and manufacturing industries. The Indian copper sector is relatively modest in global terms but strategically important due to copper’s role in infrastructure development and the ongoing energy transition. Hindustan Copper is unique as India’s only vertically integrated copper producer, controlling the entire value chain from mining to refined copper products. The sector has witnessed steady growth driven by rising domestic demand, government infrastructure initiatives, and increasing electrification, with India’s copper consumption projected to grow at a CAGR of approximately 6-8% over the medium term. Globally, copper demand is buoyed by trends in renewable energy, electric vehicles (EVs), and smart grids, which also influence the Indian market dynamics.

Industry trends in copper mining and processing are increasingly shaped by technological advancements aimed at improving ore beneficiation, smelting efficiency, and environmental sustainability. Automation and digitalization in mining operations are gaining traction to enhance productivity and reduce operational costs. Additionally, the push for green mining practices and circular economy principles, including recycling copper scrap, is becoming more prominent. Consumer behavior is indirectly influencing the industry through the demand for cleaner energy and EVs, which require substantial copper inputs. Emerging opportunities include expansion into value-added copper products and leveraging India’s mineral resource base to reduce import dependency. The integration of advanced analytics and IoT in mining operations also presents avenues for operational optimization.

The regulatory landscape governing the copper mining sector in India is complex, involving multiple layers of compliance related to mining leases, environmental clearances, labor laws, and export-import policies. The Mines and Minerals (Development and Regulation) Act, 1957, along with amendments, governs mining leases and operations. Environmental regulations have become more stringent, requiring companies to adopt sustainable mining practices and ensure rehabilitation of mining sites. The government’s focus on self-reliance (Atmanirbhar Bharat) and strategic mineral development has led to policy support for domestic mining companies, including Hindustan Copper, to expand capacity and modernize operations. However, regulatory delays and land acquisition challenges remain persistent issues impacting project timelines and capital expenditure.

Competitive dynamics in the Indian copper industry are characterized by Hindustan Copper’s dominant position as the sole integrated domestic producer, with a near-monopoly on operating copper ore mining leases in India. This unique positioning provides significant barriers to entry for new players, given the capital-intensive nature of mining, regulatory hurdles, and the need for integrated processing infrastructure. The competitive landscape is further influenced by imports of refined copper and copper products, primarily from global producers, which compete on price and quality. Hindustan Copper’s strategic advantage lies in its control over domestic ore resources and integrated operations, enabling cost efficiencies and supply security. Nonetheless, the company faces indirect competition from alternative materials and global commodity price volatility, which affect margins and investment decisions. Overall, the sector exhibits moderate competition with high entry barriers, underscoring the importance of operational excellence and regulatory navigation for sustained competitiveness.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

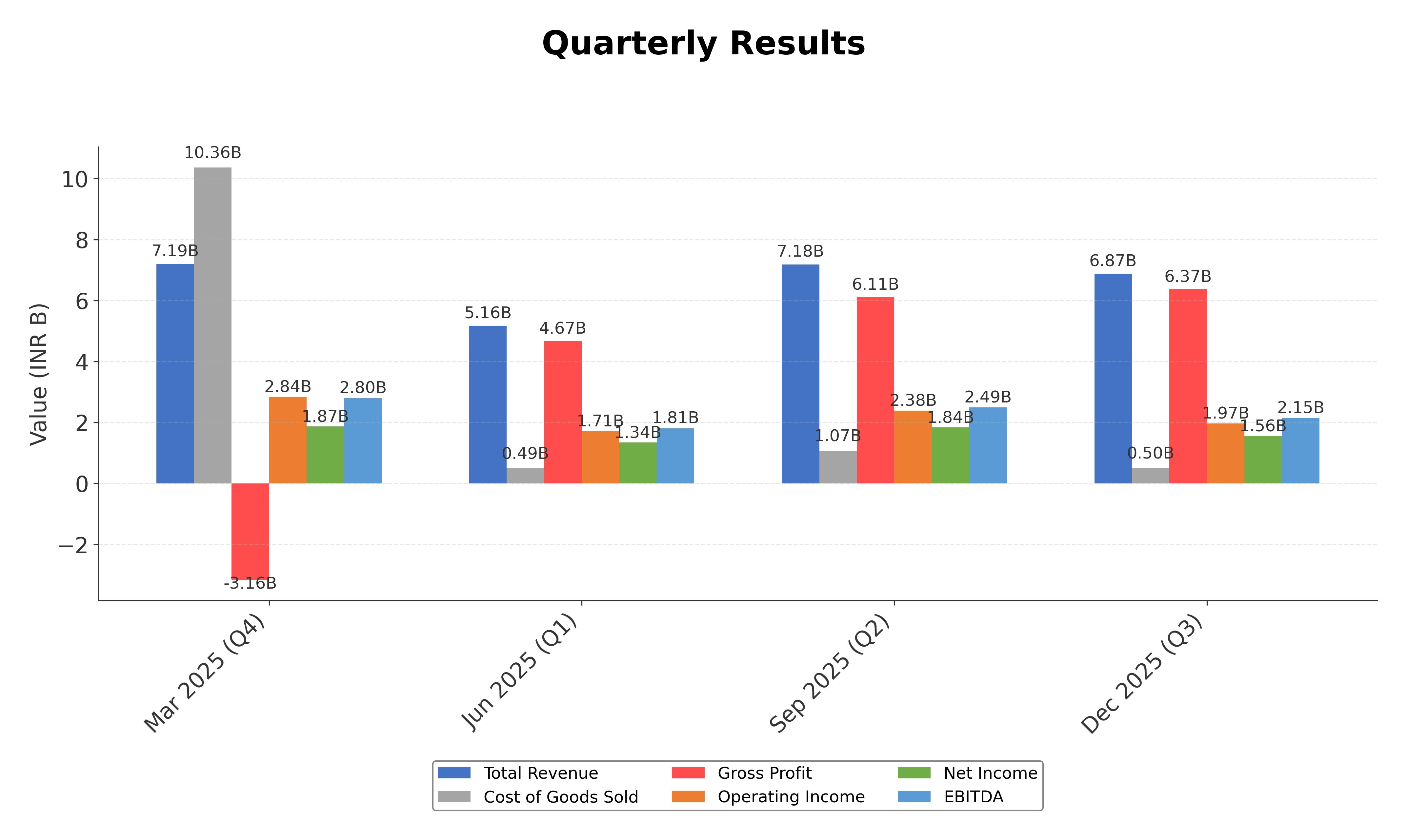

Financials

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Hindustan Copper Ltd. | ₹540.39B | 81.58 | 18.20 | 51.55 | 96.00 |

Comparison Analysis: Hindustan Copper Ltd. stands as a unique entity within the Indian copper industry due to its government ownership and integrated operations. The absence of listed direct peers in the same geographic region limits direct comparative analysis. However, the company's valuation multiples such as P/E and EV/EBITDA are relatively high, reflecting market expectations of growth or premium positioning. Return on equity is moderate at 17.48%, indicating reasonable profitability. The high price to cash flow ratio suggests elevated market valuation relative to operating cash generation. Overall, Hindustan Copper's metrics highlight its distinct market role and valuation profile within the regional copper sector.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 20.59B | 17.05B | 16.65B | 18.13B | 17.62B |

| Cost Of Goods | 10.16B | 9.26B | 8.98B | 9.06B | 10.72B |

| Gross Profit | 10.42B | 7.78B | 7.67B | 9.08B | 6.90B |

| Operating Expense Selling General And Administrative | 655.40M | 463.23M | 721.08M | 321.80M | 329.47M |

| Operating Expense Other Operating Expenses | 390.64M | 801.73M | 410.82M | 770.91M | 2.83B |

| Operating Income | 6.31B | 3.94B | 3.58B | 4.31B | 1.18B |

| Non Operating Interest Income | 111.15M | 248.83M | 217.10M | 177.89M | 38.39M |

| Non Operating Interest Expense | 20.97M | 88.80M | 75.33M | 54.11M | 147.17M |

| Pretax Income | 6.32B | 4.11B | 3.96B | 3.82B | 874.55M |

| Income Tax | 1.65B | 1.15B | 1.00B | 80.30M | -229.86M |

| Net Income | 4.65B | 2.95B | 2.95B | 3.74B | 1.10B |

| Eps Basic | 4.81 | 3.05 | 3.06 | 3.87 | 1.19 |

| Eps Diluted | 4.81 | 3.05 | 3.06 | 3.87 | 1.19 |

| Basic Shares Outstanding | 967.02M | 967.02M | 967.02M | 967.02M | 925.22M |

| Diluted Shares Outstanding | 967.02M | 967.02M | 967.02M | 967.02M | 925.22M |

| Ebit | 6.34B | 4.20B | 4.03B | 3.88B | 1.02B |

| Ebitda | 8.34B | 6.10B | 5.66B | 5.98B | 4.87B |

| Net Income Continuous Operations | 6.32B | 4.11B | 3.96B | 3.82B | 874.55M |

| Minority Interests | 131.00K | 0.00 | 354.00K | 271.00K | 381.00K |

| Preferred Stock Dividends | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 175.23M | 716.26M | 155.60M | 2.59B | 85.79M |

| Accounts Receivable | 1.71B | 1.37B | 661.46M | 801.00M | 1.68B |

| Total Assets | 35.01B | 32.70B | 29.85B | 29.55B | 28.38B |

| Total Liabilities | 8.40B | 9.85B | 9.03B | 10.43B | 17.49B |

| Long Term Debt | 1.09B | 725.75M | 174.78M | 1.94B | 7.70B |

| Shareholders Equity | 26.61B | 22.85B | 20.82B | 19.11B | 10.89B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 6.32B | 4.11B | 3.96B | 3.82B | 874.55M |

| Operating Activities Other Non Cash Items | 1.11B | -83.67M | -55.36M | 116.69M | 596.00M |

| Operating Activities Accounts Receivable | -337.83M | -706.62M | 240.18M | 788.73M | -861.25M |

| Operating Activities Other Assets Liabilities | -1.46B | -1.24B | 2.00B | 4.44B | 1.52B |

| Operating Activities Operating Cash Flow | 5.63B | 2.08B | 6.14B | 9.16B | 2.13B |

| Investing Activities Capital Expenditures | -4.13B | -4.85B | -3.45B | -4.19B | -3.66B |

| Investing Activities Net Acquisitions | 259.00K | -202.50M | -90.63M | 0.00 | -4.41M |

| Investing Activities Investing Cash Flow | -4.13B | -5.06B | -3.54B | -4.19B | -3.67B |

| Financing Activities Common Dividends | -889.66M | -889.66M | -1.12B | -338.46M | N/A |

| Financing Activities Financing Cash Flow | -889.66M | -889.66M | -1.12B | 4.66B | 520.00K |

| End Cash Position | 795.40M | 898.57M | 3.12B | 3.15B | -818.60M |

| Free Cash Flow | 1.24B | -1.93B | 3.26B | 6.32B | 4.65B |

| Financing Activities Common Stock Issuance | N/A | N/A | 0.00 | 5.00B | 0.00 |

| Investing Activities Other Investing Activity | N/A | N/A | N/A | -100.00K | -100.00K |

| Financing Activities Other Financing Charges | N/A | N/A | N/A | 260.00K | 520.00K |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend shows mixed price action with the stock trading below the 50-day moving average (₹569.86) but above the 200-day moving average (₹365.32), indicating intermediate-term consolidation.

- Key support levels are identified near ₹365 and ₹184, while resistance is observed around ₹570 and the 52-week high of ₹760.

- The stock is positioned above the 200-day moving average, suggesting long-term bullishness, but below the 10-day and 50-day moving averages, indicating short-term weakness.

- Momentum indicators show RSI near neutral levels, MACD signals a potential bearish crossover, and stochastic oscillators reflect mixed momentum across timeframes.

- Daily and weekly charts indicate consolidation within a broad range, while monthly charts show an overall upward trend since the previous year.

- Potential market scenarios include a breakout above the 50-day moving average leading to renewed upward momentum or a breakdown below the 200-day moving average triggering further declines.

Trending News

Summary: The index has lost 8.00% over last one month. Among the constituents, Jindal Steel Ltd dropped 6.67%, Hindalco Industries Ltd fell 6.16% and Hindustan Copper Ltd shed 5.89%. The Nifty Metal index has increased 29.00% over last one year compared to the 3.37% spike in benchmark Nifty 50 index.

Sentiment: negative

2. Headline: HINDUSTAN COPPER Share Price Today Down 6%

Summary: The top losers among the BSE Sensex ... Eternal Ltd. In the meantime, NSE Nifty is at 23,153.2 (down 2.1%). L&T and Hindalco are among the top losers in NSE NIFTY. Over the last 12 months, the BSE Sensex has moved up from 74,102.3 to 74,563.9, registering a gain of 461.6 points (up 0.6%). HINDUSTAN COPPER net profit ...

Sentiment: negative

3. Headline: Buy Hindustan Copper; target of Rs 650: Anand Rathi

Summary: Anand Rathi is bullish on Hindustan Copper has recommended buy rating on the stock with a target price of Rs 650 in its research report dated March 13, 2026.

Sentiment: positive

4. Headline: Shri Anupam Misra Recommended as CMD of Hindustan Copper Limited – PESB 2026

Summary: General Manager, STC of India Ltd. Briefly held additional charge as CMD of FACT in early 2026 · Shri Misra’s extensive experience in marketing, international trade, and management makes him well-suited to lead HCL in its next phase of growth. ... Hindustan Copper Limited, incorporated in ...

Sentiment: positive

5. Headline: Hindustan Copper, MCX and 3 other stocks reported up to 1,461% sales and profit growth in Q3

Summary: Coming to financial highlights, ... of India Ltd’s revenue has increased from Rs. 301 crore in Q3 FY25 to Rs. 666 crore in Q3 FY26, which has grown by 121 percent. The net profit has also grown by 151 percent from Rs. 160 crore in Q3 FY25 to Rs. 401 crore in Q3 FY26. Hindustan Copper Limited (HCL), ...

Sentiment: positive

6. Headline: Hindustan Copper Wins Stay on Jharkhand Mining Demand, Operations Protected for Now - TipRanks.com

Summary: Hindustan Copper Ltd ( ($IN:HINDCOPPER) ) has shared an update. Hindustan Copper Ltd has disclosed that India’s Ministry of Mines, acting as the Revisionary Authori...

Sentiment: positive

7. Headline: 19 Best Copper Stocks in the World 2026 – Worth Buying? - XS

Summary: Looking to invest in copper stocks in 2026? Find out which 19 companies and ETFs stand out, what supports copper prices, and whether they’re worth buying.

Sentiment: neutral

8. Headline: Hindustan Copper Ltd Sees High-Value Trading Amid Mixed Market Signals

Summary: Hindustan Copper Ltd (HINDCOPPER), a key player in the Non-Ferrous Metals sector, witnessed one of the highest value turnovers on 16 Feb 2026, with total traded value exceeding ₹248.6 crores. Despite a modest decline in share price, the stock continues to attract significant institutional ...

Sentiment: positive

9. Headline: Hindustan Copper Ltd Sees Robust Trading Activity Amid Sector Outperformance

Summary: Hindustan Copper Ltd (HINDCOPPER) emerged as one of the most actively traded stocks by value on 12 Feb 2026, reflecting strong investor interest and robust market participation. The stock outperformed its sector and broader indices, buoyed by significant volume and value turnover, alongside ...

Sentiment: positive

10. Headline: Dividend Stocks: Mazagon Dock, Hindustan Copper, MGL And More — Last Day To Buy Shares To Qualify

Summary: Shares of Mazagon Dock Shipbuilders Ltd., Hindustan Copper Ltd., Mahanagar Gas Ltd. will be of interest on Thursday, as the day marks the last session for investors to buy shares to qualify for receiving the dividend before the stock goes ex/record-date. The record date determines the eligible ...

Sentiment: neutral

Powered by Brave

Recent Updates

News Summary

Recent news highlights a mixed but generally positive outlook for Hindustan Copper Ltd. The company has successfully secured a stay on Jharkhand mining demands, ensuring continued operations and regulatory compliance. Leadership changes with the appointment of Shri Anupam Misra as CMD bring experienced management to guide future growth. Financially, the stock has demonstrated strong momentum, achieving multibagger status with over 100% rally in six months, reflecting robust market interest. However, geopolitical tensions such as the Iran war pose potential risks by increasing freight and input costs, which could pressure margins. Overall, these developments indicate a company balancing growth opportunities with operational and external challenges in a dynamic market environment.

News Sentiment

Sentiment trends lean positive with several reports emphasizing strong financial performance, leadership renewal, and operational safeguards. Negative sentiment is limited and primarily linked to external geopolitical factors and sector volatility. The overall sentiment mix suggests cautious optimism, with market participants recognizing both growth potential and risk factors.

Analytical Overview

Analysis Summary

Hindustan Copper's trailing P/E ratio of 81.58 is significantly higher than the industry average, while the forward P/E of 26.83 suggests expected earnings growth; however, the elevated price-to-book ratio of 18.20 indicates a premium valuation relative to book value.

The company demonstrates a positive revenue growth trajectory with quarterly revenue growth of 9.7% and strong cash flow generation, including operating cash flow of ₹5.63 billion and free cash flow of ₹4.65 billion, supporting operational sustainability.

Financial health is moderate with a total debt to equity ratio of 4.78 and a current ratio of 1.37, reflecting manageable liquidity but relatively high leverage requiring monitoring.

Sector-specific challenges include commodity price volatility and geopolitical risks impacting input costs, while opportunities arise from government support and domestic demand growth.

Considering the Indian market environment, regulatory frameworks favor public sector undertakings, and consumer trends support infrastructure development, which may benefit Hindustan Copper's strategic positioning.

Investment Conclusion

Supporting Factors: Primary supporting factors include robust revenue and profit growth, strong cash flow metrics, and government backing.

Risk Factors: Main risks involve elevated valuation levels, high debt relative to equity, and exposure to commodity price fluctuations and geopolitical uncertainties.

SWOT Analysis

Strengths

- Government ownership provides strategic support and stability.

- Integrated operations from mining to finished copper products enhance control and efficiency.

- Strong revenue growth and profitability with a 24.93% profit margin.

- Robust cash flow generation supports operational needs and investments.

Weaknesses

- High valuation multiples relative to earnings and book value.

- Elevated debt-to-equity ratio of 4.78 indicates significant leverage.

- Limited institutional ownership may reduce market liquidity.

- Dividend yield remains low at approximately 0.18%.

Opportunities

- Growing domestic demand for copper driven by infrastructure and technology sectors.

- Leadership renewal with experienced management may drive strategic initiatives.

- Regulatory approvals securing mining operations enhance operational continuity.

- Potential to increase market share through expanded production capacity.

Threats

- Commodity price volatility impacting revenue and margins.

- Geopolitical tensions increasing input and freight costs.

- Regulatory changes or environmental restrictions affecting mining activities.

- Market competition from global copper producers and substitutes.

Company Description

Hindustan Copper Ltd. is a government-owned enterprise engaged in the mining, smelting, and refining of copper and related products in India. As a central public sector undertaking, its primary purpose is to harness the country's copper resource potential and manufacture a wide range of copper-based products, including copper cathodes, wire rods, and other by-products. The company's activities are integrated and span from mining copper ore to marketing finished products across various regions. Hindustan Copper Ltd. plays a significant role in sectors such as transportation, electrical industries, construction, and telecommunications due to the essential nature of copper as a conductor and its use in alloys. Its operations contribute to the domestic supply of copper, supporting infrastructure development and technological advancements within the country. Established in 1967, the company's strategic importance lies in its ability to bolster India’s self-sufficiency in copper production, thus enhancing the nation’s industrial framework. Operating key mines across India, Hindustan Copper Ltd. not only boosts domestic production capacities but also aligns with governmental goals to utilize indigenous mineral resources effectively.