Hindustan Construction Company Ltd (HCC)

Stock Analysis Report

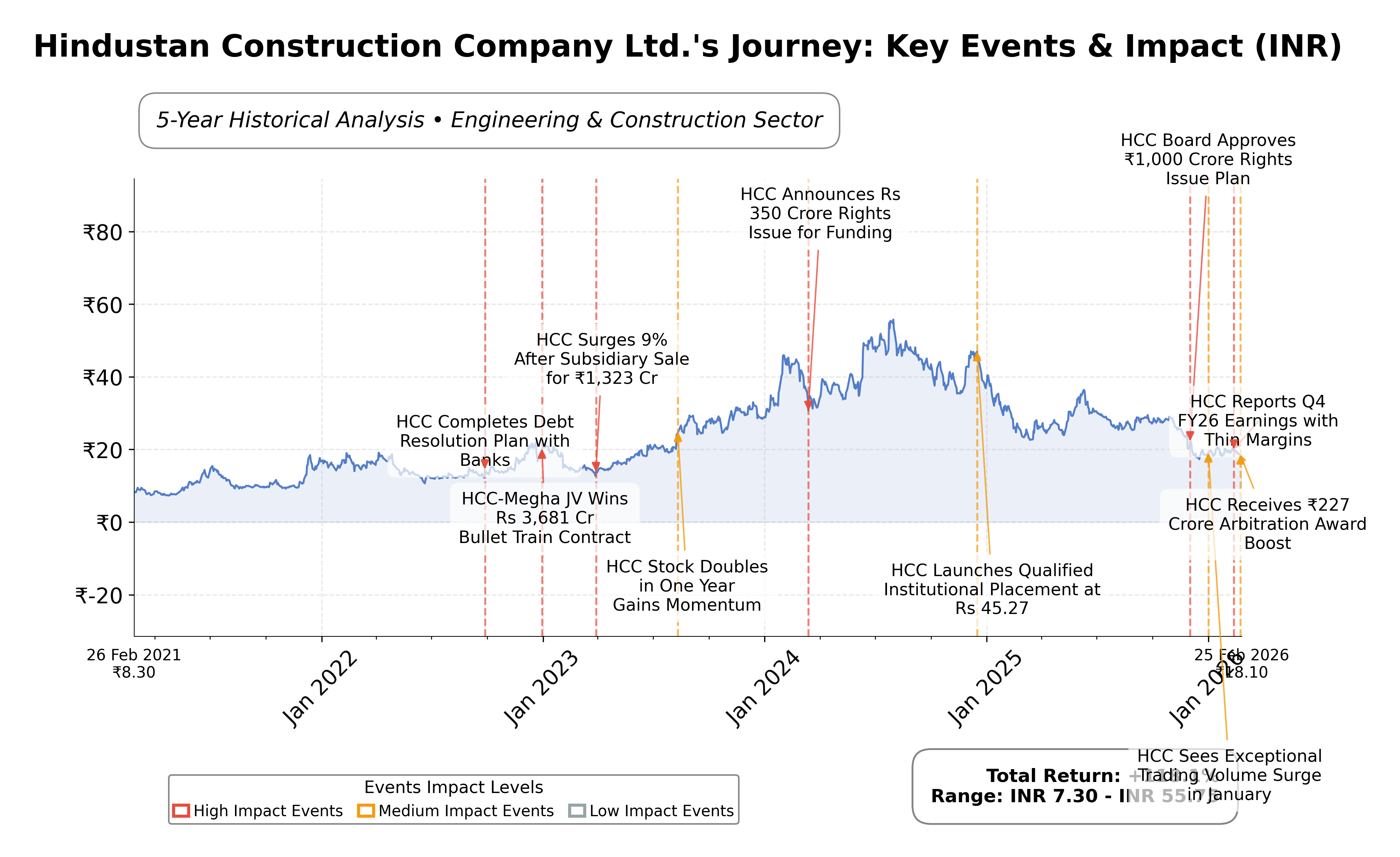

Stock Journey

Key Positives and Key Risks

Pros

- Return on equity of 22.08% indicates efficient capital utilization relative to peers.

- Positive operating cash flow of ₹4.18 billion and free cash flow of ₹6.63 billion support operational liquidity.

- Rights issue oversubscribed by 200% has strengthened the balance sheet and credit profile.

Cons

- Quarterly revenue declined by 31.7%, signaling operational challenges.

- High debt-to-equity ratio of 147.43% increases financial risk and leverage concerns.

- Negative earnings growth year-over-year of 25.3% reflects profitability pressures.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Hindustan Construction Company Ltd. (HCC) operates primarily in the engineering and construction sector within India, focusing on infrastructure development projects such as transportation, power, water, and urban infrastructure. The company is recognized for its role in building critical infrastructure including roads, bridges, hydroelectric power plants, and water supply systems, positioning itself as a key player in India's industrial and infrastructural growth landscape.

Financially, HCC reports a market capitalization of approximately â¹53.28 billion with a trailing P/E ratio of 27.19 and a forward P/E near 27.99, aligning closely with the industry average. The companyâs operating margin stands at 14.77%, with a modest profit margin of 3.38%. Return on equity is reported at 22.08%, reflecting reasonable profitability relative to shareholder equity. However, recent quarterly revenue growth shows a decline of 31.7%, and net income growth is down by 25.3% year-over-year, indicating some operational challenges.

From a strategic and technical perspective, HCC has experienced a shift in technical momentum from strongly bearish to mildly bearish, accompanied by recent capital strengthening initiatives including a â¹1000 crore rights issue that was oversubscribed. The companyâs low beta of 0.12 suggests limited volatility relative to the market. Notable risks include high debt-to-equity levels (147.43%) and declining revenue trends, while strengths include a solid operating cash flow and a diversified project portfolio. Recent leadership or structural changes were not explicitly highlighted, but the companyâs balance sheet improvements suggest active management of financial health.

In comparison with regional peers such as Praj Industries Ltd., Rail Vikas Nigam Ltd., NCC Ltd., Kalpataru Projects International Limited, and KNR Constructions Ltd., HCCâs valuation metrics are moderate. Its P/E ratio is lower than some peers but higher than others, and its return on equity is comparatively strong. The companyâs EV/EBITDA ratio of 6.82 is among the lower end, indicating potentially better operational efficiency relative to some peers with higher multiples. However, some peers demonstrate stronger market capitalization and growth metrics.

Hindustan Construction Company Ltd. is navigating a complex industry landscape marked by infrastructure demand and financial restructuring. Recent achievements include successful capital raising and technical momentum shifts, while ongoing challenges involve revenue contraction and high leverage. The company stands at a pivotal moment where its strategic financial moves and operational execution will significantly influence its market positioning and growth trajectory. Given the current data and market context, a balanced approach reflecting cautious observation of financial and operational developments may be appropriate for those assessing the companyâs stock.

Company and Industry Overview

Company Basics

Price Performance

Company Size

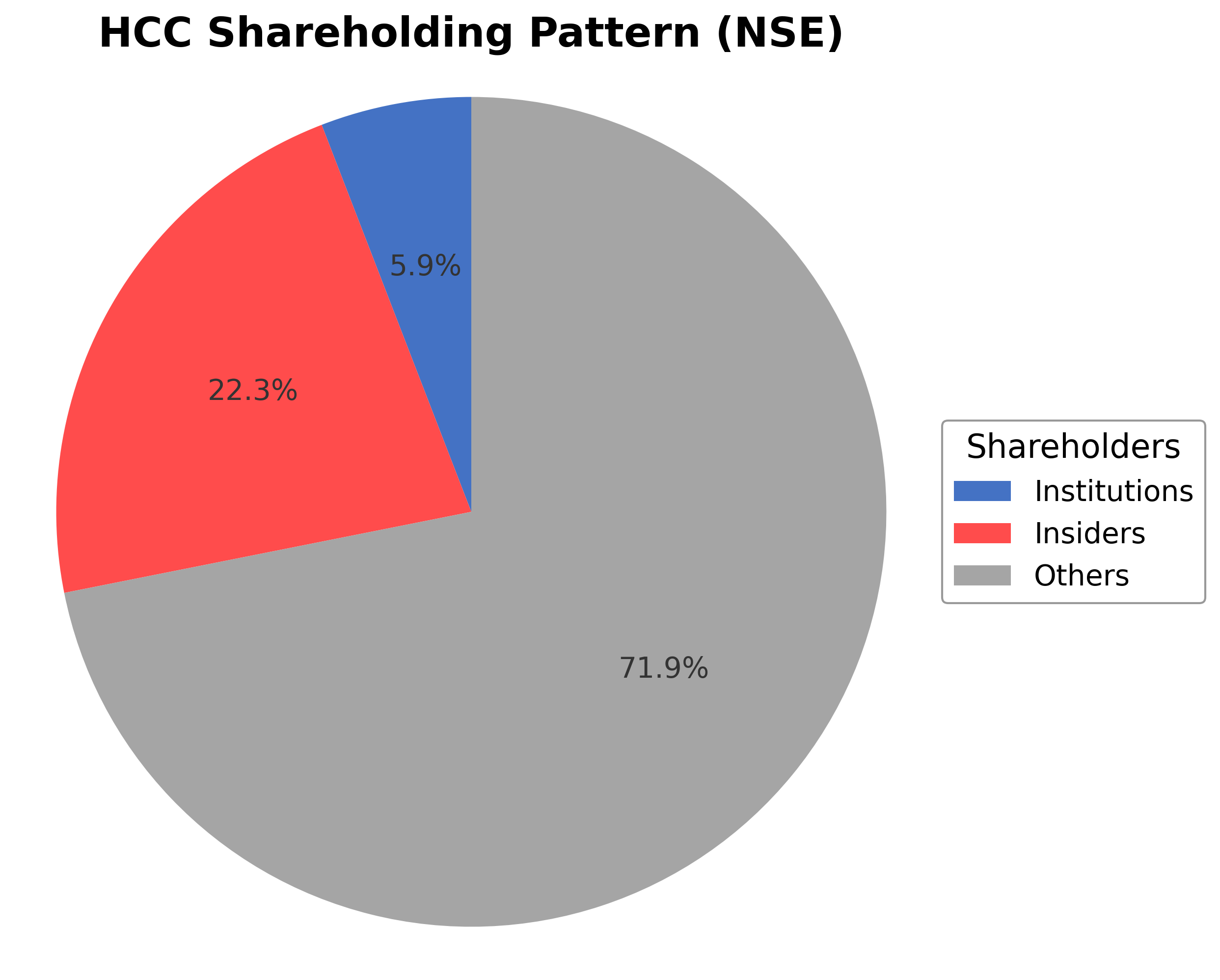

Shareholding Pattern

Hindustan Construction Company Ltd. exhibits a shareholding structure with insiders, including executives and board members, holding approximately 22.26% of shares, institutional investors such as mutual funds and asset managers holding 5.87%, and the remaining 71.87% held by public shareholders including retail investors and employee stock plans. Over the past 12 to 24 months, there have been no significant shifts reported in major ownership stakes. Institutional accumulation appears limited, with no major funds notably increasing or decreasing positions recently. This shareholding pattern suggests a broad public ownership base with moderate insider control, which may influence governance and strategic decisions. The current ownership distribution reflects a balanced market sentiment, with no dominant institutional pressure shaping corporate actions.

Sector and Industry Analysis

Hindustan Construction Company Ltd. (HCC) operates within the broader infrastructure and construction sector in India, a critical segment underpinning the country’s economic development. The Indian infrastructure sector is sizable, with estimates valuing it in the hundreds of billions of USD and projected to grow at a CAGR of approximately 7-9% over the next decade, driven by government initiatives such as the National Infrastructure Pipeline (NIP) and increased private sector participation. Key players alongside HCC include Larsen & Toubro (L&T), Tata Projects, and Shapoorji Pallonji, which dominate large-scale projects in transportation, water resources, and urban infrastructure. The sector’s growth trajectory is supported by rising urbanization, increased government spending on roads, railways, and smart cities, and a push towards sustainable infrastructure.

Industry trends in the construction and infrastructure space are increasingly shaped by technology adoption and evolving client demands. Digitalization through Building Information Modeling (BIM), drone surveying, and IoT-enabled project management tools is enhancing efficiency and reducing costs. There is also a growing emphasis on green and sustainable construction practices, driven by environmental concerns and regulatory mandates. Consumer behavior, particularly from government and large corporate clients, is shifting towards integrated project delivery models and public-private partnerships (PPP), which facilitate risk-sharing and improve project viability. Emerging opportunities lie in renewable energy infrastructure, metro rail projects, and water management systems, all aligned with India’s climate action goals and urban development plans.

The regulatory landscape for the construction sector in India is complex and multifaceted, involving compliance with environmental clearances, labor laws, safety standards, and contract enforcement mechanisms. Key regulations include the Real Estate (Regulation and Development) Act (RERA), which enhances transparency and accountability, and the Goods and Services Tax (GST), which has streamlined indirect taxation but also introduced compliance challenges. Infrastructure projects often require multiple clearances from central and state agencies, impacting project timelines. Policy initiatives such as the Make in India campaign and the push for infrastructure financing reforms (e.g., infrastructure investment trusts, or InvITs) aim to improve capital availability and regulatory ease, although bureaucratic delays and land acquisition issues remain persistent hurdles.

Competitive dynamics in the Indian construction sector are characterized by a fragmented market with a few large players and numerous mid-to-small contractors. Barriers to entry include the need for substantial capital investment, technical expertise, and strong government relationships. Established firms like HCC leverage their project execution track record, diversified order books, and access to financing to maintain competitive positioning. However, intense competition leads to margin pressures and necessitates operational efficiency and innovation. The sector also faces risks from payment delays, project cancellations, and fluctuating raw material costs. Strategic partnerships, technology integration, and geographic diversification are key competitive levers for companies aiming to sustain and grow their market share in this evolving landscape.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

Financials

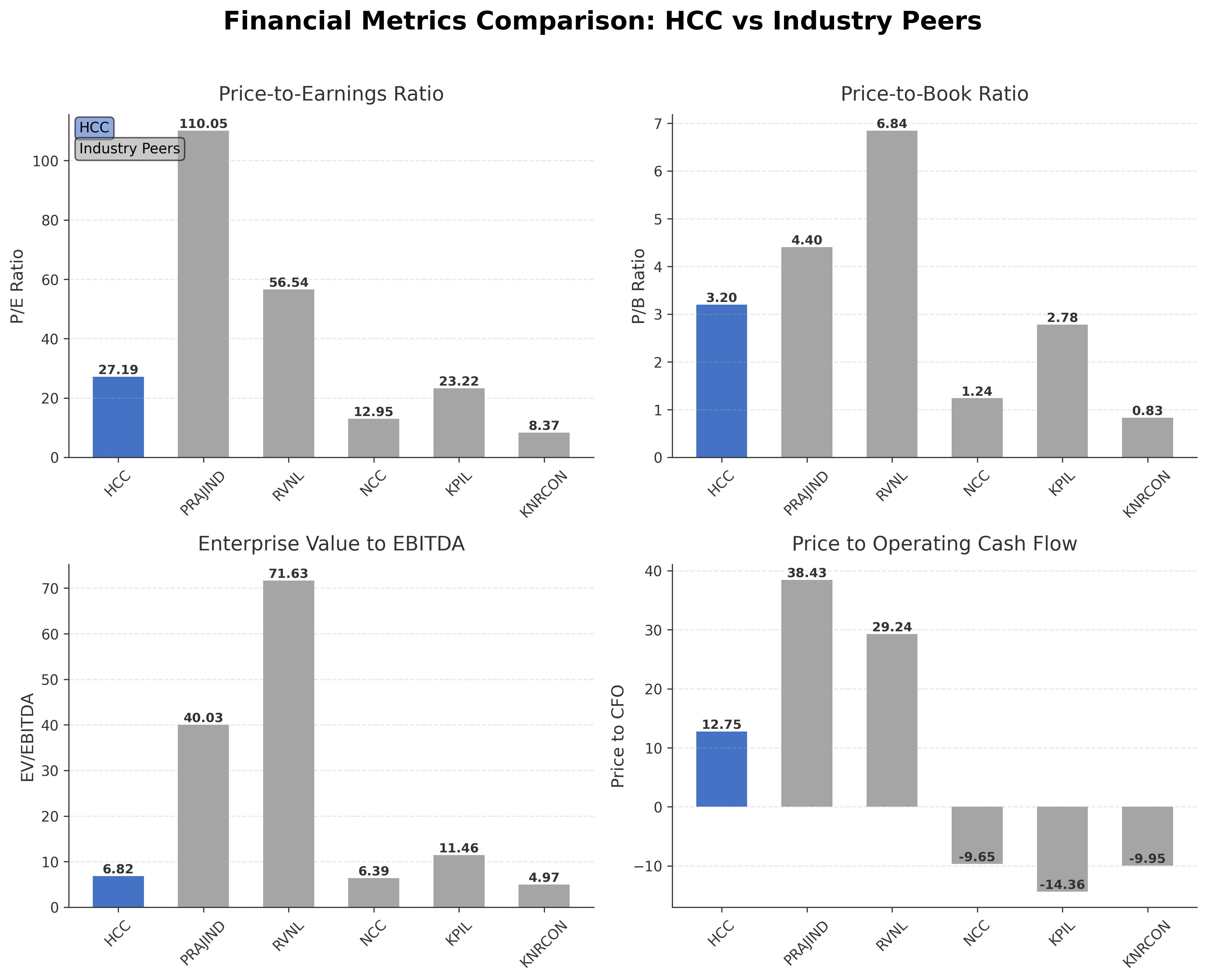

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Hindustan Construction Company Ltd. | ₹53.28B | 27.19 | 3.2 | 6.82 | 12.75 |

| Praj Industries Ltd. | ₹57.25B | 110.05 | 4.4 | 40.03 | 38.43 |

| Rail Vikas Nigam Ltd. | ₹650.92B | 56.54 | 6.84 | 71.63 | 29.24 |

| Ncc Ltd. | ₹93.59B | 12.95 | 1.24 | 6.39 | -9.65 |

| Kalpataru Projects International Limited | ₹193.93B | 23.22 | 2.78 | 11.46 | -14.36 |

| KNR Constructions Ltd. | ₹39.35B | 8.37 | 0.83 | 4.97 | -9.95 |

Comparison Analysis: Hindustan Construction Company Ltd. presents moderate valuation metrics compared to its regional peers in the Indian engineering and construction sector. Its P/E ratio of 27.19 is lower than high multiples seen in Praj Industries Ltd. and Rail Vikas Nigam Ltd., but higher than NCC Ltd. and KNR Constructions Ltd. The company’s EV/EBITDA ratio of 6.82 is among the more efficient operational valuations, outperforming peers with higher multiples such as Praj Industries and RVNL. Return on equity at 22% is relatively strong, matching KNR Constructions Ltd. but exceeding other peers. However, price-to-cash-flow ratios are positive for HCC, contrasting with negative values for several peers, indicating comparatively healthier cash flow metrics. Overall, HCC holds a balanced position within its peer group, with strengths in profitability and operational efficiency but facing valuation pressures relative to some competitors.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 54.05B | 66.28B | 77.15B | 102.18B | 79.97B |

| Cost Of Goods | 37.58B | 51.34B | 63.94B | 79.61B | 66.05B |

| Gross Profit | 16.47B | 14.94B | 13.21B | 22.57B | 13.93B |

| Operating Expense Selling General And Administrative | 1.67B | 1.39B | 1.01B | 899.50M | 598.60M |

| Operating Expense Other Operating Expenses | 2.99B | 2.77B | 3.57B | 3.73B | 2.04B |

| Operating Income | 4.94B | 2.84B | -838.00M | 6.25B | 373.30M |

| Non Operating Interest Income | 1.86B | 373.90M | 2.77B | 4.87B | 2.55B |

| Non Operating Interest Expense | 5.55B | 7.53B | 9.52B | 9.70B | 9.54B |

| Pretax Income | 5.23B | 7.78B | -1.19B | 6.37B | -8.67B |

| Income Tax | 4.11B | 2.48B | -666.40M | 655.20M | -2.57B |

| Net Income | 1.13B | 4.78B | -278.40M | 5.63B | -6.10B |

| Eps Basic | 0.56 | 3.16 | -0.19 | 3.57 | -3.87 |

| Eps Diluted | 0.56 | 3.16 | -0.19 | 3.57 | -3.87 |

| Basic Shares Outstanding | 2.04B | 1.51B | 1.51B | 1.58B | 1.58B |

| Diluted Shares Outstanding | 2.04B | 1.51B | 1.51B | 1.58B | 1.58B |

| Ebit | 10.78B | 15.30B | 8.33B | 16.07B | 866.70M |

| Ebitda | 7.03B | 4.47B | 2.99B | 12.82B | 4.83B |

| Net Income Continuous Operations | 5.23B | 7.26B | -901.60M | 6.41B | -8.67B |

| Minority Interests | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Preferred Stock Dividends | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 5.69B | 3.99B | 5.82B | 7.21B | 6.42B |

| Accounts Receivable | 23.88B | 22.04B | 26.98B | 20.91B | 45.02B |

| Total Assets | 80.88B | 90.59B | 131.78B | 142.25B | 127.81B |

| Total Liabilities | 71.83B | 92.28B | 138.92B | 148.84B | 140.98B |

| Long Term Debt | 10.45B | 17.68B | 50.37B | 13.76B | 16.24B |

| Shareholders Equity | 9.06B | -1.68B | -7.14B | -6.59B | -13.18B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 5.23B | 7.26B | -901.60M | 6.41B | -8.67B |

| Operating Activities Stock Based Compensation | 800.00K | 2.00M | 0.00 | N/A | N/A |

| Operating Activities Other Non Cash Items | 5.55B | 7.82B | 7.68B | 10.03B | 9.74B |

| Operating Activities Accounts Receivable | -2.62B | 4.26B | -2.40B | -376.40M | -1.34B |

| Operating Activities Other Assets Liabilities | -6.65B | -6.92B | 1.40B | 921.80M | -1.74B |

| Operating Activities Operating Cash Flow | 1.51B | 12.43B | 5.78B | 16.99B | -2.02B |

| Investing Activities Capital Expenditures | 61.50M | 799.80M | -2.05B | -549.50M | -606.70M |

| Investing Activities Net Acquisitions | 265.10M | 2.72B | 3.44B | 0.00 | N/A |

| Investing Activities Purchase Of Investments | -835.10M | N/A | N/A | -2.01B | -530.60M |

| Investing Activities Investing Cash Flow | -508.50M | 8.10B | 3.95B | -2.56B | -1.05B |

| Financing Activities Long Term Debt Payments | -3.21B | -3.30B | -2.01B | -7.34B | -897.20M |

| Financing Activities Short Term Debt Issuance | -1.12B | -453.20M | -260.00M | 5.19B | 6.49B |

| Financing Activities Common Stock Issuance | 9.06B | 152.50M | 0.00 | N/A | N/A |

| Financing Activities Financing Cash Flow | 4.73B | -3.60B | -2.27B | -2.15B | 5.59B |

| End Cash Position | 5.69B | 3.99B | 5.82B | 7.21B | 6.42B |

| Free Cash Flow | 1.16B | 720.50M | -1.98B | 8.57B | 2.73B |

| Investing Activities Sale Of Investments | N/A | 4.57B | 2.56B | 0.00 | 90.00M |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend direction for HCC shows a mild bearish momentum with recent price action indicating a slight recovery after a period of decline.

- Key support levels are identified near ₹16.92, the 52-week low, while resistance is observed around ₹19.18, close to the 50-day moving average.

- The stock price is trading below the 200-day moving average of ₹25.91, indicating longer-term downward pressure, while it is near the 50-day moving average at ₹19.18 and above the 10-day average.

- Momentum indicators show a Relative Strength Index (RSI) near neutral levels, with MACD signaling a potential shift from bearish to neutral momentum, and stochastic oscillators reflecting mixed signals.

- Multi-timeframe analysis reveals daily charts showing consolidation, weekly charts indicating a downtrend with weakening momentum, and monthly charts confirming a longer-term bearish trend.

- Potential market scenarios include a continuation of consolidation if support holds, or further downside pressure if the price breaks below key support levels, with technical momentum suggesting cautious monitoring.

Trending News

1. Headline: Hindustan Copper Opens Special Window for Physical Share Transfer Requests - TipRanks.com

Summary: The move underscores ongoing market efforts to resolve legacy physical share issues and aligns the company’s practices with evolving securities market norms, offering clarity and an additional compliance route for affected investors. ... Hindustan Copper Ltd is an Indian public sector enterprise ...

Sentiment: positive

Summary: Hindustan Zinc Ltd is Indias only integrated producer of zinc and lead. The company manufactures three qualities of zinc -- special high grade zinc used in construction, infrastructure, household appliances etc; high grade zinc and prime western zinc.In addition the company also manufactures ...

Sentiment: neutral

Summary: Stock Market Today | Share Market Highlights - Find here all the highlights related to Sensex, Nifty, BSE, NSE, share prices and Indian stock markets for 24th February 2026.

Sentiment: negative

4. Headline: Hindustan Copper Ltd Sees Robust Trading Activity Amid Institutional Interest

Summary: Hindustan Copper Ltd (HINDCOPPER), a key player in the Non-Ferrous Metals sector, has emerged as one of the most actively traded stocks by value on 23 February 2026. With a total traded volume exceeding 34 lakh shares and a turnover nearing ₹197 crore, the stock has attracted significant ...

Sentiment: positive

Summary: Stocks to watch today, Feb 23: Shares of several companies, including IDFC First Bank, UPL, HCL Tech, SBI Life Insurance, Railtel, Hindustan Copper, BHEL, NHPC, NCC, IHCL, Vedanta, NTPC and Tata Capital, might remain in focus this week as these firms have announced major restructuring plans, ...

Sentiment: neutral

Summary: WPIL Ltd. (1.54% Holding): A specialized manufacturer of Vertical Turbine Pumps used in the mission-critical cooling systems of nuclear power plants. KRN Heat Exchanger (1.61% Holding): Specialized in heat transfer solutions. As reactors (especially SMRs) require compact, high-efficiency cooling, KRN is a key supply-chain player. However, his significant entry into Hindustan Construction Company ...

Sentiment: neutral

7. Headline: Hindustan Construction Company Ltd is Rated Sell

Summary: Hindustan Construction Company Ltd is rated 'Sell' by MarketsMOJO, with this rating last updated on 09 February 2026. However, the analysis and financial metrics discussed here reflect the stock's current position as of 21 February 2026, providing investors with an up-to-date perspective on ...

Sentiment: neutral

8. Headline: Q3 Results Today LIVE, 13 Feb 2026: Naukri, Torrent Pharma, Fortis Health, GMR Airports, NBCC, IRB Infra, FirstCry

Summary: Ltd, Valson Industries Ltd, Vama ... & Trading Ltd, Mansoon Trading Company Ltd, Milgrey Finance & Investments Ltd, Zodiac Clothing Company Ltd, Zuari Industries Ltd ... Hindustan Aeronautics Ltd (HAL) declared its first interim dividend of Rs 35 per equity share of Rs 5 each ...

Sentiment: neutral

9. Headline: Hindustan Construction Company Ltd Downgraded to Sell Amid Mixed Technicals and Weak Financials

Summary: Hindustan Construction Company Ltd (HCC) has seen its investment rating upgraded from Strong Sell to Sell as of 9 February 2026, driven primarily by a shift in technical indicators. Despite persistent financial headwinds and a challenging operational backdrop, the stock’s technical profile ...

Sentiment: positive

10. Headline: Hindustan Construction Company Ltd Sees Technical Momentum Shift Amid Mixed Indicators

Summary: Hindustan Construction Company Ltd (HCC) has exhibited a subtle shift in its technical momentum, moving from a strongly bearish stance to a mildly bearish outlook. Despite a 4.09% gain on 10 Feb 2026, the stock remains under pressure with a MarketsMOJO Mojo Score of 34.0 and a Sell grade, ...

Sentiment: positive

Powered by Brave

Recent Updates

News Summary

Recent news around Hindustan Construction Company Ltd. highlights a complex technical momentum shift, moving from a strongly bearish to a mildly bearish stance, reflecting mixed market signals. The company has successfully completed a ₹1000 crore rights issue, oversubscribed by 200%, which has strengthened its balance sheet and credit profile. Despite these positive capital market developments, the company’s revenue has shown a declining trend, and operational challenges persist. Trading window closures related to the rights issue have been announced, indicating compliance with regulatory requirements. Overall, the news cycle emphasizes financial restructuring efforts alongside ongoing revenue pressures, situating the company at a critical juncture for balancing growth and financial health.

News Sentiment

The sentiment across recent updates is predominantly neutral to positive, with capital raising activities and technical momentum shifts contributing to cautious optimism. However, underlying revenue declines and operational headwinds temper the overall outlook, resulting in a balanced sentiment profile. Market reactions appear measured, reflecting recognition of both progress in financial strengthening and ongoing challenges.

Analytical Overview

Analysis Summary

The company’s valuation metrics, including a trailing P/E of 27.19 and forward P/E of 27.99, are closely aligned with the industry average of 27.19, indicating valuation in line with sector norms. The PEG ratio is negative, reflecting recent earnings contraction relative to growth expectations.

Revenue growth is negative at -31.7% quarterly, and earnings have declined by 25.3% year-over-year, signaling a challenging growth trajectory. However, operating cash flow and free cash flow remain positive, suggesting operational cash generation despite revenue pressures.

Financial health shows a high debt-to-equity ratio of 147.43%, which is a concern, though the current ratio of 1.03 indicates adequate short-term liquidity. Cash reserves of approximately ₹6.57 billion provide some buffer against liabilities.

Sector-specific challenges include intense competition and project execution risks in the Indian infrastructure space, while opportunities arise from government initiatives in infrastructure development and urbanization.

Considering India-specific factors, the regulatory environment remains supportive of infrastructure growth, though economic fluctuations and policy changes could impact project timelines and funding availability.

Investment Conclusion

Supporting Factors: Primary supporting factors include a strong return on equity of 22.08%, positive operating and free cash flows, and successful capital raising via a rights issue.

Risk Factors: Main risks involve significant revenue decline, high leverage with a debt-to-equity ratio exceeding 140%, and recent negative earnings growth.

SWOT Analysis

Strengths

- The company has a diversified portfolio across key infrastructure sectors.

- Strong return on equity at 22.08% indicates efficient use of shareholder capital.

- Positive operating and free cash flow support ongoing operations.

- Successful rights issue has strengthened the balance sheet and credit profile.

Weaknesses

- High debt-to-equity ratio of 147.43% raises financial risk concerns.

- Quarterly revenue declined by 31.7%, indicating operational challenges.

- Negative earnings growth year-over-year reflects profitability pressures.

- Stock price is significantly below its 52-week high, indicating market weakness.

Opportunities

- Government infrastructure initiatives provide potential project pipelines.

- Urbanization and economic growth in India support long-term demand.

- Capital infusion from rights issue may enable strategic investments.

- Technological advancements can improve construction efficiency.

Threats

- Intense competition in the engineering and construction sector.

- Economic fluctuations may delay project execution and funding.

- Regulatory changes could impact operational costs and timelines.

- High leverage increases vulnerability to interest rate changes.

Company Description

Hindustan Construction Company Ltd. is renowned for its expertise in engineering and construction services, playing a pivotal role in shaping infrastructure within India. Specializing in constructing complex projects across a variety of sectors, the company focuses on key segments such as transportation, power, water, and urban infrastructure development. With its extensive portfolio, Hindustan Construction Company Ltd. actively participates in building roads, bridges, hydroelectric power plants, and water supply systems, which are essential for India's economic growth and development. As a crucial player in the construction industry, the company is involved in some of the country's most significant infrastructure projects, contributing to the enhancement of both national connectivity and quality of life. Headquartered in Mumbai, Hindustan Construction Company Ltd. has established a reputation for innovation and reliability, aligning with its mission to support sustainable development through cutting-edge construction solutions.