HDFC Bank Limited (HDFCBANK)

Stock Analysis Report

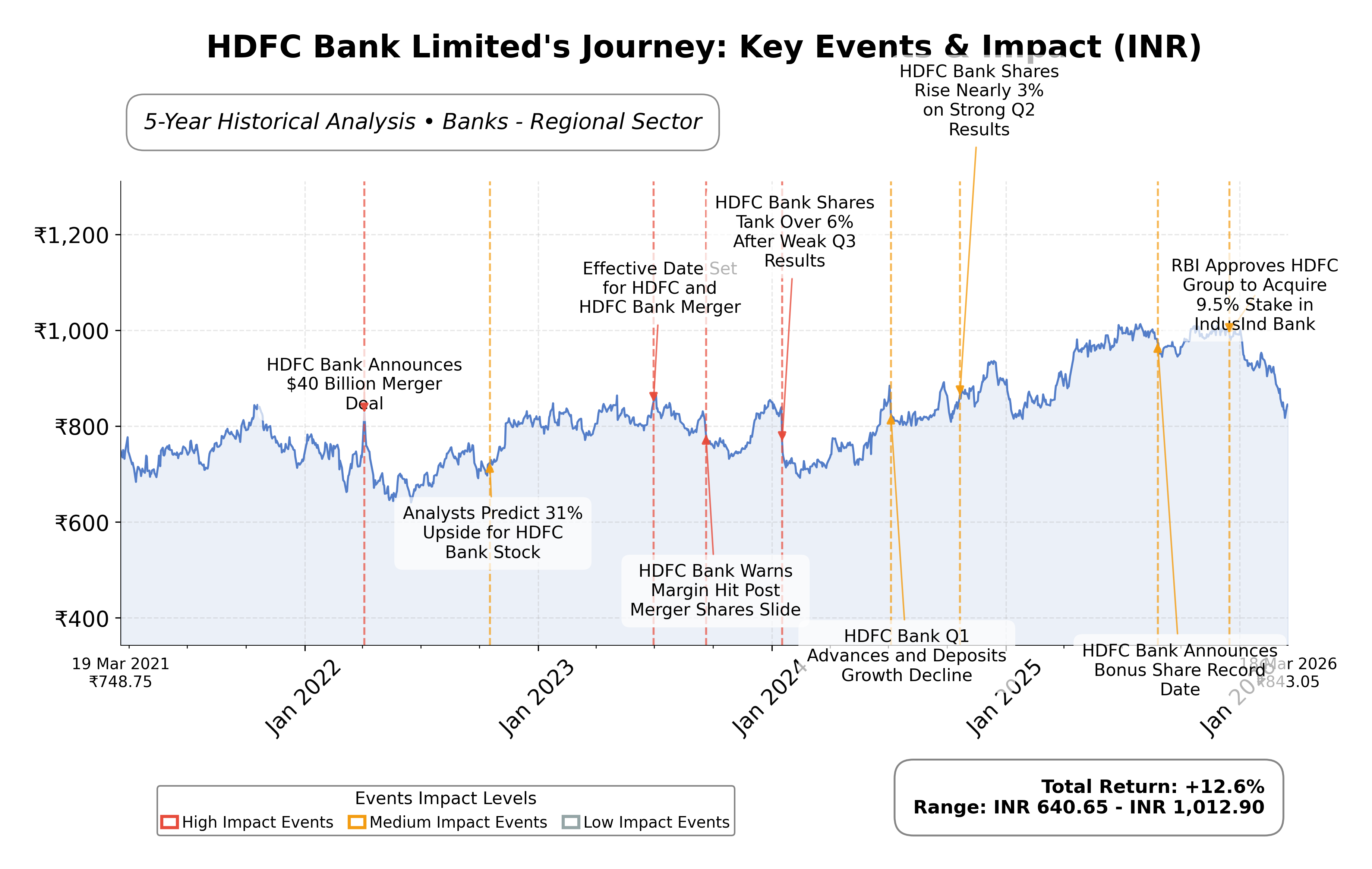

Stock Journey

Key Positives and Key Risks

Pros

- Strong revenue growth of 26.4% year-over-year demonstrates robust business expansion.

- Return on equity of 14.02% indicates effective capital utilization compared to peers.

- Institutional ownership at 55.80% reflects confidence from major investment entities.

Cons

- Recent resignation of part-time chairman raises governance and leadership concerns.

- Stock price trading below 50-day and 200-day moving averages suggests short-term weakness.

- High debt-to-equity ratio of 1.09 may indicate leverage risks relative to cash reserves.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

HDFC Bank Limited operates as one of India's largest private sector banks, providing a broad spectrum of retail and wholesale banking services. Established in 1994, it holds a significant position in the Indian financial services industry, with extensive branch and ATM networks and a strong emphasis on digital innovation and customer service. The bank's offerings include personal loans, credit cards, insurance, investment banking, and treasury management, catering to both individual and corporate clients across urban and rural regions. Its strategic focus on technology-driven solutions and financial inclusion underscores its market relevance and growth potential.

Financially, HDFC Bank exhibits robust metrics including a trailing P/E ratio of 18.24 and a forward P/E of 14.64, reflecting valuation slightly below the industry average P/E of 18.24. The bank reported a net income of approximately INR 745 billion with a profit margin of 26.19% and a return on equity of 14.02% on a trailing twelve months basis. Market capitalization stands at INR 12.57 trillion, with a price-to-book ratio of 2.22 and a dividend yield of 0.31%. The bank maintains a strong cash position of over INR 1.9 trillion and manageable debt levels, supporting operational stability.

Recent developments include leadership changes marked by the resignation of the part-time chairman over governance concerns, which has introduced some uncertainty. However, the bank continues to receive positive institutional interest, with notable stake increases by major funds. Technical indicators reveal the stock trading below its 50-day and 200-day moving averages, suggesting cautious momentum. Strengths include its market leadership, digital capabilities, and financial resilience, while risks encompass governance challenges and market volatility.

In comparison to regional peers such as City Union Bank, Bank of Maharashtra, and IDBI Bank, HDFC Bank commands a substantially larger market capitalization and superior return on equity, albeit at a higher valuation multiples. Its P/E and P/B ratios exceed those of most peers, reflecting premium market positioning. Peers exhibit more varied financial performance and valuation, with some smaller banks trading at lower multiples but also showing lower profitability metrics.

HDFC Bank stands at a pivotal juncture within the Indian banking sector, balancing strong operational fundamentals against recent governance and leadership challenges. The bank's continued focus on innovation and expansion positions it well for sustained growth, yet the evolving management dynamics and market conditions introduce elements of uncertainty. The outcomes of these factors will significantly influence its competitive standing and investor perception. Given the current data and market context, a measured approach emphasizing observation of forthcoming developments and financial performance trends may be appropriate for those assessing the stock.",

Company and Industry Overview

Company Basics

Price Performance

Company Size

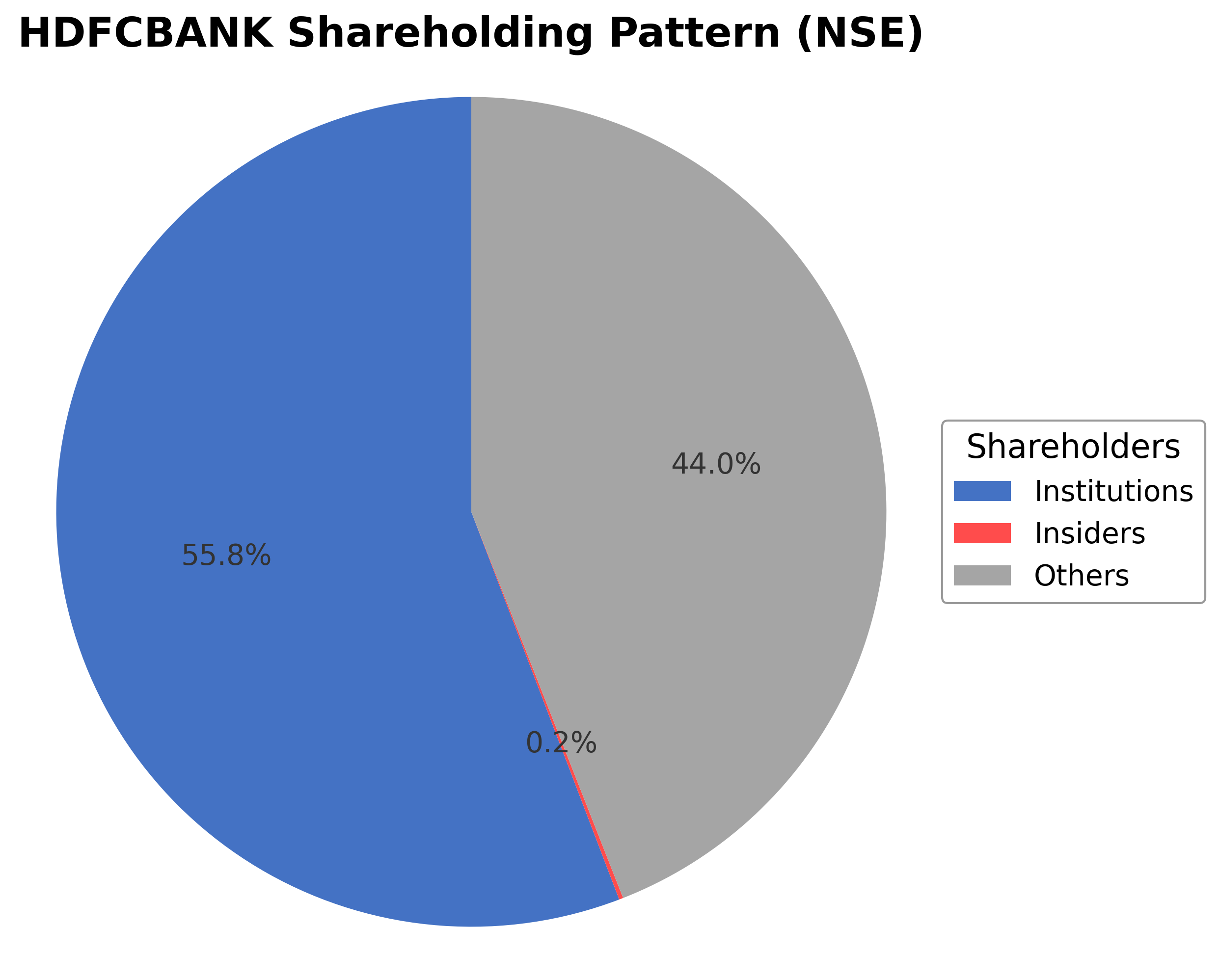

Shareholding Pattern

HDFC Bank Limited's ownership structure is characterized by a minimal promoter holding of approximately 0.16%, reflecting limited insider ownership. Institutional investors hold a significant majority stake at 55.80%, indicating strong participation from mutual funds, pension funds, and asset managers. The remaining 44.04% is held by public shareholders, including retail investors and employee stock plans. Over the past 12-24 months, institutional ownership has shown an upward trend with notable accumulation by major funds such as Kontiki Capital Management HK Ltd. and Bamco Inc. NY, which have increased their positions substantially. These shareholding patterns suggest a positive market sentiment towards the bank's governance and strategic direction, with institutional confidence potentially supporting future corporate initiatives. The dominant institutional presence may also influence governance practices and strategic decision-making within the company.

Sector and Industry Analysis

The Indian banking sector, within which HDFC Bank Limited operates, represents one of the largest and most dynamic segments of the country’s financial services industry. With a market capitalization exceeding ₹12.9 trillion, the sector is characterized by a mix of public sector banks, private sector banks, and foreign banks, collectively serving over a billion consumers. The banking sector’s growth trajectory has been robust, driven by expanding retail and corporate credit demand, digital financial inclusion initiatives, and rising economic activity. Key players include HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra Bank, and State Bank of India, which dominate in terms of assets, branch network, and customer base. The sector continues to see steady expansion in branch networks and customer acquisition, with HDFC Bank alone operating around 9,600 branches and serving approximately 100 million customers.

Industry trends reveal a significant shift towards digital transformation and technology adoption, reshaping traditional banking models. The proliferation of mobile banking, UPI (Unified Payments Interface), and fintech collaborations have enhanced customer convenience and operational efficiency. Consumer behavior is evolving with increased demand for personalized, relationship-based banking services rather than purely price-driven offerings, especially in retail segments such as auto loans and mortgages. Emerging opportunities include growth in underserved rural and semi-urban markets, expansion of digital lending platforms, and integration of AI and data analytics for credit risk assessment and customer engagement. However, challenges persist in deposit mobilization and margin improvement, with banks like HDFC Bank experiencing stagnant deposit growth and margin pressures amid competitive and macroeconomic headwinds.

The regulatory landscape governing the Indian banking sector is comprehensive and evolving, primarily overseen by the Reserve Bank of India (RBI). Key regulations include capital adequacy norms under Basel III, priority sector lending mandates, and stringent Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements. Recent policy shifts emphasize financial stability, risk management, and consumer protection, impacting credit growth strategies and product offerings. Compliance with agricultural financing norms and sector-specific lending guidelines also shapes banks’ portfolio management. Regulatory focus on digital security and data privacy is increasing, reflecting the sector’s digital pivot. Policy measures aimed at fostering credit flow to priority sectors coexist with prudential norms that constrain aggressive risk-taking, influencing banks’ strategic recalibrations.

Competitive dynamics in the Indian banking industry are marked by an oligopolistic market structure dominated by a handful of large private and public sector banks. Barriers to entry remain high due to regulatory capital requirements, established brand loyalty, extensive branch and digital infrastructure, and the need for robust risk management frameworks. HDFC Bank’s competitive positioning is strengthened by its extensive retail franchise, strong profitability metrics, and focus on customer relationships rather than aggressive pricing. The sector faces intense competition in key segments like retail loans and digital payments, with fintech firms and non-banking financial companies (NBFCs) increasingly encroaching on traditional banking domains. Strategic differentiation through technology integration, product innovation, and branch productivity enhancement remains critical for maintaining market share and profitability in this highly competitive environment.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

Financials

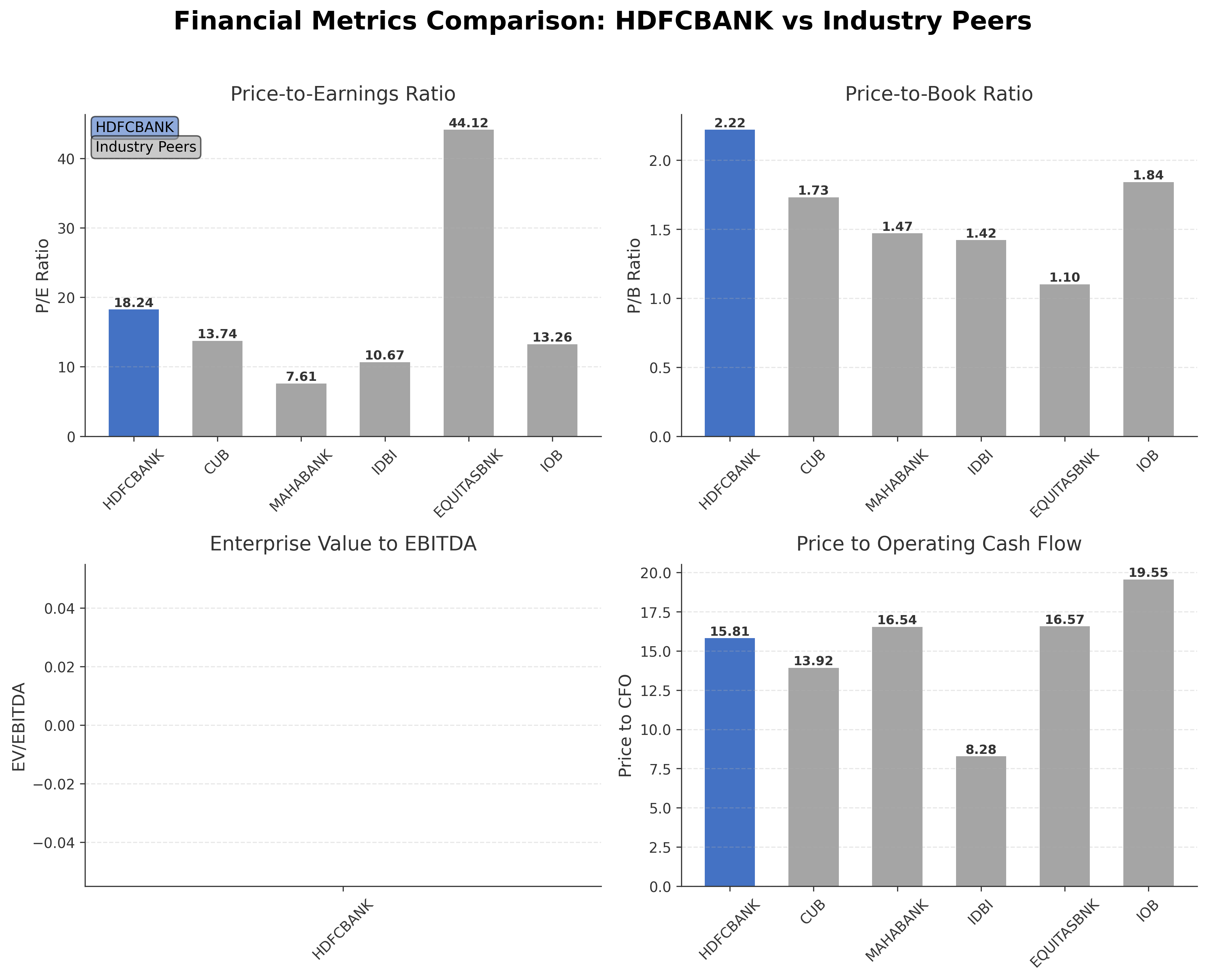

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| HDFC Bank Limited | ₹12.57T | 18.24 | 2.22 | N/A | 15.81 |

| City Union Bank Ltd. | ₹172.02B | 13.74 | 1.73 | N/A | 13.92 |

| Bank of Maharashtra | ₹492.95B | 7.61 | 1.47 | N/A | 16.54 |

| IDBI Bank Ltd. | ₹991.25B | 10.67 | 1.42 | N/A | 8.28 |

| Equitas Small Finance Bank Limited | ₹64.41B | 44.12 | 1.10 | N/A | 16.57 |

| Indian Overseas Bank | ₹628.31B | 13.26 | 1.84 | N/A | 19.55 |

Comparison Analysis: HDFC Bank Limited stands out among its regional banking peers with a substantially larger market capitalization of ₹12.57 trillion, reflecting its dominant market position. The bank's P/E ratio of 18.24 is higher than most peers, indicating a premium valuation relative to smaller banks such as Bank of Maharashtra and IDBI Bank, which trade at lower multiples but exhibit varied return on equity levels. HDFC Bank's return on equity of 14.02% is competitive within the peer group, outperforming several banks but trailing Bank of Maharashtra's 21%. Price-to-book and price-to-cash-flow ratios also suggest a relatively higher valuation, consistent with its scale and profitability. Overall, HDFC Bank's metrics reflect its leadership and premium status in the Indian regional banking sector, while peers demonstrate a range of valuations and financial performance profiles.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 2371.51B | 1986.93B | 1205.38B | 1019.41B | 936.66B |

| Operating Expense Selling General And Administrative | 1124.88B | 951.76B | 400.22B | 320.22B | 292.98B |

| Pretax Income | 861.55B | 705.46B | 662.38B | 519.16B | 439.83B |

| Income Tax | 175.01B | 77.83B | 166.12B | 132.56B | 113.82B |

| Net Income | 686.53B | 627.63B | 496.26B | 386.60B | 326.01B |

| Eps Basic | 45.01 | 88.66 | 89.02 | 69.76 | 59.27 |

| Eps Diluted | 44.81 | 88.31 | 88.68 | 69.38 | 59.02 |

| Basic Shares Outstanding | 15.26B | 7.08B | 5.57B | 5.53B | 5.50B |

| Diluted Shares Outstanding | 15.26B | 7.08B | 5.57B | 5.53B | 5.50B |

| Net Income Continuous Operations | 686.53B | 627.63B | 496.26B | 386.60B | 326.01B |

| Minority Interests | -13.02B | -4.98B | -817.50M | -602.60M | -29.30M |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 3222.32B | 3425.97B | 2363.92B | 1599.22B | 1041.38B |

| Accounts Receivable | 323.23B | 249.94B | 194.53B | 136.49B | 123.69B |

| Total Assets | 48187.67B | 44118.57B | N/A | N/A | N/A |

| Total Liabilities | 39564.78B | 36232.39B | N/A | N/A | N/A |

| Long Term Debt | 6020.09B | 6779.81B | 2061.90B | 1632.47B | 1245.18B |

| Shareholders Equity | 8622.89B | 7886.18B | 2917.84B | 2509.45B | 2163.40B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 686.53B | 627.63B | 496.26B | 386.60B | 326.01B |

| Operating Activities Depreciation | 63.02B | 52.35B | 23.49B | 16.82B | 13.86B |

| Operating Activities Deferred Taxes | -15.61B | -57.13B | 12.28B | -9.89B | -8.27B |

| Operating Activities Stock Based Compensation | 24.63B | 20.12B | 14.01B | 13.87B | 10.60B |

| Operating Activities Other Non Cash Items | 34.73B | 18.61B | 4.64B | 790.70M | 3.42B |

| Operating Activities Accounts Receivable | -72.88B | -24.10B | -51.40B | -15.64B | -15.80B |

| Operating Activities Accounts Payable | 19.36B | 12.95B | 29.89B | 4.42B | -2.07B |

| Operating Activities Other Assets Liabilities | 55.41B | 447.77B | -201.55B | 22.62B | 470.48B |

| Operating Activities Operating Cash Flow | 795.18B | 1098.19B | 327.64B | 419.59B | 798.22B |

| Investing Activities Capital Expenditures | -65.42B | -52.30B | -43.19B | -26.13B | -17.65B |

| Investing Activities Net Acquisitions | 0.00 | 149.80B | 0.00 | 0.00 | N/A |

| Investing Activities Purchase Of Investments | -4710.47B | -4308.27B | -1595.30B | -1736.50B | -3217.28B |

| Investing Activities Sale Of Investments | 3158.04B | 3540.58B | 1031.73B | 1588.66B | 2393.48B |

| Investing Activities Investing Cash Flow | -1617.85B | -670.20B | -606.76B | -173.96B | -841.46B |

| Financing Activities Long Term Debt Issuance | 661.23B | 1155.78B | 1022.93B | 722.91B | 481.99B |

| Financing Activities Long Term Debt Payments | -1463.10B | -1400.30B | -558.11B | -353.33B | -326.29B |

| Financing Activities Short Term Debt Issuance | -13.44B | 222.25B | 535.73B | 314.74B | -138.02B |

| Financing Activities Common Dividends | -158.06B | -86.62B | -86.39B | -36.24B | -166.60M |

| Financing Activities Other Financing Charges | 6.01B | 3.64B | 822.70M | 691.80M | 492.40M |

| Financing Activities Financing Cash Flow | -967.36B | -31.55B | 914.98B | 648.77B | 18.01B |

| End Cash Position | 1982.93B | 2086.03B | 1387.40B | 1122.03B | 930.69B |

| Income Tax Paid | 195.41B | 199.75B | 163.67B | 148.38B | 130.21B |

| Interest Paid | 1803.80B | 1407.75B | 745.49B | 579.85B | 594.39B |

| Free Cash Flow | 1129.22B | 968.48B | 433.58B | 554.69B | 903.97B |

| Financing Activities Common Stock Issuance | N/A | 76.00B | N/A | N/A | 0.00 |

| Financing Activities Common Stock Repurchase | N/A | -2.30B | N/A | N/A | N/A |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend direction shows the stock trading below its 50-day moving average of ₹915.99 and 200-day moving average of ₹969.14, indicating a short to medium-term bearish momentum.

- Key support levels are near the 52-week low of ₹812, while resistance is observed around the 52-week high of ₹1020.5 and the 200-day moving average.

- The stock price is positioned below both the 10-day and 50-day moving averages, suggesting downward pressure in the near term.

- Momentum indicators such as RSI and MACD are currently neutral to slightly bearish, with RSI levels indicating neither oversold nor overbought conditions.

- Multi-timeframe analysis across daily, weekly, and monthly charts shows consistent consolidation with a mild downward bias, reflecting cautious market sentiment.

- Potential market scenarios include a continuation of consolidation near support levels or a rebound if the price breaks above key moving averages, contingent on broader market conditions.

Trending News

1. Headline: India's HDFC Bank says chairman exit may be over rift with management; stock falls | Reuters

Summary: Chakraborty, a former bureaucrat, was appointed as HDFC Bank's chairman in April 2021 for a three-year term and reappointed in 2024 through May 2027. "While governance standards have historically been strong for the bank, the current episode raises concerns about aspects that we may have limited ...

Sentiment: negative

2. Headline: HDFC Bank shares fall 5% as part-time chair of India’s largest private bank resigns over 'ethics'

Summary: Interim part‑time chairman, Keki Mistry, said that Atanu Chakraborty, had not provided the board with any evidence or details of the alleged unethical practices.

Sentiment: negative

3. Headline: HDFC Bank chairman quits over 'values and ethics'; Keki Mistry is interim head | Reuters

Summary: India's HDFC Bank said late on Wednesday that its part-time chairman, Atanu Chakraborty, had resigned citing differences with the lender over "values and ethics", and appointed insider Keki Mistry as interim part-time chairman.

Sentiment: negative

4. Headline: [6-K] HDFC BANK LTD Current Report (Foreign Issuer) | HDB SEC Filing - Form 6-K

Summary: HDFC Bank Limited reported that India Ratings and Research Private Limited assigned and affirmed strong credit ratings on several of its instruments on March 17, 2026.

Sentiment: positive

5. Headline: Greenfield Seitz Capital Management LLC Acquires 55,533 Shares of HDFC Bank Limited $HDB

Summary: Greenfield Seitz Capital Management LLC lifted its stake in HDFC Bank Limited (NYSE:HDB - Free Report) by 99.3% in the third quarter, according to the company in its most recent filing with the Securities and Exchange Commission. The institutional investor owned 111,479 shares of the bank's stock

Sentiment: positive

6. Headline: HDFC Bank Limited (HDB): Billionaire Ken Fisher Admires This Indian Company

Summary: HDFC Bank Limited (NYSE:HDB) is one of Billionaire Ken Fisher’s 15 Most Notable Moves for 2026. HDFC Bank Limited (NYSE:HDB) is one of the few foreign companies that occupy a prominent position in the 13F portfolio of Fisher Asset Management. Fisher has held a stake in this banking stock ...

Sentiment: neutral

7. Headline: HDFC Bank officer reports initial share and option holdings | HDB SEC Filing - Form 3

Summary: Jul 15, 2025 HDFC Bank Limited Form 20-F for the Year Ended March 31, 2025 Available Online

Sentiment: neutral

8. Headline: Kontiki Capital Management HK Ltd. Has $253.44 Million Stock Position in HDFC Bank Limited $HDB

Summary: Kontiki Capital Management HK Ltd. grew its holdings in HDFC Bank Limited (NYSE:HDB - Free Report) by 97.4% in the 3rd quarter, according to the company in its most recent filing with the SEC. The firm owned 7,419,143 shares of the bank's stock after buying an additional 3,661,469 shares during the

Sentiment: positive

9. Headline: HDFC Bank Limited $HDB Stock Position Lifted by Bamco Inc. NY

Summary: Bamco Inc. NY grew its holdings in shares of HDFC Bank Limited (NYSE:HDB - Free Report) by 100.2% during the third quarter, according to its most recent Form 13F filing with the SEC. The firm owned 107,320 shares of the bank's stock after purchasing an additional 53,725 shares during the period. Ba

Sentiment: positive

10. Headline: Earnest Partners LLC Has $81.76 Million Stock Holdings in HDFC Bank Limited $HDB

Summary: Earnest Partners LLC boosted its position in HDFC Bank Limited (NYSE:HDB - Free Report) by 97.9% during the third quarter, according to its most recent disclosure with the Securities and Exchange Commission (SEC). The fund owned 2,393,566 shares of the bank's stock after acquiring an additional 1,1

Sentiment: positive

Powered by Brave

Recent Updates

News Summary

Recent news highlights a mix of leadership changes and positive institutional interest in HDFC Bank Limited. The resignation of the part-time chairman over governance and ethical disagreements has introduced uncertainty and led to a decline in share price. Concurrently, several institutional investors, including prominent funds, have increased their holdings significantly, reflecting confidence in the bank's long-term fundamentals. Credit rating affirmations by India Ratings and Research further underscore the bank's financial strength. These developments collectively shape the current narrative around HDFC Bank, balancing governance challenges with strong market support and creditworthiness.

News Sentiment

Overall sentiment is mixed with a tilt towards cautious optimism. Negative sentiment arises from leadership instability and governance concerns, while positive sentiment is driven by institutional accumulation and credit rating affirmations. The divergence in sentiment reflects the complexity of the bank's current position, with market participants weighing risks against underlying financial resilience.

Analytical Overview

Analysis Summary

Valuation Metrics: HDFC Bank's trailing P/E of 18.24 and forward P/E of 14.64 are in line with or slightly below the industry average of 18.24, indicating a valuation consistent with its market position. The price-to-book ratio of 2.22 suggests a premium relative to many regional peers, reflecting investor confidence in the bank's asset quality and growth prospects.

Growth Trajectory: The bank demonstrates a strong revenue growth rate of 26.4% year-over-year, supported by a 12.2% quarterly earnings growth. Operating and profit margins remain healthy, with operating margin at 34.79% and profit margin at 26.19%. Cash flow trends are positive, with operating cash flow of approximately INR 795 billion and free cash flow of INR 673 billion, underscoring solid operational efficiency.

Financial Health: HDFC Bank maintains a robust balance sheet with total assets of INR 48.19 trillion and a manageable debt-to-equity ratio of 1.09. Cash reserves exceed INR 1.9 trillion, providing liquidity buffers. The bank's return on equity of 14.02% and return on assets of 1.75% indicate effective capital utilization and asset management.

Sector-Specific Factors: The Indian banking sector is influenced by regulatory frameworks promoting financial inclusion and digital banking innovation, areas where HDFC Bank is well positioned. However, challenges include governance scrutiny, competitive pressures from fintech, and macroeconomic factors affecting credit quality. The bank's strategic focus on technology and rural outreach aligns with sector growth drivers.

India-Specific Market Factors: India's evolving regulatory environment emphasizes transparency and risk management, impacting banking operations. Consumer trends favor digital banking adoption, benefiting HDFC Bank's technology initiatives. Economic outlook remains positive, supporting credit demand and financial sector expansion, though geopolitical and inflationary risks persist.

Investment Conclusion

Supporting Factors: No data

Risk Factors: No data

SWOT Analysis

Strengths

- Market leader with a large and diversified customer base across India.

- Strong revenue growth and healthy profit margins.

- Robust balance sheet with significant cash reserves.

- Advanced digital banking capabilities and extensive branch network.

Weaknesses

- Recent leadership resignation raises governance concerns.

- Stock price trading below key moving averages indicating short-term weakness.

- Relatively high valuation multiples compared to some regional peers.

- Limited promoter shareholding may affect insider alignment.

Opportunities

- Expansion in rural and semi-urban markets supporting financial inclusion.

- Growing adoption of digital banking services among consumers.

- Potential for strategic partnerships and technological innovation.

- Favorable regulatory environment promoting banking sector growth.

Threats

- Governance and management instability could impact investor confidence.

- Competitive pressures from fintech and other private banks.

- Macroeconomic risks including inflation and credit quality deterioration.

- Regulatory changes imposing stricter compliance requirements.

Company Description

HDFC Bank Limited, a leading financial institution, serves as one of India's largest private sector banks. Established in 1994, it is a prominent player in retail and wholesale banking services. HDFC Bank provides a comprehensive range of financial products and services including personal loans, credit cards, insurance, investment banking, and treasury management. With a vast network of branches and ATMs across India, it ensures wide accessibility to its customers. The bank is renowned for its digital innovation and robust customer service practices, significantly contributing to the advancement of the Indian banking sector. HDFC Bank plays a crucial role in the financial ecosystem, supporting economic growth through services that cater to both individual consumers and corporate clients. Its strategic focus on technology-driven solutions and expansion aligns with the dynamic needs of the market, marking its significance in the financial landscape. Furthermore, HDFC Bank has been instrumental in promoting financial inclusion by providing banking services in rural and semi-urban areas, thereby fostering economic development across diverse regions.