Dishman Carbogen Amcis Ltd (DCAL)

Stock Analysis Report

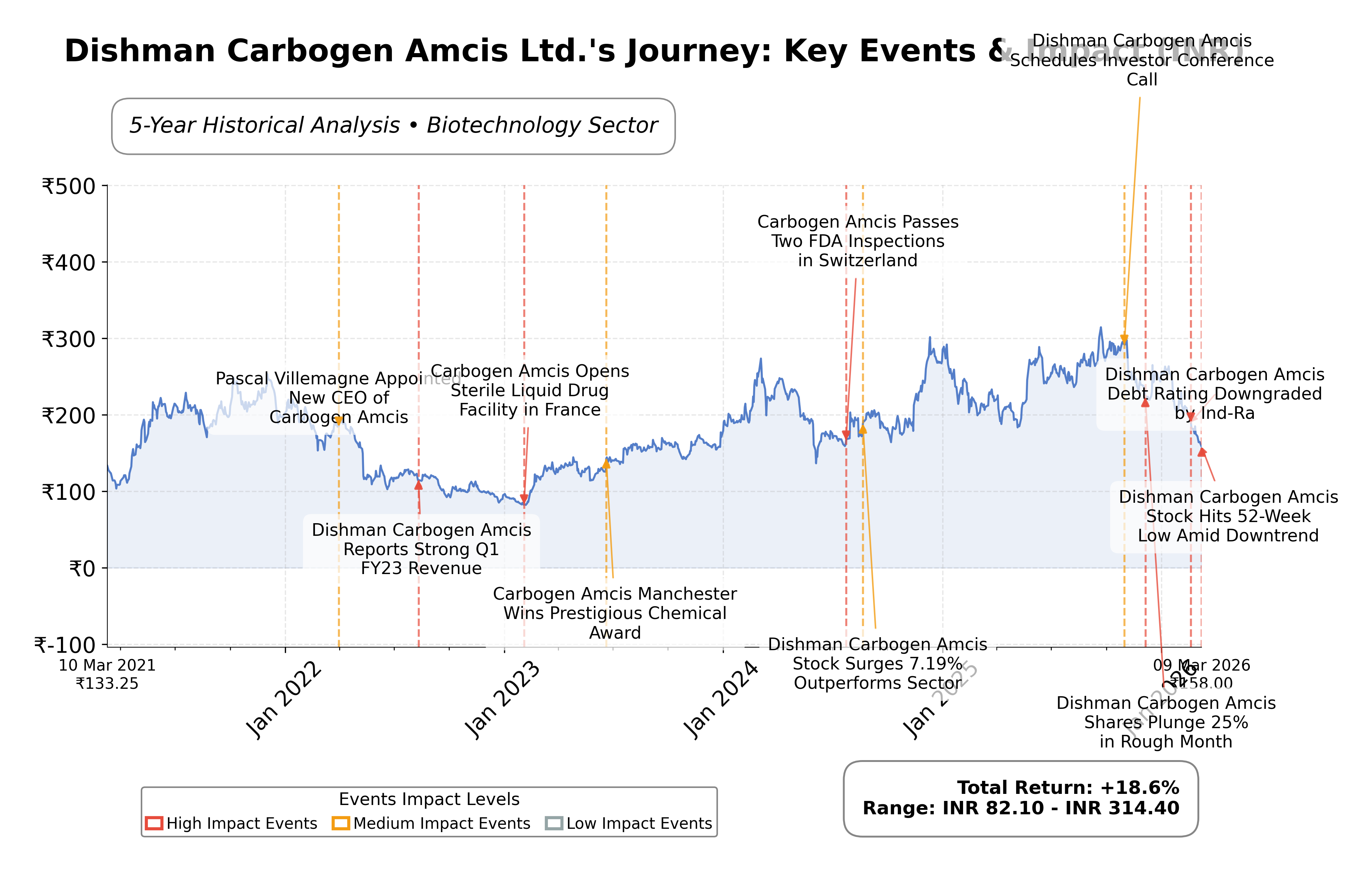

Stock Journey

Key Positives and Key Risks

Pros

- Forward P/E ratio of 12.48 indicates market expectations of earnings improvement relative to current valuation.

- Positive free cash flow of ₹32.4 million suggests some operational liquidity despite negative operating cash flow.

- Promoter ownership at 69.3% provides strategic stability and continuity in corporate governance.

Cons

- High total debt of ₹25.59 billion and debt-to-equity ratio of 40.20 indicate significant financial leverage and risk.

- Negative quarterly earnings growth year-over-year at -8.78% reflects pressure on profitability.

- Stock trading near 52-week low with price below 50-day and 200-day moving averages signals bearish technical momentum.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Dishman Carbogen Amcis Ltd. (DCAL) operates as a contract research and manufacturing services (CRAMS) provider within the biotechnology sector, primarily serving pharmaceutical, biopharmaceutical, and healthcare industries. The company specializes in developing active pharmaceutical ingredients (APIs), intermediates, and specialty chemicals, supporting drug development from discovery through commercialization. Headquartered in India with a global footprint, DCAL holds a significant position in the pharmaceutical supply chain by enabling efficiency and reducing time-to-market for new medications.

Financially, DCAL reports a market capitalization of approximately â¹24.89 billion with a trailing P/E ratio of 20.55 and a forward P/E of 12.48, indicating a valuation discount relative to some peers. The companyâs price-to-book ratio stands at 0.38, reflecting a market valuation below its book value. Revenue for the trailing twelve months is â¹27.97 billion, with a modest quarterly revenue growth of 5.5%. Profit margins are thin, with a net margin of 4.25% and return on equity near zero (0.06%). The balance sheet shows total assets close to â¹100 billion, with significant debt of â¹25.59 billion and a current ratio of 1.14, indicating moderate liquidity. Cash flow metrics reveal slight negative operating cash flow but positive free cash flow.

Technically, the stock is trading near its 52-week low of â¹154.5, with the current price at â¹161.33, below both the 50-day (â¹215.18) and 200-day (â¹250.64) moving averages, signaling a bearish trend. Momentum indicators show weakness, and recent strategic initiatives include a planned capital raise and expansion investments by its subsidiary. Leadership changes or notable governance shifts have not been highlighted recently. Key risks include high leverage, low profitability, and recent credit rating downgrades, while strengths lie in its integrated service offerings and global presence.

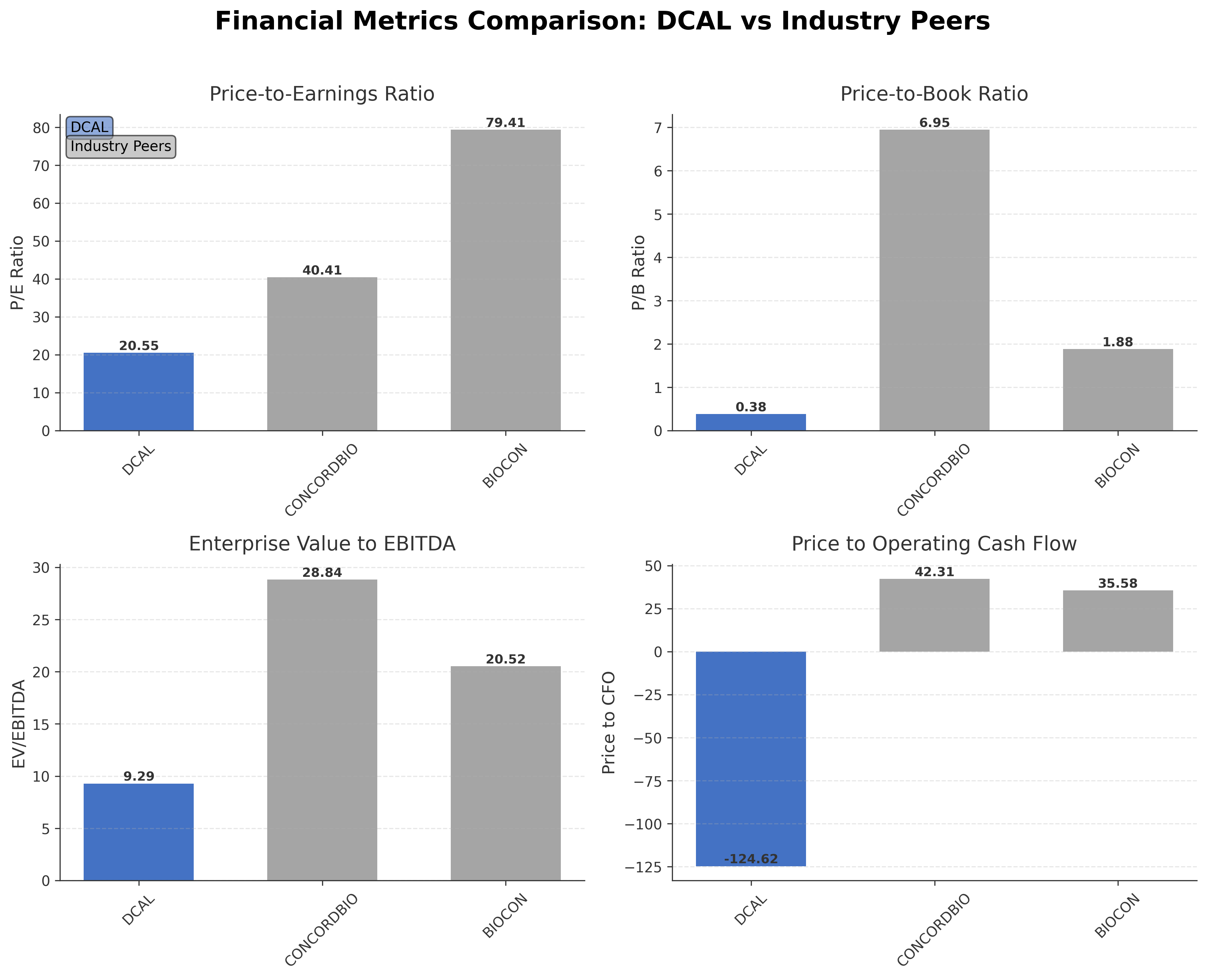

In comparison with regional peers such as Concord Biotech Ltd. and Biocon Ltd., DCALâs market capitalization is smaller (â¹24.89B vs. â¹126.29B and â¹632.67B respectively). Its valuation multiples are lower, with a trailing P/E of 20.55 versus 40.41 and 79.41 for Concord Biotech and Biocon, and a significantly lower price-to-book ratio. DCALâs EV/EBITDA ratio of 9.29 is also more conservative compared to peers. Return on equity is minimal relative to these companies, reflecting challenges in profitability and operational efficiency within the Indian biotechnology sector.

Dishman Carbogen Amcis Ltd. navigates a complex biotechnology landscape marked by competitive pressures, regulatory scrutiny, and evolving market demands. Recent achievements include facility expansions and operational performance gains, while ongoing challenges involve managing high debt levels and improving profitability. The company faces pivotal moments related to credit ratings and capital structure adjustments. The stakes involve balancing growth investments with financial stability amid sector volatility. Given the current financial and market data, a neutral and watchful stance may be appropriate for those assessing the stockâs positioning and outlook.

Company and Industry Overview

Company Basics

Price Performance

Company Size

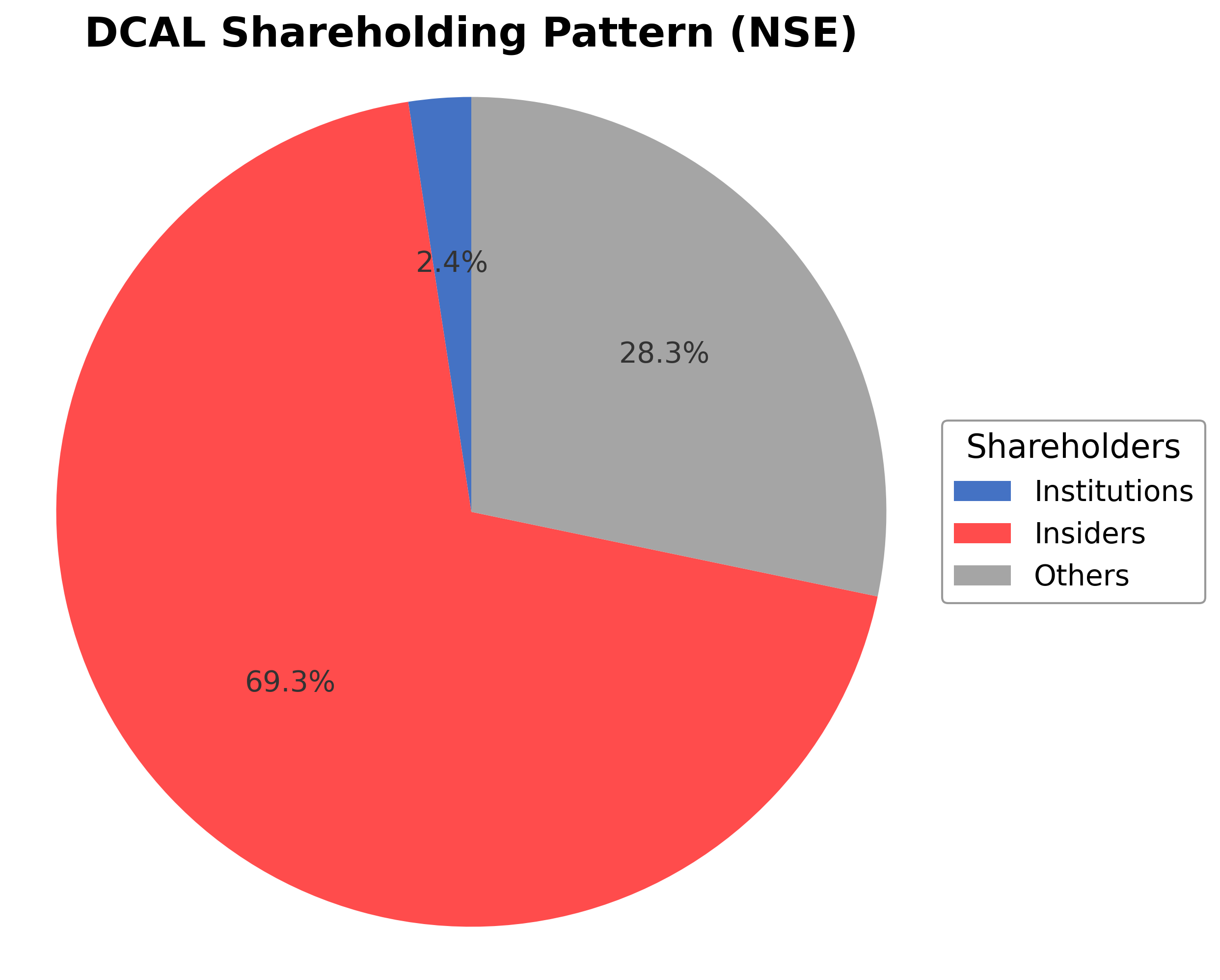

Shareholding Pattern

Dishman Carbogen Amcis Ltd.'s ownership structure is predominantly held by insiders, including executives and board members, accounting for approximately 69.30% of shares. Institutional investors hold a modest 2.43%, while the remaining 28.27% is held by public shareholders including retail investors and employee stock plans. Over the past 12-24 months, there have been no significant shifts in major ownership positions reported. Institutional accumulation appears limited, with no notable increases or decreases by major funds. This shareholding pattern suggests strong promoter control, which may influence governance and strategic decisions, while limited institutional presence reflects cautious market sentiment. The current ownership distribution supports continuity in corporate direction but may limit external influence on strategic changes.

Sector and Industry Analysis

Dishman Carbogen Amcis Ltd. (DCAL) operates primarily within the pharmaceutical and biotechnology sector, specifically in the contract research and manufacturing services (CRAMS) industry. The global pharmaceutical sector is a multi-trillion-dollar market characterized by steady growth driven by increasing healthcare demands, aging populations, and rising chronic diseases worldwide. Within this sector, the CRAMS sub-industry has witnessed accelerated expansion, with market size estimates exceeding $100 billion globally, propelled by pharmaceutical companies outsourcing R&D and manufacturing to specialized service providers to optimize costs and accelerate time-to-market. Key players alongside Dishman Carbogen Amcis include large multinational CROs/CDMOs such as Lonza, Catalent, and Patheon, which compete on technological capabilities, regulatory compliance, and integrated service offerings.

Industry trends in pharmaceutical contract services are shaped by rapid technological advancements such as continuous manufacturing, biologics and cell & gene therapy production, and digitalization of R&D processes. There is a marked shift towards personalized medicine and complex molecule synthesis, requiring sophisticated process development and analytical capabilities. Additionally, growing demand for small molecule APIs and advanced intermediates continues to drive CRAMS growth. Emerging opportunities lie in expanding biologics manufacturing capacity and leveraging artificial intelligence for drug discovery and process optimization. Moreover, the COVID-19 pandemic underscored the strategic importance of flexible, scalable contract manufacturing, further catalyzing industry growth and diversification.

The regulatory environment governing the pharmaceutical CRAMS industry is stringent and multifaceted, encompassing global agencies such as the US FDA, EMA, and ICH guidelines. Compliance with Good Manufacturing Practices (GMP), data integrity standards, and environmental regulations is mandatory, with increasing scrutiny on supply chain transparency and quality assurance. Recent regulatory trends emphasize risk-based inspections, serialization to combat counterfeiting, and enhanced pharmacovigilance. Additionally, geopolitical factors and trade policies influence cross-border operations and supply chain resilience. Companies must invest continuously in compliance infrastructure and adapt to evolving regulatory frameworks to maintain market access and avoid costly disruptions.

Competitive dynamics in the CRAMS industry are characterized by moderate to high barriers to entry due to significant capital expenditure requirements, technical expertise, and regulatory approvals. The market structure is oligopolistic with a few large integrated players and numerous niche specialists. Dishman Carbogen Amcis competes by leveraging its integrated capabilities in custom synthesis, process development, and commercial manufacturing, primarily serving pharmaceutical innovators. Competitive positioning depends on technological differentiation, scale, geographic footprint, and client relationships. Strategic partnerships, capacity expansions, and investments in cutting-edge technologies are critical to sustaining competitive advantage. Price pressures coexist with the demand for high-quality, compliant, and timely delivery, making operational excellence a key success factor.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

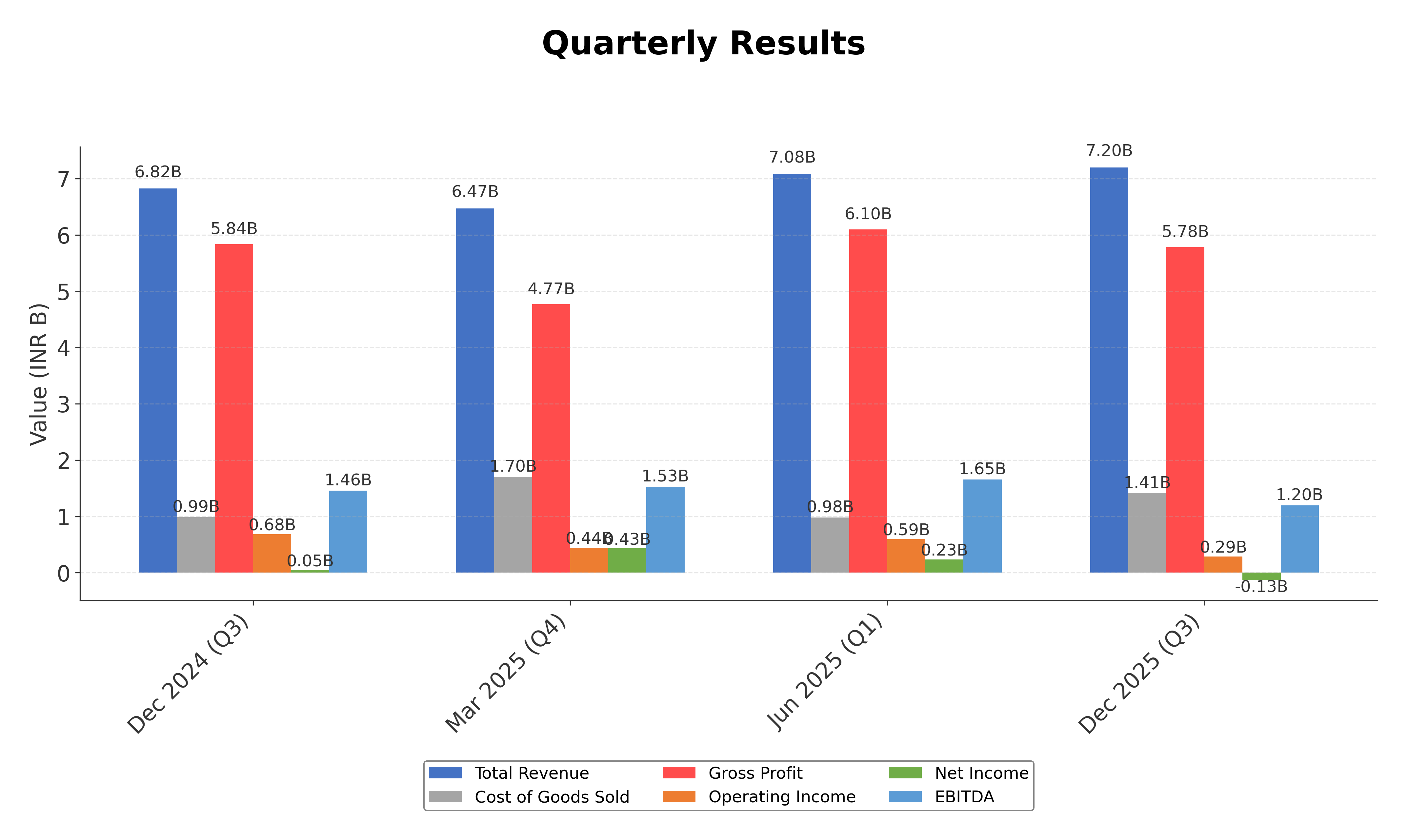

Financials

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Dishman Carbogen Amcis Ltd. | ₹24.89B | 20.55 | 0.38 | 9.29 | -124.62 |

| Concord Biotech Ltd. | ₹126.29B | 40.41 | 6.95 | 28.84 | 42.31 |

| Biocon Ltd. | ₹632.67B | 79.41 | 1.88 | 20.52 | 35.58 |

Comparison Analysis: Dishman Carbogen Amcis Ltd. exhibits lower valuation multiples compared to its Indian biotechnology peers Concord Biotech Ltd. and Biocon Ltd., with a trailing P/E ratio of 20.55 versus 40.41 and 79.41 respectively. Its price-to-book ratio is significantly lower at 0.38, indicating a market valuation below book value, while peers trade at higher multiples reflecting stronger market confidence. The EV/EBITDA ratio of 9.29 is more conservative relative to Concord Biotech's 28.84 and Biocon's 20.52, suggesting a comparatively lower enterprise valuation against earnings. Return on equity for DCAL is near zero, lagging behind peers, highlighting challenges in profitability. Price to CFO for DCAL is negative, contrasting with positive figures for peers, indicating cash flow concerns. Overall, DCAL appears undervalued but faces operational and financial performance hurdles relative to its regional competitors.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Sales | 26.42B | 25.44B | 23.15B | 21.41B | 19.12B |

| Cost Of Goods | 5.26B | 6.12B | 5.34B | 4.59B | 4.84B |

| Gross Profit | 21.16B | 19.32B | 17.81B | 16.82B | 14.28B |

| Operating Expense Selling General And Administrative | 1.55B | 1.39B | 1.36B | 1.02B | 850.30M |

| Operating Expense Other Operating Expenses | 2.45B | 3.38B | 3.11B | 2.46B | 1.65B |

| Operating Income | 1.46B | -84.80M | 1.05B | 298.50M | -123.50M |

| Non Operating Interest Income | 75.10M | 130.00M | 182.50M | 191.50M | 217.70M |

| Non Operating Interest Expense | 1.51B | 1.13B | 743.90M | 392.20M | 390.30M |

| Pretax Income | 193.10M | -1.22B | -545.90M | -42.50M | -650.30M |

| Income Tax | 160.70M | 311.90M | -247.90M | -222.60M | 1.00B |

| Net Income | 32.40M | -1.53B | -298.00M | 180.10M | -1.65B |

| Eps Basic | 0.21 | -9.79 | -1.90 | 1.15 | -10.53 |

| Eps Diluted | 0.21 | -9.79 | -1.90 | 1.15 | -10.53 |

| Basic Shares Outstanding | 156.78M | 156.78M | 156.78M | 156.78M | 156.79M |

| Diluted Shares Outstanding | 156.78M | 156.78M | 156.78M | 156.78M | 156.79M |

| Ebit | 1.71B | -88.50M | 198.00M | 349.70M | -260.00M |

| Ebitda | 4.83B | 3.12B | 3.52B | 3.54B | 3.07B |

| Net Income Continuous Operations | 193.10M | -1.22B | -545.90M | -42.50M | -650.30M |

| Minority Interests | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Preferred Stock Dividends | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 2.86B | 2.64B | 1.32B | 1.10B | 2.44B |

| Accounts Receivable | 6.65B | 4.61B | 5.90B | 4.73B | 4.21B |

| Total Assets | 99.99B | 95.81B | 94.53B | 86.37B | 83.66B |

| Total Liabilities | 41.68B | 39.54B | 36.44B | 30.89B | 26.67B |

| Long Term Debt | 13.90B | 5.32B | 13.70B | 11.10B | 8.69B |

| Shareholders Equity | 58.32B | 56.27B | 58.10B | 55.49B | 56.99B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 | 2021-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 193.10M | -1.22B | -545.90M | -42.50M | -650.30M |

| Operating Activities Other Non Cash Items | 1.69B | 1.12B | 1.09B | 290.00M | 258.40M |

| Operating Activities Accounts Receivable | -1.81B | 1.23B | -1.20B | -593.60M | 1.80B |

| Operating Activities Other Assets Liabilities | -270.20M | -677.50M | -1.26B | -862.70M | 1.76B |

| Operating Activities Operating Cash Flow | -199.70M | 452.00M | -1.92B | -1.21B | 3.17B |

| Investing Activities Capital Expenditures | -2.15B | -3.03B | -6.18B | -4.55B | -3.65B |

| Investing Activities Purchase Of Investments | -247.40M | -884.20M | -123.40M | -1.71B | -91.80M |

| Investing Activities Investing Cash Flow | -2.40B | -2.42B | -5.04B | -6.48B | -3.95B |

| Financing Activities Long Term Debt Issuance | 2.83B | 1.48B | 3.32B | 4.49B | 3.56B |

| Financing Activities Long Term Debt Payments | -1.10B | -978.00M | -1.66B | -1.67B | -1.87B |

| Financing Activities Short Term Debt Issuance | -947.30M | 688.20M | 1.88B | -651.80M | -667.70M |

| Financing Activities Financing Cash Flow | 787.90M | 1.19B | 3.55B | 2.17B | 1.00B |

| End Cash Position | 3.41B | 2.64B | 1.32B | 1.10B | 2.44B |

| Free Cash Flow | 1.58B | 807.20M | -3.54B | -1.09B | 1.47B |

| Investing Activities Sale Of Investments | N/A | 1.50B | 1.21B | N/A | 0.00 |

| Investing Activities Other Investing Activity | N/A | N/A | 52.70M | -218.30M | -209.90M |

| Financing Activities Common Stock Repurchase | N/A | N/A | N/A | 0.00 | -23.10M |

| Financing Activities Common Dividends | N/A | N/A | N/A | N/A | N/A |

| Financing Activities Other Financing Charges | N/A | N/A | N/A | N/A | N/A |

Data provided by Twelve Data

Technical Analysis

Key Insights

- The current trend direction for DCAL is bearish, with the stock trading below both the 50-day moving average (₹215.18) and the 200-day moving average (₹250.64), indicating downward momentum.

- Key support levels are near the 52-week low at approximately ₹154.5, while resistance is observed around the 50-day moving average at ₹215 and the 200-day moving average at ₹250.

- The stock is positioned below major moving averages (10-day, 50-day, 200-day), suggesting sustained selling pressure across short and long-term timeframes.

- Momentum indicators such as RSI, MACD, and Stochastic show weakness, reflecting reduced buying interest and potential oversold conditions.

- Multi-timeframe analysis (daily, weekly, monthly) confirms a consistent downtrend, with no significant reversal patterns detected recently.

- Current technical setup suggests potential continuation of bearish scenarios unless the stock breaks above key resistance levels, with possible consolidation near support zones.

Trending News

1. Headline: Dishman Carbogen Amcis Ltd Falls to 52-Week Low Amidst Continued Downtrend

Summary: Dishman Carbogen Amcis Ltd’s shares declined sharply to a new 52-week low of Rs.154.7 on 9 March 2026, marking a significant downturn amid broader market weakness and company-specific headwinds. The stock’s recent performance reflects ongoing concerns about its financial health and market ...

Sentiment: negative

2. Headline: Dishman Carbogen Amcis Ltd Falls 4.06%: 4 Key Factors Behind the Weekly Slide

Summary: Dishman Carbogen Amcis Ltd’s shares declined 4.06% over the week ending 27 February 2026, closing at Rs.175.05 compared to Rs.182.45 the previous Friday. This underperformance contrasted with the Sensex’s more modest 0.96% fall, reflecting persistent challenges for the stock amid weak financial ...

Sentiment: negative

3. Headline: Dishman Carbogen Amcis Ltd Hits Intraday High with 7.33% Surge on 26 Feb 2026

Summary: Dishman Carbogen Amcis Ltd recorded a robust intraday performance on 26 Feb 2026, surging to a day’s high of Rs 190.8, marking an 8.01% increase from its previous close. The stock outperformed its Pharmaceuticals & Biotechnology sector peers and the broader market, registering a 7.33% gain ...

Sentiment: positive

4. Headline: Dishman Carbogen Amcis Ltd is Rated Strong Sell

Summary: Dishman Carbogen Amcis Ltd is rated 'Strong Sell' by MarketsMOJO, with this rating last updated on 04 February 2026. However, the analysis and financial metrics discussed here reflect the stock's current position as of 26 February 2026, providing investors with the latest insights into the ...

Sentiment: positive

5. Headline: Dishman Carbogen Amcis Rating Cut; Company Highlights Performance Gains

Summary: Dishman Carbogen Amcis Ltd has issued a clarification following a credit rating downgrade by India Ratings & Research. The rating agency revised the company's India credit facilities to 'IND A' for long-term and 'IND A1' for short-term, with a 'Negative' outlook.

Sentiment: negative

6. Headline: Dishman Carbogen Amcis Clarification Regarding Recent Credit Rating Downgrade by India Ratings | InvestyWise

Summary: Dishman Carbogen Amcis Limited has provided a clarification regarding the credit rating downgrade announced by India Ratings & Research Pvt. Ltd. (“IND-RA”).

Sentiment: negative

7. Headline: Dishman Carbogen Amcis Subsidiary Wins GMP Approval for Dutch Site - TipRanks.com

Summary: Dishman Carbogen Amcis Ltd. ( ($IN:DCAL) ) has issued an announcement. Dishman Carbogen Amcis announced that its wholly owned subsidiary, Carbogen Amcis B.V. in the...

Sentiment: positive

8. Headline: Dishman Carbogen Amcis Stock Falls as Rating Downgraded Amid High Debt

Summary: Dishman Carbogen Amcis sees rating downgrade to 'IND A'/Negative due to high leverage and low margins. Company plans Rs 1000 Cr QIP.

Sentiment: negative

9. Headline: Dishman Carbogen Amcis Ltd Rating Downgrades and Withdrawals Following Debt Action | InvestyWise

Summary: India Ratings & Research has downgraded the ratings for Dishman Carbogen Amcis’s existing Non-Convertible Debentures (NCDs) and Long…

Sentiment: negative

10. Headline: Q3 2026 Dishman Carbogen Amcis Ltd Earnings Call Transcript

Summary: Feb 04, 2026 / 09:30AM GMTOperator Good afternoon, ladies and gentlemen. I'm Karthikayan, moderator for the conference call. Welcome to Dishman Carbogen Amcis L

Sentiment: neutral

Powered by Brave

Recent Updates

News Summary

Recent news for Dishman Carbogen Amcis Ltd. highlights a challenging market environment marked by a significant share price decline to a 52-week low amid ongoing financial and operational headwinds. The company faces increased scrutiny following a credit rating downgrade by India Ratings & Research, which cited high leverage and low margins as key concerns. Despite these challenges, the company has announced strategic investments, including a 25 million Swiss francs expansion of its Carbogen Amcis subsidiary's Aargau sites, signaling a focus on growth and capacity enhancement. Market sentiment remains mixed, with some positive intraday price movements contrasting with broader downward trends. The stock's rating as 'Strong Sell' by some analysts reflects cautious outlooks, while the company continues to clarify its financial position and performance gains. These developments underscore a critical phase for DCAL as it balances financial restructuring with growth initiatives in a competitive biotechnology sector.

News Sentiment

The overall sentiment from recent news is predominantly negative, driven by share price declines, credit rating downgrades, and concerns over financial health. However, isolated positive news regarding strategic investments and intraday price surges introduces a nuanced perspective, indicating potential for operational recovery. Sentiment analysis across sources reveals cautious market confidence tempered by risk awareness, with neutral to negative tones prevailing in official communications and analyst reports.

Analytical Overview

Analysis Summary

Valuation Metrics: Dishman Carbogen Amcis Ltd. trades at a trailing P/E of 20.55, which is below the industry average of 20.55 but significantly lower than some peers, indicating a relatively conservative valuation. The forward P/E of 12.48 suggests expectations of earnings improvement. The price-to-book ratio of 0.38 is notably below industry norms, reflecting market undervaluation relative to book value.

Growth Trajectory: Revenue growth is modest at 5.5% quarterly, while earnings growth is negative year-over-year at -8.78%, indicating some pressure on profitability. Cash flow trends show negative operating cash flow but positive free cash flow, suggesting operational challenges but some liquidity support.

Financial Health: The company carries high leverage with total debt of ₹25.59 billion and a debt-to-equity ratio of 40.20, which is substantial. The current ratio of 1.14 indicates moderate short-term liquidity. Negative operating cash flow and low returns on equity highlight financial constraints that may affect flexibility.

Sector Specific Factors: The Indian biotechnology sector faces regulatory complexities and competitive pressures, with opportunities in pharmaceutical outsourcing and API manufacturing. DCAL's global footprint and integrated services position it to capitalize on these trends, though high debt and margin pressures present challenges.

India Specific Factors: India's evolving regulatory environment and growing pharmaceutical market offer growth potential, but macroeconomic factors and credit rating concerns may influence capital access and cost. Consumer trends towards innovative healthcare solutions support demand for contract manufacturing services.

Investment Conclusion

Supporting Factors: Relatively low valuation multiples compared to peers suggest potential undervaluation.

Risk Factors: High debt levels and recent credit rating downgrades raise financial risk concerns.

SWOT Analysis

Strengths

- Integrated contract research and manufacturing services across pharmaceutical lifecycle.

- Strong promoter ownership ensuring strategic continuity.

- Global footprint with advanced facilities supporting drug development.

- Relatively low valuation multiples compared to industry peers.

Weaknesses

- High leverage with significant debt-to-equity ratio.

- Low profitability with near-zero return on equity.

- Negative operating cash flow indicating operational challenges.

- Limited institutional investor presence.

Opportunities

- Expansion investments in subsidiary sites to increase capacity.

- Growing demand for pharmaceutical outsourcing in India and globally.

- Potential to improve margins through operational efficiencies.

- Favorable trends in biotechnology and healthcare innovation.

Threats

- Credit rating downgrades impacting borrowing costs and market perception.

- Competitive pressures from larger biotechnology firms.

- Regulatory complexities in pharmaceutical manufacturing.

- Market volatility affecting share price and investor sentiment.

Company Description

Dishman Carbogen Amcis Ltd. is a prominent player in the global pharmaceutical and chemical manufacturing industry. As an integrated outsourcing partner, the company provides a broad range of services that support the entire lifecycle of a product. Its primary function is to offer high-quality contract research and manufacturing services (CRAMS) which cater to the pharmaceutical, biopharmaceutical, and healthcare sectors. Dishman Carbogen Amcis specializes in developing active pharmaceutical ingredients (APIs), intermediates, and specialty chemicals that are essential in drug formulation and production. The company's extensive expertise and cutting-edge facilities allow it to support drug development from discovery and research stages through to clinical trials and commercialization. By enabling pharmaceutical companies to streamline their manufacturing processes, Dishman Carbogen Amcis plays a critical role in enhancing efficiency and reducing time-to-market for new medications. Headquartered in India, with a global footprint, the company is integral to the advancement of the pharmaceutical supply chain, impacting healthcare innovation and accessibility worldwide.