Aditya Infotech Limited (CPPLUS)

Stock Analysis Report

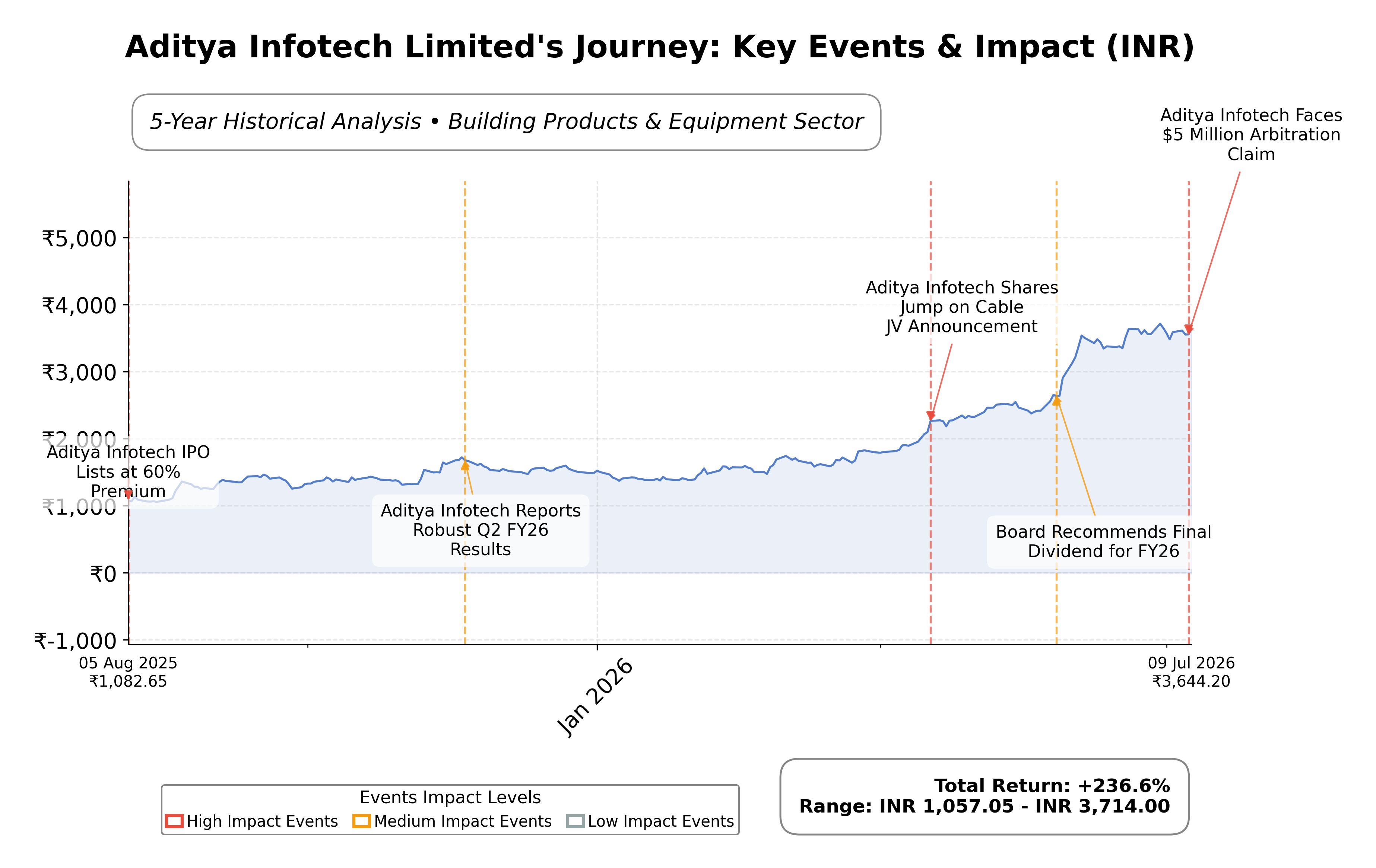

Stock Journey

Key Positives and Key Risks

Pros

- Strong market leadership with over 45% market share in Indian video surveillance, indicating competitive dominance.

- Robust financial performance with 35.6% revenue growth YoY and EBITDA margin expansion of over 500 basis points, reflecting operational efficiency.

- Healthy return on equity at 25.4%, demonstrating effective capital utilization and profitability.

Cons

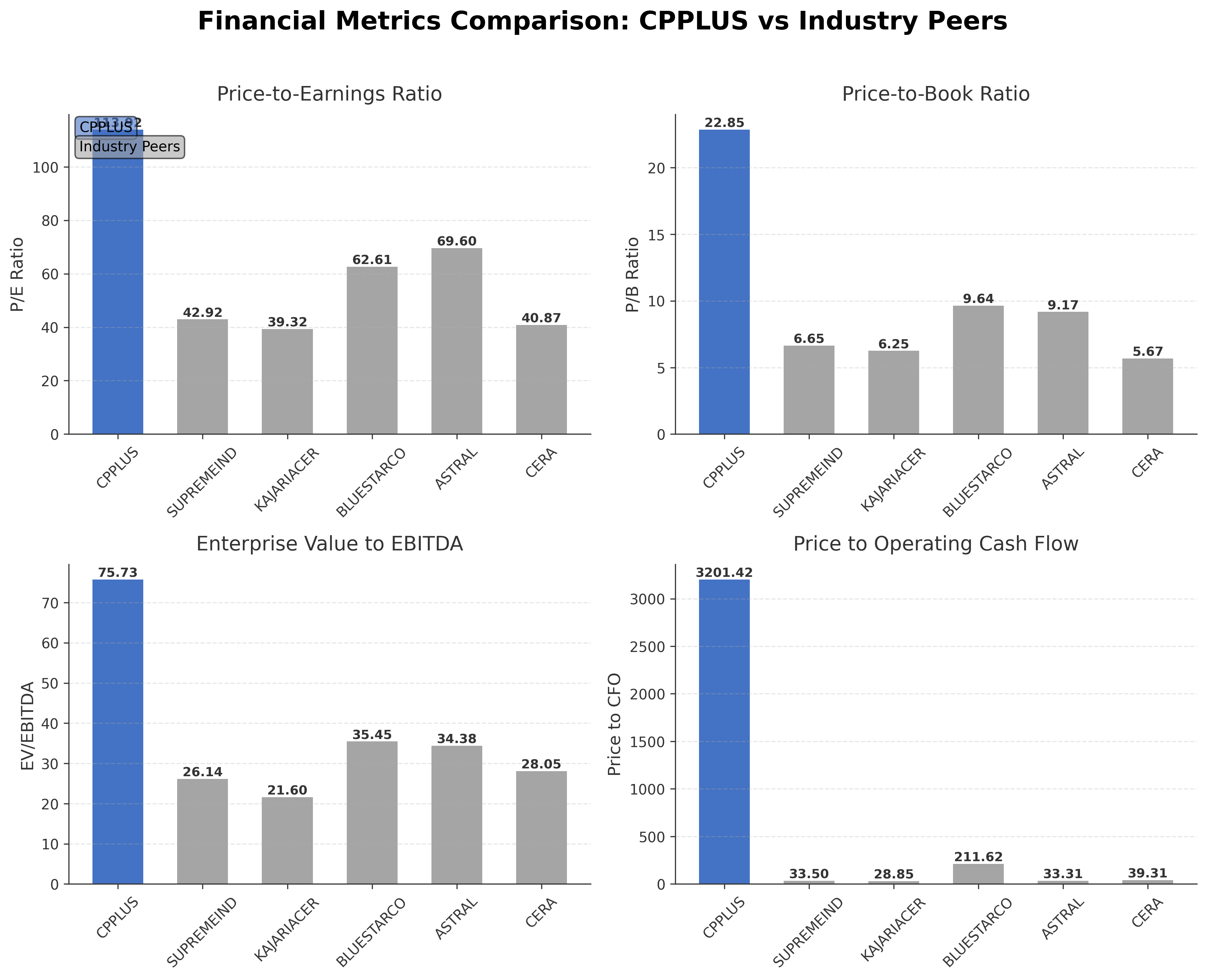

- Elevated valuation multiples including a trailing P/E of 113.9 and P/B of 22.85, suggesting premium pricing relative to earnings and book value.

- Negative free cash flow of approximately INR -1.2 billion, indicating significant capital expenditure and investment needs.

- Ongoing $5 million arbitration claim that introduces legal uncertainty and potential financial risk.

Disclosure: This information is for general awareness and does not constitute investment advice

Report Summary

Aditya Infotech Limited, trading under the symbol CPPLUS on the NSE, operates primarily in the Industrials sector within the Building Products & Equipment industry. The company specializes in security and surveillance technology, offering a comprehensive range of video security products and solutions under the CP Plus brand. Its portfolio includes analog HD and network cameras, digital video recorders, home security devices, and access control systems, serving government, commercial, residential, and industrial clients across India. The firm leverages a vertically integrated business model supported by extensive distribution and system integrator networks, local R&D, and manufacturing partnerships, positioning it as a leading provider in the Indian video surveillance market.

Financially, Aditya Infotech reported trailing twelve months (TTM) revenue of approximately INR 42.2 billion, with a gross margin of 31.8%, operating margin of 16.5%, and net profit margin of 8.7%. The company demonstrated strong profitability and operational efficiency, reflected in a return on equity (ROE) of 25.4% and return on assets (ROA) of 8.9%. The return on invested capital (ROIC) is supported by robust EBITDA of INR 6.1 billion, indicating effective capital utilization. Quarterly revenue growth stood at 45.5%, and earnings per share (EPS) reached 31.99 INR, underscoring significant earnings momentum.

Valuation metrics reveal a trailing price-to-earnings (P/E) ratio of 113.9 and a forward P/E of 50.4, indicating a premium valuation relative to earnings expectations. The price-to-book (P/B) ratio is elevated at 22.85, and the enterprise value to EBITDA (EV/EBITDA) stands at 75.7, suggesting the stock is priced richly compared to its fundamentals. The market capitalization is approximately INR 431.6 billion. The stock currently trades at INR 3,661, within a 52-week range of INR 1,015 to INR 3,787, reflecting a strong upward price movement over the past year.

Aditya Infotech’s strengths include its dominant market share of over 45% in the Indian video surveillance sector, strong cash position with INR 1.99 billion in cash against INR 1.8 billion in debt, and expanding manufacturing capacity to 2.5 million units monthly. Key risks involve ongoing arbitration claims amounting to USD 5 million, competitive pressures in a rapidly evolving technology space, and regulatory challenges. Recent strategic actions include successful IPO fundraising, product diversification with new brands like NEXIVUE and EYRA, and investments in AI-led surveillance technologies.

Technically, the stock exhibits bullish momentum supported by price trading above its 50-day and 200-day moving averages, with key support near INR 3,050 and resistance around INR 3,787. Momentum indicators such as RSI and MACD show positive trends across daily and weekly timeframes. Recent news highlights strong earnings growth and market leadership, balanced by neutral sentiment around arbitration proceedings. Overall, the data suggests a nuanced stance where accumulation interest may be tempered by valuation considerations and legal uncertainties.

Company and Industry Overview

Company Basics

Price Performance

Company Size

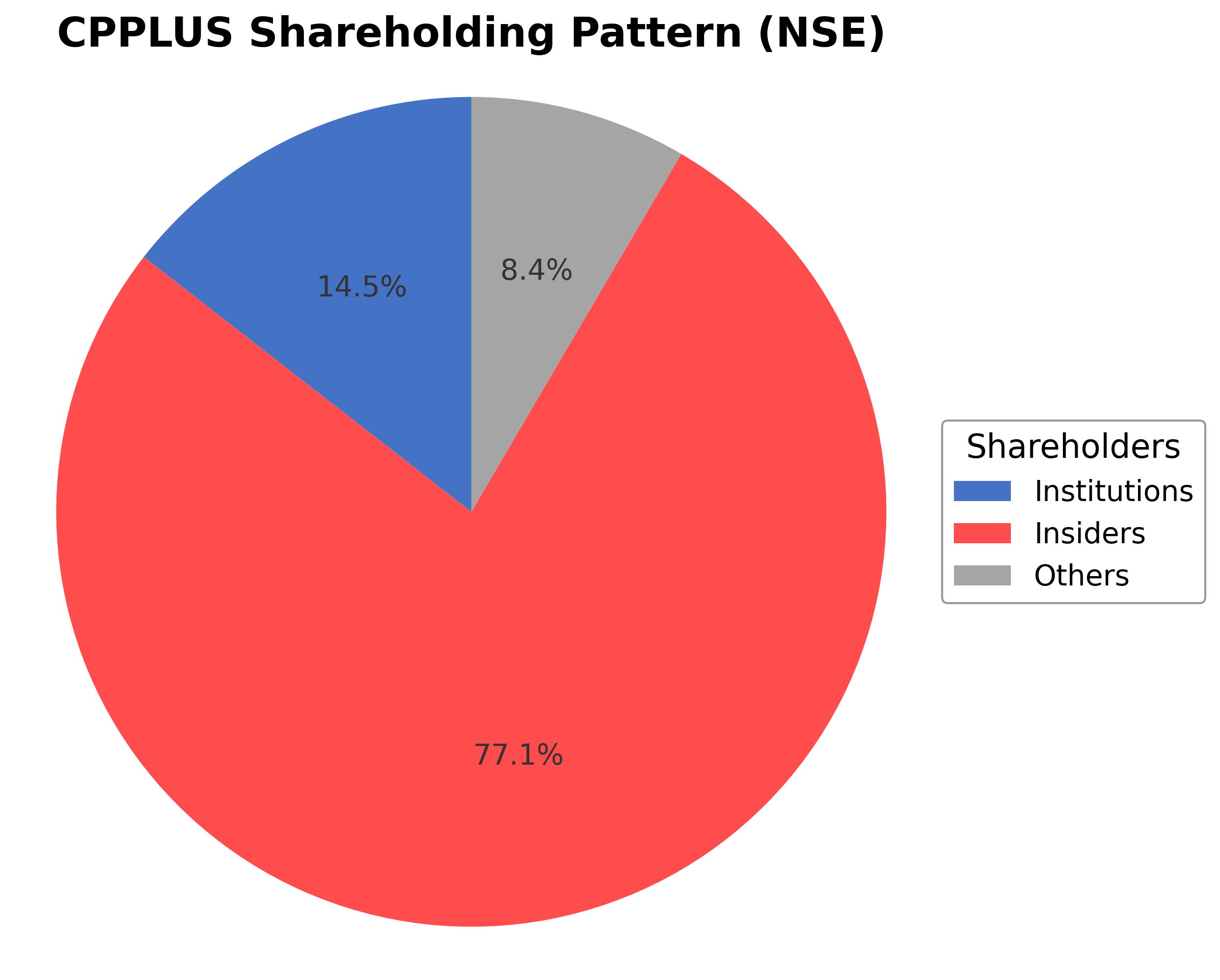

Shareholding Pattern

Sector and Industry Analysis

The video security and surveillance sector in India has witnessed robust growth driven by increasing demand across residential, commercial, and government segments. The market size has expanded significantly, with leading players like Aditya Infotech Limited (CP PLUS) capturing substantial market share, reportedly rising from 20.8% in FY25 to over 45% in FY26. The sector benefits from rising urbanization, infrastructure development, and heightened security concerns, positioning it on a strong growth trajectory.

Industry trends include rapid technological advancements such as AI-enabled cameras, cloud-based monitoring, and integration with IoT platforms, enhancing product offerings and customer value. Competitive dynamics are marked by intense rivalry among established firms, with high capital requirements and technological expertise serving as barriers to entry. Companies like Aditya Infotech leverage increased manufacturing capacity and brand recognition to consolidate their leadership in a fragmented market.

The regulatory landscape is shaped by data privacy laws and government mandates on surveillance standards, impacting product design and deployment. Compliance with cybersecurity norms and import-export regulations also influences operational strategies. Ongoing regulatory developments are expected to drive innovation while ensuring consumer protection, thereby shaping the sector’s future growth and competitive environment.

Note: Analysis synthesized from industry research, market reports, and regulatory filings. Information is subject to change based on market conditions.

Financial Ratios Dashboard

Illustrative Scenario Analysis

DCF Assumptions:

Method: Two-Stage EPS-Priority Model

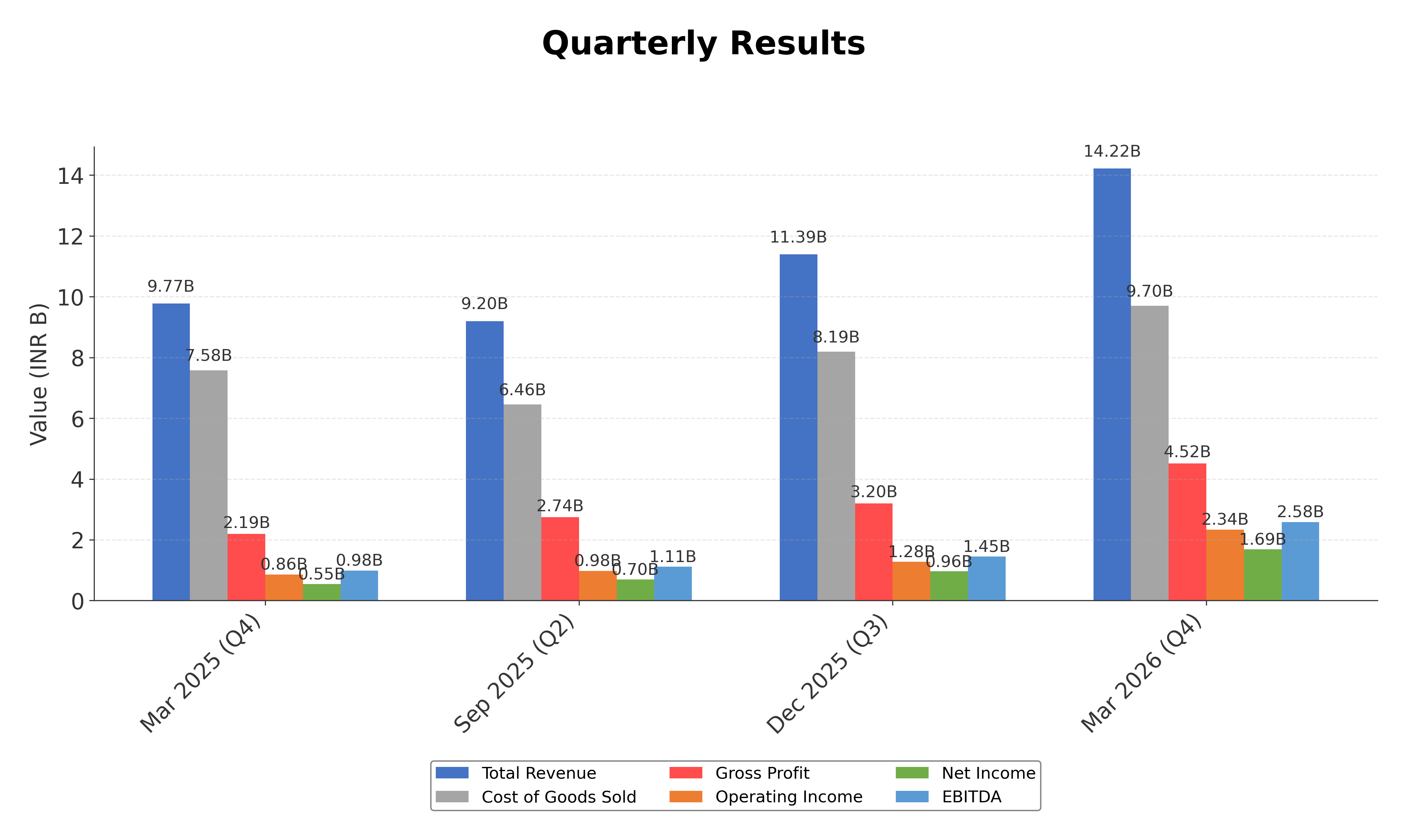

Financials

Peer Analysis

| Company Name | Market Cap | P/E Ratio | P/B Ratio | EV/EBITDA | Price to CFO |

|---|---|---|---|---|---|

| Aditya Infotech Limited | ₹431.62B | 113.92 | 22.85 | 75.73 | 3201.42 |

| Supreme Industries Ltd. | ₹410.31B | 42.92 | 6.65 | 26.14 | 33.50 |

| Kajaria Ceramics Ltd. | ₹191.49B | 39.32 | 6.25 | 21.60 | 28.85 |

| Blue Star Ltd. | ₹325.49B | 62.61 | 9.64 | 35.45 | 211.62 |

| Astral Limited | ₹372.08B | 69.60 | 9.17 | 34.38 | 33.31 |

| Cera Sanitaryware Ltd. | ₹83.29B | 40.87 | 5.67 | 28.05 | 39.31 |

Comparison Analysis: Aditya Infotech Limited trades at significantly higher valuation multiples compared to its regional industry peers, with a trailing P/E ratio of 113.92 versus peer averages ranging from approximately 39 to 70. Its price-to-book ratio of 22.85 also exceeds the peer range of 5.67 to 9.64, indicating a premium market pricing relative to book value. The EV/EBITDA multiple of 75.73 is notably elevated compared to peers, reflecting expectations of superior growth or profitability. Return on equity at 25.42% surpasses all listed peers, demonstrating strong capital efficiency. However, the extraordinarily high price to cash flow ratio of 3201.42 suggests a stretched valuation relative to operating cash flow, which contrasts with more moderate peer ratios. Overall, Aditya Infotech exhibits leadership in profitability but commands a premium valuation that may reflect growth prospects or market positioning.

Financial Metrics Comparison with Peers

Financial Statements

Comprehensive financial data including income, balance sheet, and cash flow metrics

Income Statement

| fiscal_date | 2026-03-31 | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 |

|---|---|---|---|---|---|

| Sales | 42.21B | 31.12B | 27.82B | 22.84B | 16.46B |

| Cost Of Goods | 30.07B | 24.42B | 22.72B | 18.99B | 13.55B |

| Gross Profit | 12.14B | 6.69B | 5.10B | 3.85B | 2.91B |

| Operating Expense Other Operating Expenses | 3.05B | 2.19B | 502.02M | 378.87M | 189.72M |

| Operating Income | 5.10B | 2.16B | 2.09B | 1.56B | 1.36B |

| Non Operating Interest Expense | 302.04M | 418.12M | 299.30M | 208.13M | 189.91M |

| Pretax Income | 4.93B | 1.85B | 1.65B | 1.43B | 1.29B |

| Income Tax | 1.25B | 827.13M | 494.47M | 348.71M | 324.18M |

| Net Income | 3.68B | 3.51B | 1.15B | 1.08B | 969.31M |

| Ebit | 5.23B | 2.27B | 1.95B | 1.64B | 1.48B |

| Ebitda | 5.79B | 5.07B | 2.06B | 1.80B | 1.58B |

| Net Income Continuous Operations | 4.93B | 4.34B | 1.65B | 1.43B | 1.29B |

| Preferred Stock Dividends | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Operating Expense Selling General And Administrative | N/A | 1.29B | 975.99M | 741.87M | 419.18M |

| Non Operating Interest Income | N/A | 100.20M | 109.44M | 64.27M | 70.03M |

| Eps Basic | N/A | 29.97 | 9.83 | 9.24 | 8.27 |

| Eps Diluted | N/A | 29.97 | 9.83 | 9.24 | 8.27 |

| Basic Shares Outstanding | N/A | 117.22M | 117.22M | 117.22M | 117.22M |

| Diluted Shares Outstanding | N/A | 117.22M | 117.22M | 117.22M | 117.22M |

| Minority Interests | N/A | 0.00 | 0.00 | 0.00 | 0.00 |

Data provided by Twelve Data

Balance Sheet

| fiscal_date | 2026-03-31 | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 |

|---|---|---|---|---|---|

| Cash And Cash Equivalents | 1.65B | 1.36B | 394.67M | 1.48B | 1.05B |

| Accounts Receivable | 14.04B | 10.39B | 7.34B | 6.15B | 5.25B |

| Total Assets | 39.91B | 31.75B | 16.44B | 17.09B | 12.14B |

| Total Liabilities | 21.14B | 21.57B | 12.20B | 13.97B | 9.28B |

| Long Term Debt | 988.97M | 434.82M | 459.29M | 524.65M | 530.11M |

| Shareholders Equity | 18.77B | 10.18B | 4.24B | 3.12B | 2.87B |

Data provided by Twelve Data

Cash Flow Statement

| fiscal_date | 2026-03-31 | 2025-03-31 | 2024-03-31 | 2023-03-31 | 2022-03-31 |

|---|---|---|---|---|---|

| Operating Activities Net Income | 4.93B | 4.34B | 1.65B | 1.43B | 1.29B |

| Operating Activities Stock Based Compensation | 117.77M | 117.85M | 0.00 | 0.00 | N/A |

| Operating Activities Other Non Cash Items | 210.09M | 312.37M | 186.33M | 130.97M | 31.33M |

| Operating Activities Accounts Receivable | -3.82B | -3.12B | -1.20B | -895.07M | -1.48B |

| Operating Activities Other Assets Liabilities | -3.62B | -375.50M | 680.77M | -2.16B | -2.55B |

| Operating Activities Operating Cash Flow | -2.18B | 1.27B | 1.31B | -1.49B | -2.70B |

| Investing Activities Capital Expenditures | -1.33B | -262.46M | -64.12M | -70.45M | -67.04M |

| Investing Activities Other Investing Activity | 520.00K | 3.14M | 4.22M | 4.68M | 4.32M |

| Investing Activities Investing Cash Flow | -1.33B | -105.51M | 1.14B | -1.31B | -976.64M |

| Financing Activities Long Term Debt Issuance | 707.96M | 131.34M | 49.42M | 325.00M | 500.00M |

| Financing Activities Long Term Debt Payments | -15.26B | -22.17B | -17.53B | -6.01B | -456.96M |

| Financing Activities Short Term Debt Issuance | -3.50B | 64.48M | 371.48M | 2.25B | 11.00M |

| Financing Activities Common Stock Issuance | 5.17B | 0.00 | N/A | N/A | N/A |

| Financing Activities Common Dividends | -180.00M | -180.00M | -10.00M | -38.50M | -10.00M |

| Financing Activities Other Financing Charges | 14.54M | 144.00M | -279.09M | -201.16M | -169.75M |

| Financing Activities Financing Cash Flow | -13.04B | -22.01B | -17.39B | -4.47B | -125.71M |

| End Cash Position | 1.65B | 1.36B | 394.67M | 1.48B | 1.05B |

| Free Cash Flow | -1.23B | 7.18M | -1.99B | 486.46M | 368.25M |

| Investing Activities Sale Of Investments | N/A | 153.81M | 1.20B | 52.60M | 0.00 |

| Financing Activities Common Stock Repurchase | N/A | 0.00 | 0.00 | -799.58M | 0.00 |

| Investing Activities Purchase Of Investments | N/A | N/A | 0.00 | -1.30B | -913.92M |

Data provided by Twelve Data

Technical Analysis

Key Insights

- Aditya Infotech's current trend is upward with strong price momentum, supported by consistent higher highs and higher lows in recent trading sessions.

- Key support levels are identified near INR 3,050 and INR 1,957, while resistance is observed around the 52-week high of INR 3,787.

- The stock price is trading above its 10-day, 50-day (INR 3,051.89), and 200-day (INR 1,957.95) moving averages, indicating a bullish trend across short and long-term horizons.

- Momentum indicators show RSI in the upper range, MACD is positive with a widening gap between signal and MACD lines, and Stochastic oscillators confirm strong buying pressure.

- Multi-timeframe analysis reveals bullish signals on daily, weekly, and monthly charts, with no significant divergence or reversal patterns detected.

- Current technical setup suggests potential continuation of upward movement, with possible consolidation near resistance levels before further directional decisions.

Trending News

Summary: Equirus Securities started with Add and a target price of Rs 3,800 (4.3% upside). Aditya Infotech, through its flagship CP PLUS brand, is the market leader in India's surveillance industry with an estimated market share of over 40%. The company operates a vertically integrated business model ...

Sentiment: positive

2. Headline: Broker’s Call: Aditya Infotech (Add) - The HinduBusinessLine

Summary: Discover Aditya Infotech's growth potential and strong market position in India's video surveillance industry, with a target price of ₹3,800.

Sentiment: positive

3. Headline: Stocks to Watch, July 9: TCS, SBI, Tata Steel, NLC India, NALCO, JSW Energy, M&M - The HinduBusinessLine

Summary: Digital access to daily edition e-PaperSubscribe to Newsletters ... THIS AD SUPPORTS OUR JOURNALISM. SUBSCRIBE FOR MINIMAL ADS. THIS AD SUPPORTS OUR JOURNALISM. SUBSCRIBE FOR MINIMAL ADS. Updated - July 09, 2026 at 10:40 AM. ... https://www.thehindubusinessline.com/markets/stocks-in-focus-today-tcs-sbi-tata-steel-nlc-india-nalco-jsw-energy-aditya-infotech...

Sentiment: neutral

4. Headline: Stock Market Highlights, July 9: Sensex ends 238 points higher; Nifty closes above 23,950 - The HinduBusinessLine

Summary: Sensex Today, Nifty 50 | Stock Market Highlights: The Sensex closed 238.22 points, or 0.31 per cent, higher at 76,741.82, while the Nifty gained 80.75 points, or 0.34 per cent, to settle at 23,962.80 after Wednesday’s sharp slide.

Sentiment: positive

5. Headline: Aditya Infotech fixes record date for ₹1.64 dividend

Summary: The dispute arises from an agreement where Aditya Infotech proposed to purchase and resell certain products of Avathon and SparkCognition. The claimants have demanded USD 5,000,000, approximately INR 47,50,00,00, along with interest at 18% per annum accruing from May 16, 2027. The disclosure was submitted to the National Stock Exchange of India Limited ...

Sentiment: neutral

Powered by Brave

Recent Updates

News Summary

As of July 8, 2026. Aditya Infotech faces a $5 million arbitration claim filed by Avathon Inc. and SparkCognition India Private Ltd, alleging breach of contract related to product purchase and resale agreements. The company disclosed that the claim includes a principal amount plus 18% interest accruing from May 16, 2027, but management assesses no material financial impact is expected. Concurrently, the company reported strong Q4 FY26 and full-year FY26 financial results, with revenue growth of 45.5% YoY in Q4 and 35.6% YoY for FY26, EBITDA rising 124.1% YoY, and PAT increasing 166.1% YoY. Manufacturing capacity expanded to 2.5 million units monthly, supporting growth and localization efforts. The company also completed a successful IPO in August 2025, raising significant capital to fund expansion and innovation initiatives.

News Sentiment

The overall sentiment from recent updates is cautiously positive. Strong financial performance and market share gains drive optimism, supported by capacity expansion and strategic product launches. However, the arbitration claim introduces a neutral to slightly cautious tone, as the company navigates legal proceedings without expected material financial impact. Dividend announcements and analyst coverage reinforce confidence in the company's fundamentals. The balance of positive operational developments and legal uncertainties suggests a measured outlook among stakeholders.

Source List

Analytical Overview

Analysis Summary

Aditya Infotech's valuation metrics, including a trailing P/E of 113.9 and forward P/E of 50.4, are significantly higher than industry averages, reflecting market expectations for strong growth but also indicating a premium pricing relative to earnings. The company's revenue growth rate of 45.5% quarterly and 35.6% annually, coupled with expanding manufacturing capacity and improved EBITDA margins, demonstrate a robust growth trajectory supported by operational efficiencies. Financial health is solid, with a low debt-to-equity ratio of 0.096 and a positive current ratio of 1.53, although free cash flow remains negative, suggesting ongoing investment in growth initiatives. Sector-specific opportunities include increasing demand for video surveillance driven by regulatory changes and AI integration, while challenges encompass competitive pressures and legal disputes. India-specific factors such as evolving regulatory frameworks, rising security awareness, and economic growth underpin the company's market positioning and expansion potential.

Overall Business and Market Assessment

Supporting Factors: Key supporting factors include Aditya Infotech's dominant market share exceeding 45%, strong revenue and profit growth with EBITDA margins expanding by over 500 basis points, and strategic capacity expansion to 2.5 million units monthly. Risks to monitor involve the ongoing $5 million arbitration claim and the stretched valuation multiples relative to peers, which may impact near-term sentiment. The appropriate investment timeframe is medium to long-term, considering the company's growth initiatives and market leadership balanced against legal and valuation considerations. Overall, the analysis reflects a balanced outlook with significant growth prospects tempered by premium valuation and legal uncertainties.

Risk Factors: No data

SWOT Analysis

Strengths

- Market leader in Indian video surveillance with over 45% market share.

- Strong revenue growth of 35.6% year-over-year and expanding EBITDA margins.

- Robust return on equity at 25.4% indicating efficient capital use.

- Vertically integrated business model with extensive distribution and manufacturing capabilities.

Weaknesses

- High valuation multiples with P/E ratio exceeding 110 and P/B ratio above 22.

- Negative free cash flow indicating significant ongoing investment requirements.

- Limited dividend yield at 0.05%, providing minimal income to shareholders.

- Relatively low institutional ownership at 14.47%, potentially limiting liquidity.

Opportunities

- Growing demand for AI-enabled video surveillance solutions in India.

- Expansion of manufacturing capacity to 2.5 million units supports scaling.

- Regulatory changes favoring increased security infrastructure investments.

- Product diversification with new brands like NEXIVUE and EYRA.

Threats

- Ongoing $5 million arbitration claim introduces legal and financial uncertainty.

- Intense competition in the security technology sector may pressure margins.

- Potential regulatory risks related to data privacy and surveillance laws.

- Macroeconomic volatility impacting capital expenditure in key sectors.

Company Description

Aditya Infotech Limited is a security and surveillance technology company focused on video security products, solutions, and services under the CP Plus brand. It develops and supplies intelligent video surveillance systems, including analog HD and network cameras, digital video recorders, home security devices, access control, and related accessories for government, commercial, residential, and industrial applications across India. The company supports nationwide deployment through an extensive channel ecosystem of distributors and system integrators, complemented by local R&D in Noida and manufacturing partnerships and facilities aimed at indigenous production. Its portfolio and integration capabilities position the firm as a key provider of end-to-end security infrastructure, spanning sectors such as banking, healthcare, education, law enforcement, hospitality, smart traffic, industrial, and retail. Independent assessments describe Aditya Infotech as one of India’s largest providers in video security by revenue, reflecting its scale and market presence. The business is led by a professional management team and continues to expand capacity and product depth to meet growing demand for electronic video surveillance solutions in India.